Over the past weeks, the number one topic has undoubtedly been central banks and inflation. Investors are now wondering if, after a cycle of interest rate hikes around the world, the markets are approaching the so-called Pivot, i.e. a slowdown in the pace of such rapid tightening and a turnaround in the rhetoric of central bankers. Tomorrow it's time for the Fed. CPI inflation in the US has strengthened the chances of a dovish move by the Fed. Let's look at the key points to better prepare for tomorrow's FOMC meeting.

The biggest drop in CPI inflation since April 2020!

CPI inflation came in clearly below expectations. The main surprise is the decline in core inflation. For core inflation, the energy contribution weakens: from 1.3 points to 1.0 points. The commodity contribution also weakens, from 1.1 points to 0.8 points. The data may suggest that the peak in inflation is behind us, which may support the recent change in rhetoric from the Fed. Also noteworthy is the small increase in monthly inflation. Source: Bloomberg

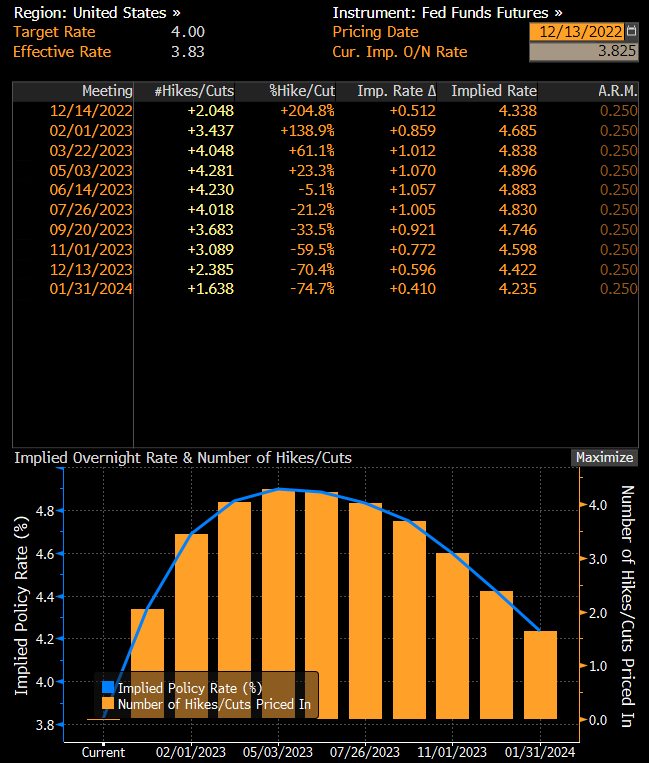

FOMC will raise rates

A hike at tomorrow's meeting is more than certain. The market is currently discounting a 50 basis point hike at tomorrow's FOMC meeting. This path also seems to be confirmed by swaps, which point to an almost 100% chance of a 50 basis point hike. What does this mean? The market is set for decisive Fed action. This scenario also seems to be confirmed by analysts surveyed by the agency. Source: Bloomberg

What will the dot-plot show?

It is worth remembering that in December we will get a new dot-plot (published quarterly), where members will convey their current expectations for the path of interest rates. September's forecast pointed to a median of around 4.6% The forward rate is now projected to jump to 4.8% - 5.0%. If the Fed raises rates tomorrow by the predicted 50 points, and the marginal rate is not raised above 5.0%, we will be close to the expected marginal rate, which could further strengthen market bulls. Source: Bloomberg

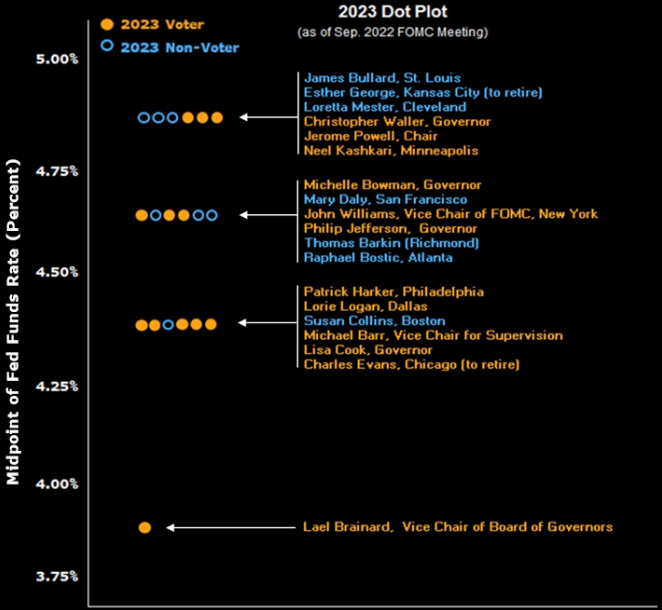

What awaits us in 2023?

The composition of the voting committee changes quite a bit next year. This year it was very hawkish, and next year it becomes decidedly more "dovish" taking likely interest rate expectations. Remember, however, that ultimately the decision is made by the chairman, the members can only express a dissenting opinion - but this has not happened recently. Source: Bloomberg

Market behavior after CPI inflation reading

The US500 index broke sharply above the long-term downtrend line after the publication of the CPI reading. The nearest resistance is at the level of 4175 points, where there is a barrier set by the Fibonacci measure and the upper limit of the technical 1:1 structure. Source: xStation 5

Daily Summary: Markets limit the pullback while awaiting the Fed

France Challenges Palantir, Market Reacts.

The semiconductors sell-off continues 📉

US OPEN: Deeper sell-off and a SaaS rebound

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.