After 16 years of Viktor Orbán's rule, Hungary wakes up to a new reality. The Tisza party has secured a historic victory led by Péter Magyar, which not only ends the era of "illiberal democracy" but thanks to a likely constitutional supermajority (2/3 of seats) gives the new leader a mandate for a complete state overhaul. The forint is currently one of the strongest currencies in the global market during Monday's opening, despite sharp tensions in the Middle East. Meanwhile, Brussels looks toward Budapest with hope, which could signal further potential for the appreciation of local assets.

A Mandate for Great Change

The election result is a political earthquake, though largely anticipated by observers. Péter Magyar managed to mobilize the nation to reject the previous anti-European establishment. Although the vote count is still ongoing, all signs point to his Tisza party gaining two-thirds of the seats in parliament. Such a tool provides the opportunity to "unblock" many institutions that were secured by Orbán's party for years. In his victory speech, Magyar has already called for the resignation of key officials, including the Attorney General and judges of the Constitutional Court, promising a return to full democratic standards and the rule of law.

Forint: Is This Just the Beginning of a Larger Rally?

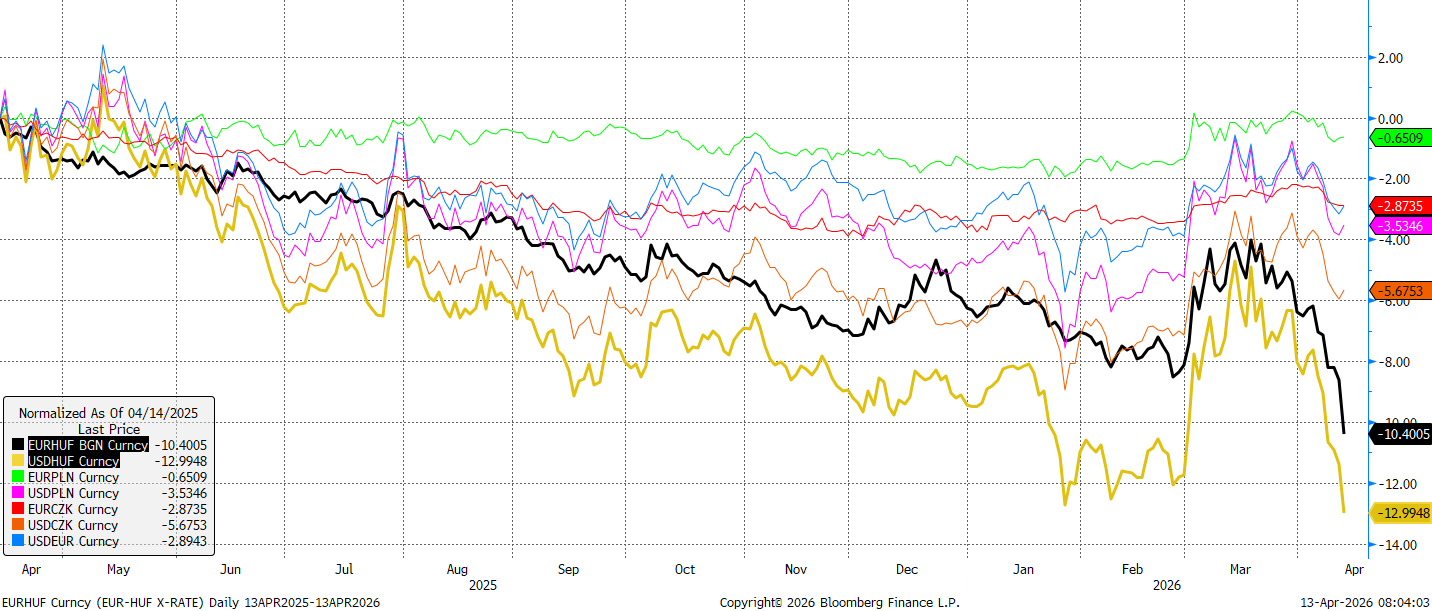

The Hungarian currency reacted instantly, strengthening significantly against both the US dollar and the euro. The USD/HUF pair is falling by nearly 2%, and the forint is currently one of the strongest currencies over the last 12 months—not only against the dollar but also the euro.

The forint has been decisively stronger against the US dollar compared to other regional currencies like the Polish złoty or the Czech koruna. Source: Bloomberg Finance LP.

Despite such a large appreciation over the last year, it is worth noting that historically, the forint was one of the weakest currencies in the region, leaving room for potential further gains. In its latest report, Morgan Stanley indicates that demand for domestic bonds will likely rise sharply, which could stimulate additional demand for the currency. The bank also sees potential for less monetary policy tightening due to the forint’s strength, which would allow for a more robust economic recovery.

-

5-Year Perspective: Looking back, the forint has endured years of deep depreciation caused by conflicts with the EU, energy market weaknesses, and unconventional economic policies. A return to stability could mean a further appreciation of 5–7% in the medium term.

-

Risk Premium: The collapse of the Orbán government drastically reduces the so-called political risk premium. The yield curve is expected to fall by 100–150 basis points, attracting foreign capital that has avoided Budapest for years.

Economy: Unlocking Billions from the EU

The key to future growth is the unfreezing of EU funds. Morgan Stanley estimates that access to the Recovery and Resilience Facility (KPO) and cohesion funds could raise Hungary's GDP growth potential by 1–1.5 percentage points.

What does this mean for taxes? While the new administration inherits an economy with some fiscal burden, the influx of euros from Brussels gives Magyar significant room for maneuver:

-

End of "Windfall Taxes": It is possible to withdraw the sectoral levies imposed by Orbán on banks, retail, and energy, which would improve the investment climate.

