Your savings rate matters more than your salary because it decides how many years of your life you’re buying back with each year you work. Sure, income helps, but the real driver of financial freedom is what you keep, not what you make. Returns, inflation, taxes, and the occasional “I deserve this” spending spree all matter, but the math itself is simpler than people think. Once it clicks, financial freedom stops feeling like a rich-person club and starts feeling like a plan.

Your savings rate matters more than your salary because it decides how many years of your life you’re buying back with each year you work. Sure, income helps, but the real driver of financial freedom is what you keep, not what you make. Returns, inflation, taxes, and the occasional “I deserve this” spending spree all matter, but the math itself is simpler than people think. Once it clicks, financial freedom stops feeling like a rich-person club and starts feeling like a plan.

What Is Financial Freedom?

Financial freedom means having enough invested assets to cover your living expenses without relying on active work. In practical terms, your portfolio produces enough income or sustainable withdrawals to fund your lifestyle. That income might come from stocks, ETFs, dividends, real estate, or even a business you built years ago. The structure can vary. The core idea is simple: your survival is no longer tied to your next paycheck.

It is just as important to define what financial freedom is not. It is not yachts, viral success, or a social media highlight reel. It does not automatically mean retiring at 35 or abandoning ambition. In fact, many financially independent people keep working. They build companies, trade markets, invest or consult part-time. The difference is subtle but powerful. They work because they want to, not because the mortgage demands it.

Financial freedom matters because it gives you leverage over your own time. When your essential expenses are covered, conversations change. You negotiate differently. You tolerate less nonsense. You can leave a job that drains you or take a calculated risk that once felt reckless. That psychological shift is hard to quantify, but anyone who has experienced it will tell you the same thing: reduced financial pressure creates clearer thinking.

There are also persistent myths that stop people before they even start. It helps to confront them honestly:

- “You need to be a millionaire.” The real number depends on your spending, not on a round net worth milestone. A modest lifestyle requires far less capital than social media implies.

- “Only high earners can achieve financial independence.” Income helps, but savings rate and disciplined investing often matter more than headline salary figures.

- “It requires extreme frugality.” Sustainable progress usually comes from conscious spending, not from living like you are permanently grounded.

- “You must retire early to call it success.” Financial freedom is about flexibility, not about quitting work at a specific age.

Once these myths fall apart, the concept becomes less intimidating. It stops looking like a fantasy reserved for startup founders or hedge fund managers. It starts to look like a structured, math-driven strategy built on expenses, savings behavior, and time…And time, whether we plan for it or not, keeps moving.

