Can Belarus directly enter the war against Ukraine on Russia’s side?

This scenario is still not the base case, but it has also stopped being a fantasy. For markets, it would mean a rise in geopolitical risk, pressure on regional currencies, a potential strengthening of the US dollar, and a return of capital to the defence sector.

The return of the threat from the north?

The topic of Belarus fully joining the war against Ukraine on Russia’s side has regularly returned to the media since 2022. That was when the last Russian units were pushed out of northern Ukrainian territories after the failed offensive launched from the Belarusian direction.

Since then, Belarus has supported Russia in many ways. It has provided military infrastructure, barracks, hospitals, logistical facilities, and operational space. It has also taken part in activities supporting Russian strikes. Despite this, the regime in Minsk has tried to keep its involvement below the threshold of open war.

That is why further suggestions that Belarus may still enter the conflict can cause fatigue. In practice, however, the scenario of Minsk’s direct participation is no longer purely speculation. It has become an issue to analyse, monitor, and potentially price in.

The question of when escalation happens

The key question is: why would the Kremlin wait more than four years for Russia’s closest ally to enter the war only now?

Source: Bloomberg Finance

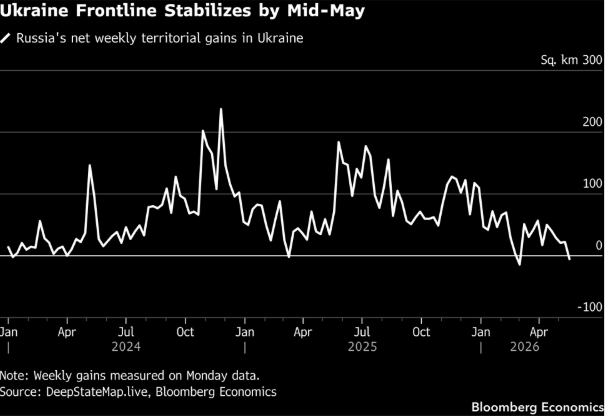

The answer may lie in Russia’s worsening situation on the front. More and more analytical centres indicate that the Russian war machine is losing momentum. In net terms, Russia is not losing territory, but available forces and resources are genuinely shrinking. The Kremlin may conclude that if Belarus does not enter the war in the near future, it may not join it at all.

Quiet mobilisation matters more than nuclear weapons

There are more and more indications of a slow but consistent shift in Belarus’s stance. Reports of gradual mobilisation of Belarusian forces appeared as early as the beginning of the year. Since then, they have been increasing in scale—though in a way that does not attract much media attention.

In the context of nuclear drills involving Belarus and Russia, a cool-headed assessment is needed. Nuclear weapons remain above all a tool of rhetorical pressure. Such exercises can, however, distract attention from more practical elements of escalation: reserve mobilisation and infrastructure expansion.

For NATO, more important than nuclear rhetoric itself is whether Minsk is genuinely increasing readiness for operations near the Ukrainian border. According to Ukrainian military officials, infrastructure expansion directed toward Ukraine is underway.

This is a more meaningful signal than propaganda statements alone.

The US and diplomatic pressure

Interest in Belarus is now being shown not only by Ukrainian military officials, but also by the United States. On 21 May, the President of Ukraine warned that any direct attempt by Belarus to engage on Russia’s side would meet with a devastating response.

Bloomberg reports also matter: according to them, the US allegedly asked Ukraine to ease sanctions on Belarusian fertiliser exports. The goal would be to reduce Minsk’s dependence on Russia. This shows that the issue is not limited to the battlefield—it equally involves the economy and trade.

It is often in moments like these that risk gets mispriced. The market assumes one conflict is partially fading because its attention shifts to another. Escalation involving Belarus would therefore be not only a military event, but also a narrative shock for investors.

Does Belarus have a real capacity to attack?

Despite rising risk, Belarus’s practical capabilities remain limited. The Belarusian armed forces are small and in a state of partial decay. Russia, in turn, no longer has the reserves that would allow it to easily man an additional several hundred kilometres of border.

The terrain between Belarus and Ukraine is very difficult. Dense forests, swamps, rivers, and a limited number of paved roads significantly hinder rapid manoeuvre. One of the key routes runs through the Chernobyl exclusion zone.

Over years of war, Ukraine has heavily fortified its northern border. An attempt to break through could end in disaster for Belarus and the Russians. Therefore, Belarus entering the war would not necessarily mean an effective offensive.

For Russia, however, escalation via Belarus could be an attempt to force political, diplomatic, and military concessions before it loses initiative or the ability to conduct controlled escalation.

What would this mean for the market?

For financial markets, Belarus directly entering the war would primarily be a signal of escalation in a conflict that some investors have already considered partially de-escalated or on a path toward ending.

The reaction could be quick, although its scale would depend on actual military actions.

The most likely effects are:

- A fall in bond prices in the region and an increase in the geopolitical risk premium,

- Pressure on Central and Eastern European currencies, including the Polish zloty.

- A strengthening of the US dollar as a “safe-haven” currency.

- A sell-off in stock indices, especially local ones.

- A return of capital to defence companies, especially those that have seen large declines in recent months.

Low probability, high risk

Belarus entering the war is still not the base-case scenario. The risk remains constrained by the weakness of the Belarusian army, difficult terrain, Ukrainian fortifications, and potentially very high political costs for the regime in Minsk.

That does not mean the topic can be ignored. Belarus would not have to win a single battle to change the geopolitical and market context.

Kamil Szczepański

Financial Markets Analyst at XTB

Oil rises over 3% 🛢️

Defense sector ahead of earnings: Summary

🛢️Brent Crude Oil Tests $95 per Barrel

Morning Wrap: AI companies and gold back in favour? (22.07.2026)

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.