- PPI inflation highest since December 2022.

- All measures place considerably above expected levels.

- EUR/USD reaction very muted.

- FOMC rate hike by year-end roughly 40% priced-in.

- PPI inflation highest since December 2022.

- All measures place considerably above expected levels.

- EUR/USD reaction very muted.

- FOMC rate hike by year-end roughly 40% priced-in.

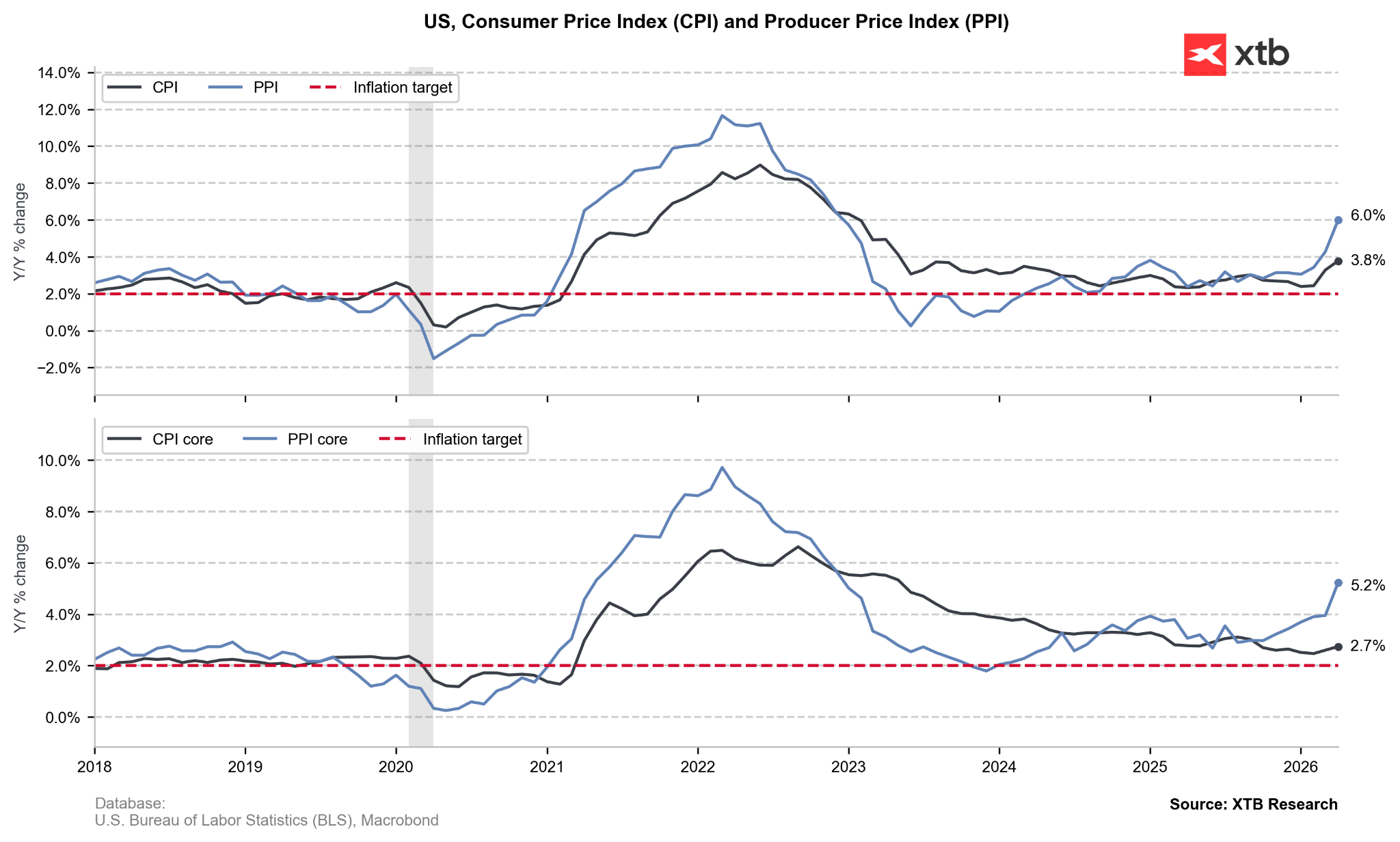

The April reading has shown the sharpest increase in producer prices since 2022. The increase is, naturally, largely due to higher petrol prices. That said, the core measure, stripping off food and energy, has also picked up significantly, up to 5.2%.

Figure 1: US CPI & PPI Inflation (2018 - 2026)

Source: XTB Research, 13.05.2026

Source: XTB Research, 13.05.2026

All of the readings represent a major upward surprise, placing considerably above expected levels.

- PPI Inflation [YoY]: 6.0% (vs. 4.8% consensus)

- PPI Inflation [MoM]: 1.4% (vs. 0.5%)

- Core PPI Inflation* [YoY]: 5.2% (vs. 4.3%)

- Core PPI Inflation* [MoM]: 1.0% (vs. 0.3%)

- Super-Core PPI Inflation** [YoY]: 5.2% (vs. 4.3%)

- Super-Core PPI Inflation** [MoM]: 1.0% (vs. 0.3%)

* Excluding food and energy.