Why Your Savings Rate Matters More Than Your Salary

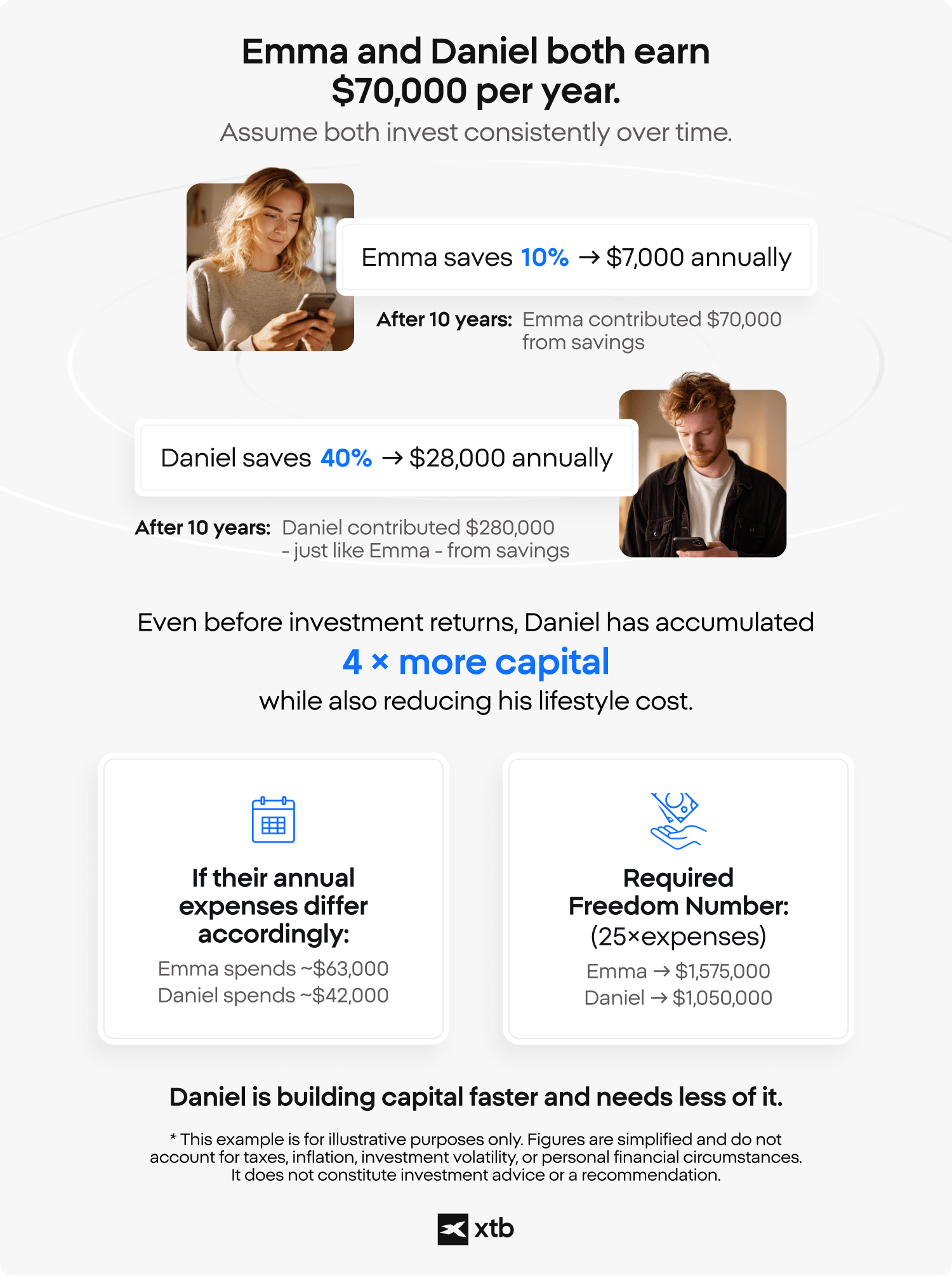

Your savings rate matters more than your salary because every year you save aggressively is a year of freedom you buy in advance. If you earn $50,000 and save $25,000, you are not just “being responsible.” You are effectively prepaying half a year of your lifestyle. Do that consistently, and something interesting happens. Financial independence is built by how much of your life you pre-fund, not by how impressive your income sounds.

The real engine behind this is compound interest. When you invest your savings, returns begin generating additional returns, and over time the curve stops behaving politely. It bends. In the early years, it can feel slow, almost underwhelming. Then momentum builds. That snowball analogy is overused, but it works for a reason. Moderate earners who consistently invest often outpace high earners who increase their lifestyle every time their salary rises. The market rewards consistency more than ego.

