- US stock markets gain at Thursday's opening

- The increases are supported by declines in the USD dollar

- Yields on 10-year bonds are also falling

Today's market sentiment is definitely better than in previous days. The first trading sessions of the new month and quarter were bearish, and today investors can expect a slight rebound. The US500 opens 0.60% higher, and the US100 0.80% higher. The indices thus recover a larger part of the decline from the previous days. The outlook for April may be mixed. It should be remembered that April 15th is the final deadline for paying taxes on 2023 profits, which usually correlates with somewhat higher selling pressure. On the other hand, we won't have to wait long for a catalyst for a bigger move, as the NFP labor market report is scheduled for publication tomorrow. From the Fed's point of view, this is an important report, and a publication far from consensus can affect volatility in the indices and forex.

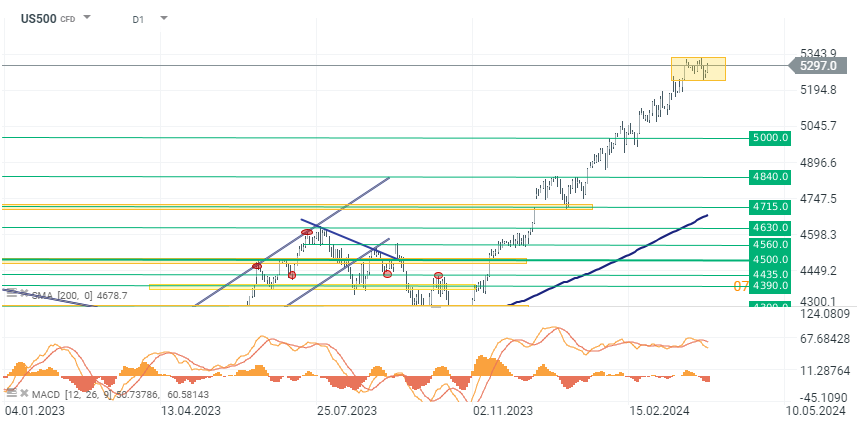

US500

Contracts on the main SP500 index gain 0.60% and are again approaching levels above 5300 points. Quotations in the 5250-5340 point zone have been consolidating for over two weeks. The market is consolidating in anticipation of the NFP data on the number of employed people in the USA.

Source: xStation 5

Company News

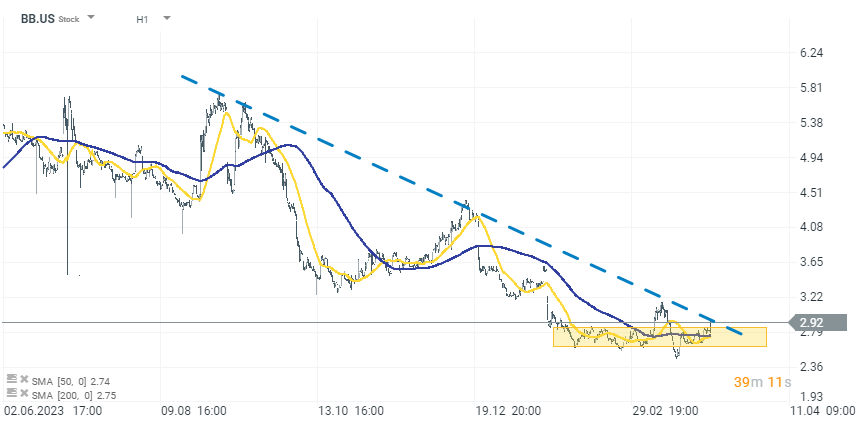

BlackBerry (BB.US) gains 4% after the company reported Q4 results that exceeded expectations. Despite that, the company's guidelines were below market expectations, projecting 1Q25 sales between $130M and $138M (below the consensus of $151.85M), and adjusted EPS for the quarter between -$0.04 and -$0.06 per share (below the consensus of -$0.03).

Conagra Brands (CAG.US) gains almost 5% after reporting a profit beat for FQ3 2024 and raising its fiscal adjusted operating margin guidance. Despite a 1.7% Y/Y decline in quarterly net sales to $3.03B and a 2% decrease in organic net sales, Conagra's performance was buoyed by U.S. consumers eating more at home.

Levi Strauss (LEVI.US): surges over 16% after the company surpassed Q1 expectations and raised its profit outlook. Levi Strauss reaffirmed its revenue growth outlook for the year at +1% to +3%, aligning with the consensus growth of 2.4%. It also increased its FY2024 EPS guidance range to $1.17 to $1.27, up from the prior range of $1.15 to $1.25 and above the $1.22 consensus.

Lamb Weston (LW.US) fell over 15% following a top and bottom line miss in FQ3 2024. The disappointing results were attributed to issues arising from a transition to a new ERP system in North America, which affected the company's ability to fill customer orders, impacting sales volume and margin performance. Consequently, Lamb Weston cut its fiscal 2024 net sales guidance from $6.8B-$7B to $6.54B-$6.60B.

Block (SQ.US) dropped almost 3% after Morgan Stanley downgraded the stock to Underweight from Equal-weight and lowered the price target to $60 from $62 (currently $77). The downgrade reflects concerns that the market is overestimating growth potential for its Cash App and Square business.

Ford (F) announced a delay in the launch of its all-new three-row EVs in Oakville, Ontario, from 2025 to 2027. Ford will focus on hybrid vehicles and plans to offer hybrid options across its North American lineup by the end of the decade. This move reflects the broader challenges in the automotive industry in adopting EVs.

Daily Summary: Semiconductors Rise in the Shadow of Geopolitical Turmoil

Did SaaS lost too much? Morgan Stanley says yes.

Tech sector catches its breath 🚀

US OPEN: Semiconductors drive a rebound

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.