* Excluding food, energy and trade services.

A 3% monthly increase in airfares is perhaps the most striking when looking at detailed data. Some categories have, however, surprised to the downside, with hospital care up roughly 0.1% MoM and portfolio management down 2.4%.

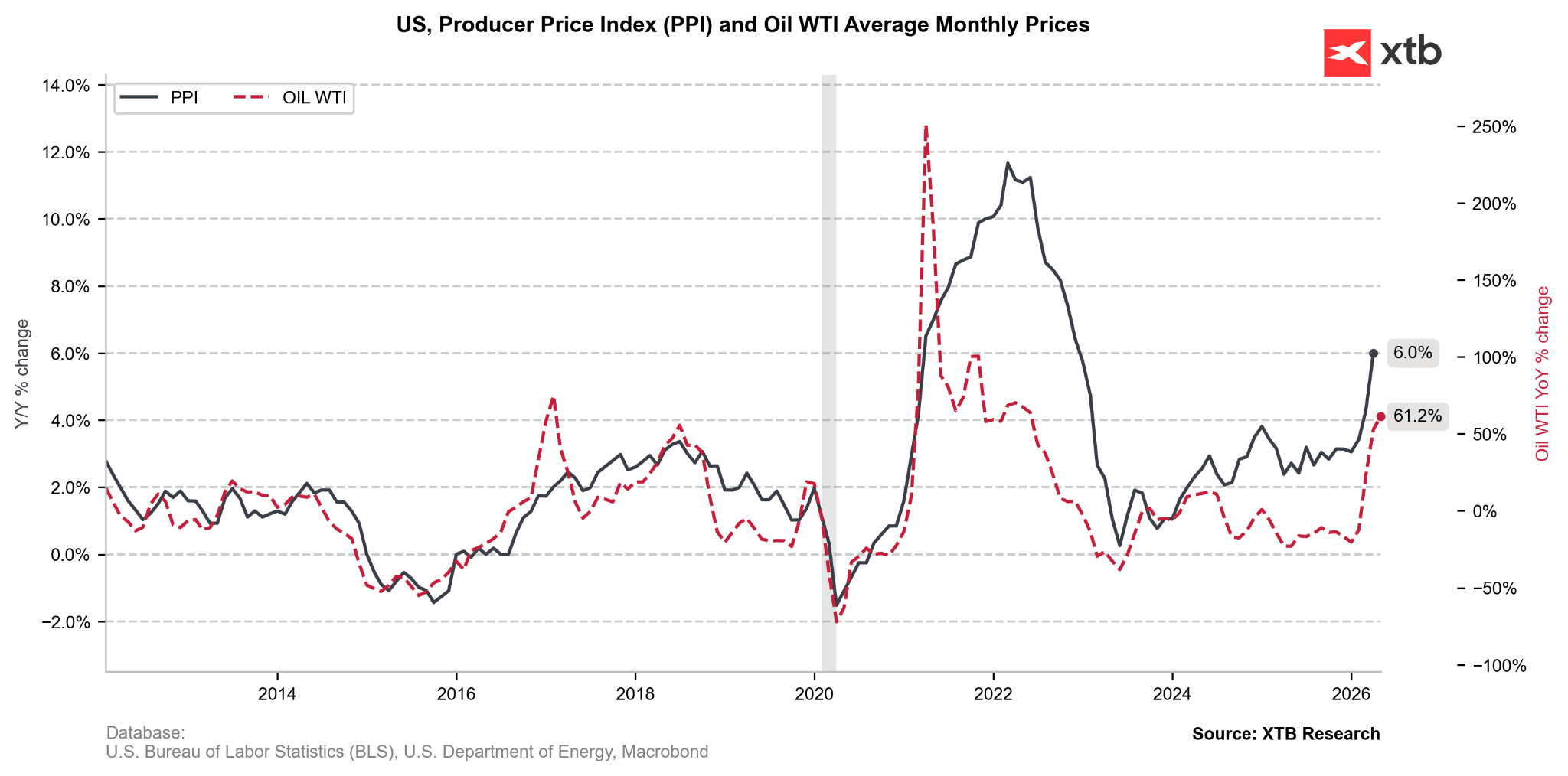

Figure 2: US PPI Inflation and WTI Oil (2012 - 2026)

Source: XTB Research, 13.05.2026

Source: XTB Research, 13.05.2026

The reaction of the EUR/USD is, rather surprisingly, very muted, with the pair flat after the release and down 0.3% on the day, likely due to little to none positive information regarding the developments in the Middle East. We also see very timid swings in S&P 500 futures.

Markets slightly increased their bets for FOMC interest rate hikes, such a move happening before the year-end is still not the base scenario, however (roughly 40% priced-in). We have also seen a further pick-up in US 10-year bond yields, up to 4.48%, not seen since July.

—

Michał Jóźwiak

Financial Markets Analyst at XTB

michal.jozwiak@xtb.com

Daily Summary: Wall Street Regains Ground; Another Intervention in the Yen Market❓

Three Markets to Watch Next Week (July 31, 2026)

Market Wrap: European equities at 3-week highs! Apple dips in US premarket!

Euro Area core inflation above estiamtes! EURUSD under key resistance!

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.