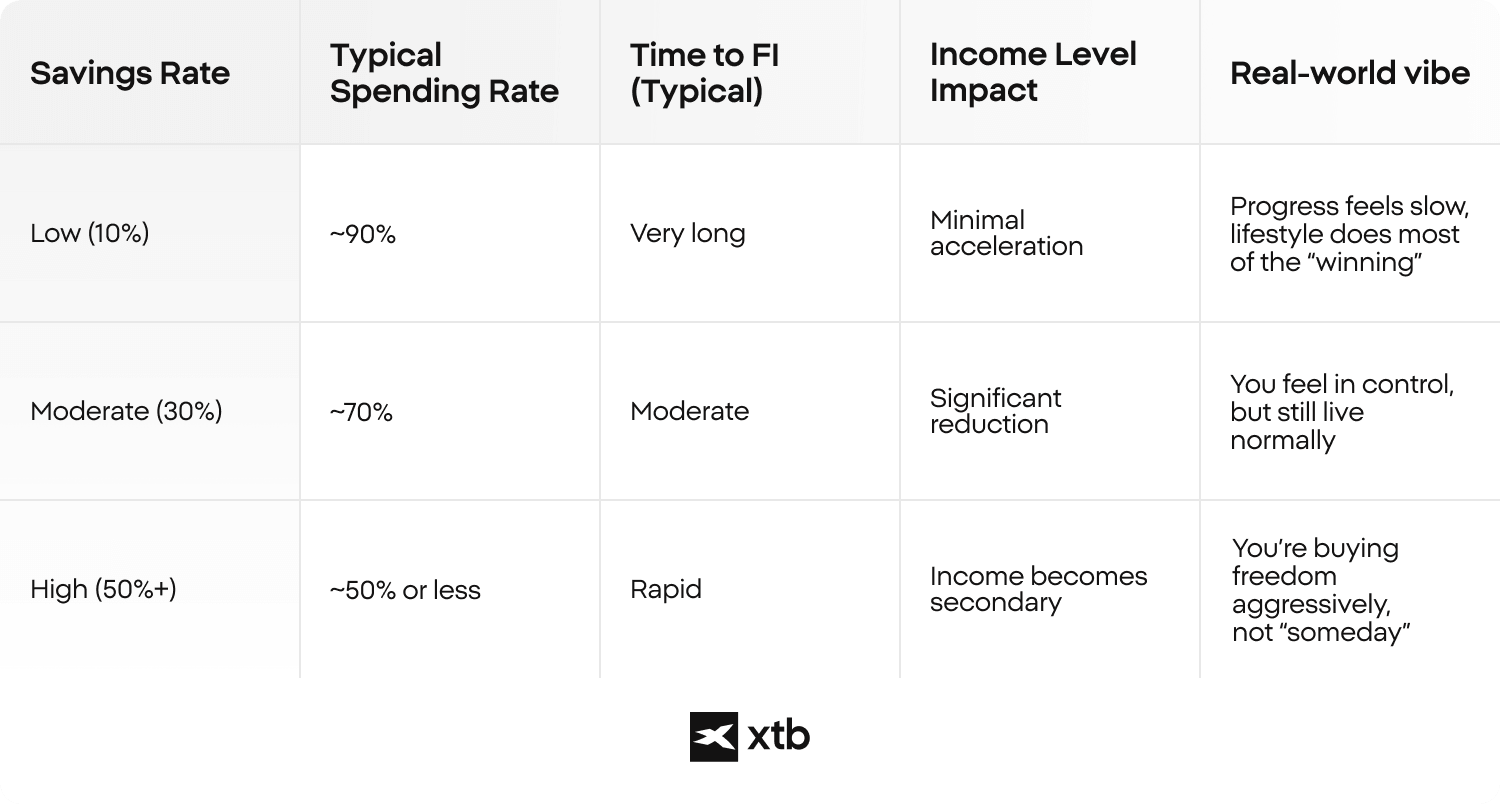

Here’s the part most people underestimate: timeline compression. Increasing your savings rate does not reduce your time to financial freedom in a neat, linear way. It shrinks aggressively. Moving from saving 10% to 20% helps. Moving from 20% to 50% changes the entire equation. At very high savings rates, the sheer speed at which you accumulate capital starts to matter more than marginal improvements in returns. Small percentage changes in savings today can translate into years of regained time later.

Savings Rate vs Income Impact on Time to Financial Independence

At higher savings rates, you’re not just investing more, you’re also reducing the amount your future portfolio needs to support, which is why the timeline shrinks so fast. Look closely at that dynamic. Someone earning $70,000 and saving half of it often reaches independence sooner than someone earning $150,000 and saving 15%. Income can speed the process up, but savings rate determines how aggressively you are moving toward the finish line.

DID YOU KNOW?

Many people believe that financial stability is reserved only for the wealthy. According to the "Financial Health of Europeans" report (September 2025), 1 in 3 Europeans shares the view that only very rich people can achieve financial health.

The level of optimism varies significantly across the continent:

- Most pessimistic: Swedes (43% believe stability is only for the rich).

- Most optimistic: Italians (only 23% hold this view).

Source: EFPA, Financial Health of Europeans Quantitative Research Report, September 2025.

How Much Money Do You Need for Financial Freedom?

You need enough money for financial freedom to cover your annual expenses, not to hit some shiny “net worth milestone.” Financial independence is not about becoming rich - it’s about making your assets large enough to replace your spending. The real question is not “How much money do I want?” but rather “How much capital do I need so my investments can fund my lifestyle?”

That’s where the so-called Rule of 25 and the 4% Rule come in. In reality, they are two sides of the same idea.