-

Investment over Consumption: EU funds will likely be directed toward infrastructure modernization and energy transformation, which is more pro-growth than Fidesz’s pre-election social transfers.

Geopolitical Shift: Ukraine and Russia

The victory of the Tisza party represents a fundamental change in foreign policy.

-

End of the Veto on Ukraine: Magyar has announced a return to the "European family." This means a potential end to the blocking of military and financial aid for Kyiv (including the crucial €90 billion package). Hungary ceases to be Russia's "Trojan horse" within EU and NATO structures.

-

Russian Commodities: Here, the change will be more evolutionary than revolutionary. Despite a pro-European course, Magyar presented a realistic timeline (extending into the next decade) for weaning the country off Russian oil and gas. Hungary is currently too dependent on infrastructure (TurkStream pipeline, MOL refineries adapted for Urals crude) to cut ties overnight, but the direction toward diversification is now irreversible.

Summary

Hungary is entering a new era. For investors, this is a signal to return to a market that has been "underweighted" for years. For the region, it is a chance to strengthen the Visegrád Group and the cohesion of the entire European Union. If Péter Magyar uses his constitutional majority to quickly repair relations with Brussels, the forint and the Hungarian stock exchange could become growth leaders in Central Europe for years to come.

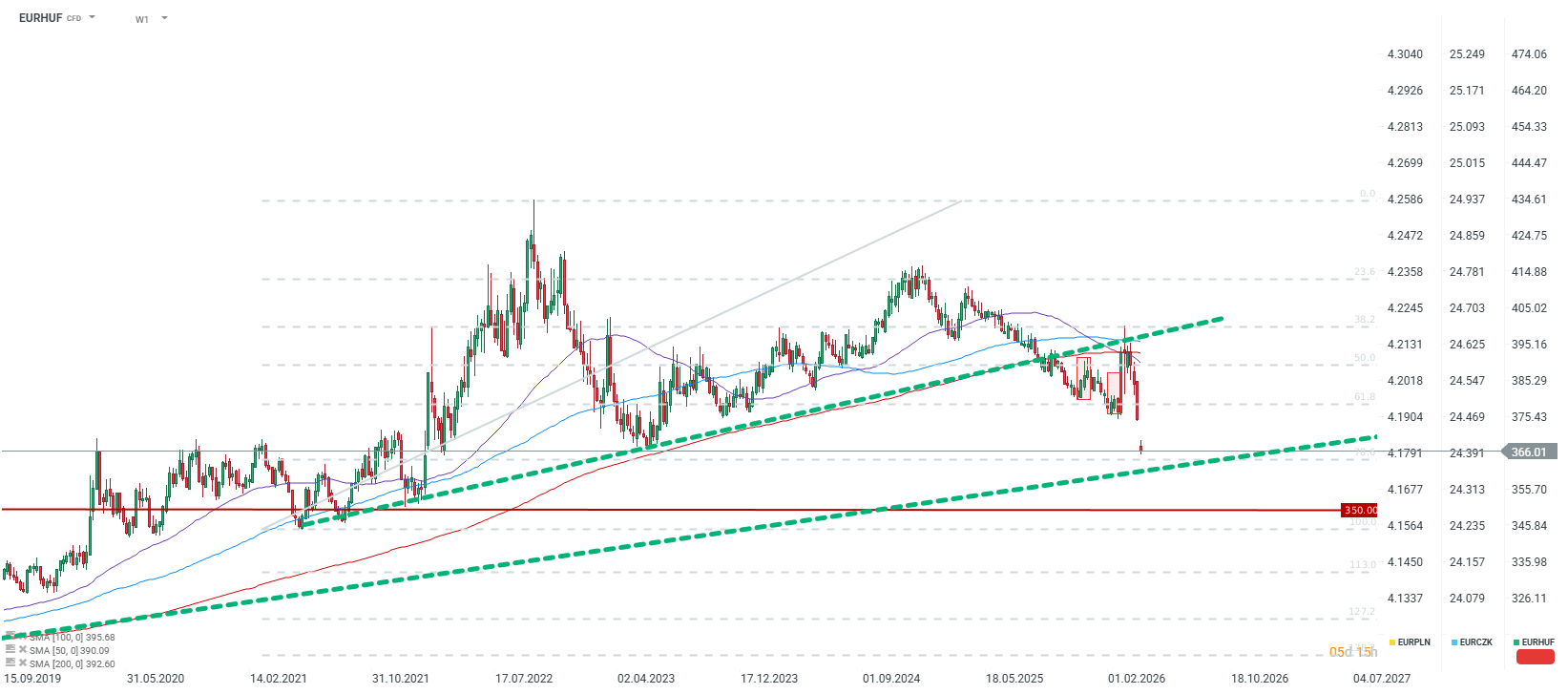

EURHUF is dropping to the 366 level, its lowest since April 2022. A potential further 5% appreciation of the forint would provide an opportunity to test 350, a level not seen since September 2021. A move below 360 would also represent a break of the 15-year upward trendline. Source: xStation5

EURHUF is dropping to the 366 level, its lowest since April 2022. A potential further 5% appreciation of the forint would provide an opportunity to test 350, a level not seen since September 2021. A move below 360 would also represent a break of the 15-year upward trendline. Source: xStation5

Oil Slides Ahead of the Weekend!

BREAKING: Eurozone recovery? Positive PMI data tempered by high oil and gas prices

Oil rises over 3% 🛢️

Defense sector ahead of earnings: Summary

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.