Historically, diversified portfolios have often been able to support withdrawals of around 4% per year over long periods without immediately depleting capital. If you flip that percentage mathematically, you get the origin of the “25”:

4% = 0.04

1 ÷ 0.04 = 25

So multiplying your annual expenses by 25 is simply the inverse of assuming a 4% withdrawal rate. It’s not a random number. It’s just the math behind turning spending into required capital.

If you spend $40,000 per year, you multiply it by 25 and get $1,000,000. At a 4% withdrawal rate, that portfolio could generate roughly $40,000 annually. Spend $60,000, and the rough target becomes $1.5 million. The formula works in both directions: either multiply expenses by 25, or calculate 4% of your portfolio. Same concept, different entry point.

The important part is the mindset. This is not a promise, and it’s not a guarantee of future performance. It’s a planning baseline - a way to translate lifestyle costs into a capital target. The Rule of 25 doesn’t predict the future. It simply helps you anchor your goal in a rational framework instead of chasing an arbitrary net worth number

EXAMPLE

Let’s say your annual expenses are $50,000. Using the Rule of 25, you get $50,000 × 25 = $1,250,000. A 4% withdrawal on $1.25M is $50,000 a year, which matches your spending. On paper, that’s the “financially free” point. In real life, you’d still want flexibility because markets don’t send calendar invites before they fall.

The last piece is adjusting for inflation and market risk. Inflation slowly raises your cost of living, and downturns can shrink your portfolio at uncomfortable times, especially early in retirement. Your financial freedom number is an estimate, not a guarantee. That’s why many investors build a buffer, aim a bit above 25×, or keep spending adjustable so they’re not forced into bad decisions when conditions change.

The Stages of the Financial Freedom Journey

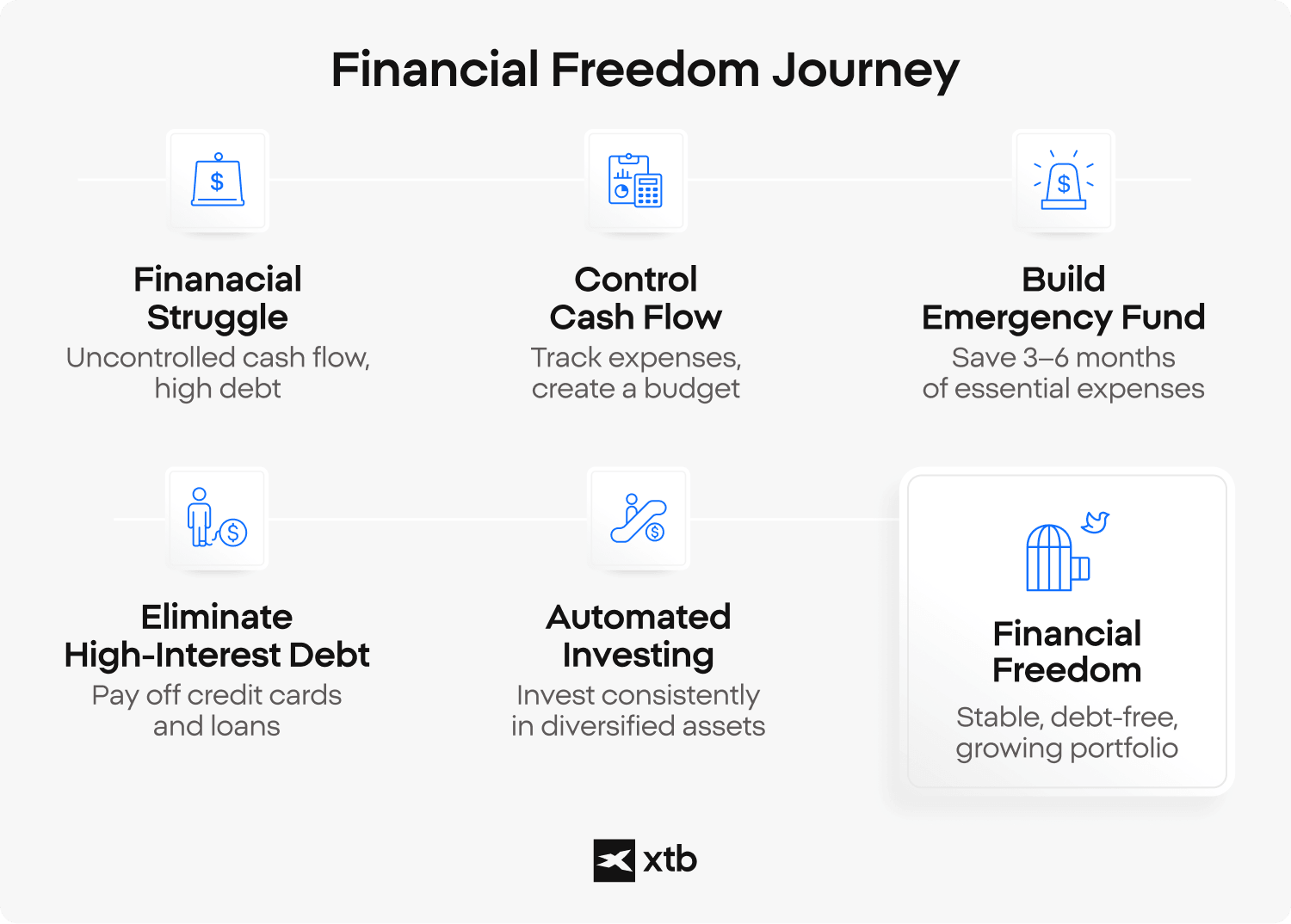

Financial freedom usually unfolds in stages. If you know what stage you’re in, you stop trying to “optimize everything” and start doing the one thing that actually moves the needle right now.

- Gaining control of your cash flow starts with tracking expenses and using a realistic budget. When you can see where the money goes each month, saving stops being a vague intention and becomes a set of decisions you can actually repeat.

- Building an emergency fund creates stability before you scale investing. Setting aside three to six months of essential expenses helps you handle life surprises without selling investments at a bad moment or reaching for expensive credit.

- Eliminating high-interest debt removes a silent drag on your progress. Learning how to get out of debt, especially credit card debt, often delivers a guaranteed “return” equal to the interest rate you stop paying. That is one of the few wins in finance that comes with no market risk.

- Automated investing and scaling contributions turns discipline into a system. With automated investing into diversified assets, your portfolio grows quietly in the background, and as income rises, scaling contributions instead of lifestyle inflation can accelerate financial independence more than most people expect.

A Solid Foundation: Debt, Budget, and Financial Cushion

Before you worry about returns, optimize stability. Real financial freedom is built on controlled cash flow, manageable debt, and a cushion that keeps you from making desperate decisions when life inevitably throws something at you. This part is not glamorous. Nobody brags about their emergency savings at dinner. But it quietly determines whether your plan survives its first real test.

How to Get Out of Debt Strategically

High-interest debt is one of the biggest obstacles to becoming financially independent. A credit card charging 20% interest is not neutral. It is actively working against you every single day, even while you sleep. Eliminating high-interest debt is often the highest guaranteed return you will ever earn.

Start by listing every debt with its balance and interest rate. Not in your head. On paper. When you see the numbers clearly, they stop feeling abstract. Many people choose the avalanche method, attacking the highest interest rate first. Others prefer the snowball method, paying off smaller balances quickly for psychological momentum. Both work. What matters is consistency.

And during this phase, avoid new consumer debt unless absolutely necessary. Financial freedom and lifestyle inflation rarely move in the same direction.

Why a Budget Planner Changes Everything

A budget planner is not about restriction. It is about awareness and control. Most people resist budgeting because they imagine spreadsheets, guilt, and cutting every small pleasure. In reality, budgeting simply answers one question: where is my money actually going?

Track fixed expenses. Track variable spending. Set a savings target. That’s enough to start. You do not need advanced software unless you enjoy it. Clarity creates leverage. Once you can see your financial patterns, increasing your savings rate becomes a tactical adjustment, not an emotional struggle.

And here is the quiet benefit: budgeting exposes small leaks. Subscriptions you forgot about. Dining habits that slowly expanded. Lifestyle upgrades that happened without a conscious decision. Awareness alone often corrects more than strict rules ever could.

Building a Financial Cushion That Protects Your Freedom

A financial cushion, sometimes called a safety net, protects your independence plan from collapsing during volatility. It is separate from your long-term investments. It is liquid, stable, and intentionally boring.

Most disciplined investors keep three to six months of essential expenses in easily accessible accounts. Some hold more if income is variable or entrepreneurial. The goal is simple: never be forced to sell investments during a downturn just to cover a short-term problem.

Markets fluctuate. Jobs change. Cars break down at inconvenient times. A financial cushion absorbs shocks so your long-term strategy does not have to.

Without it, every surprise feels like a threat to your progress. With it, downturns become uncomfortable, not catastrophic.

Where Does the Money Grow?

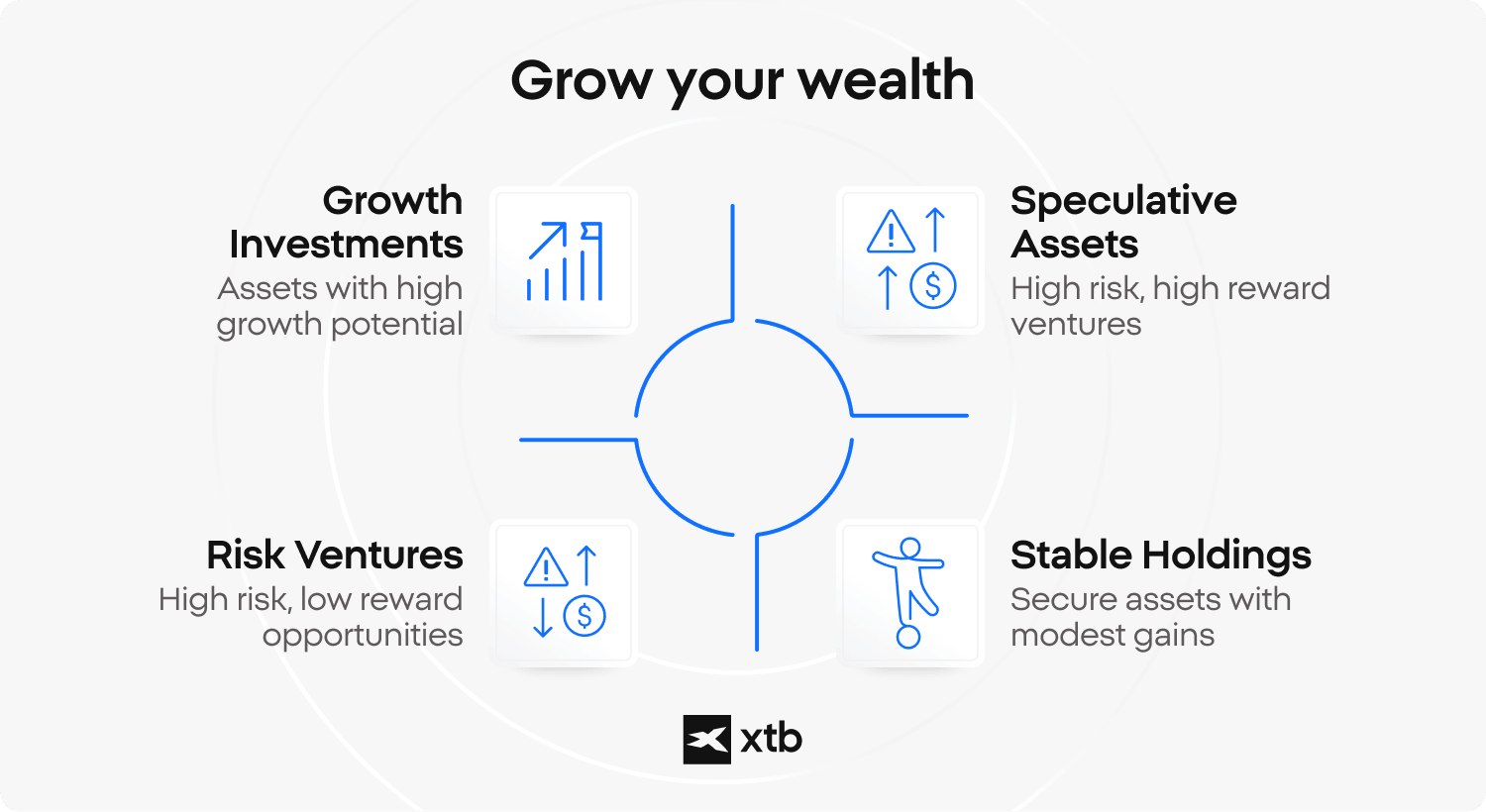

Once your savings rate is working and your system is stable, the next question is pretty practical: where should the money actually grow? Financial freedom is funded by productive assets, not by cash sitting idle and slowly getting chewed up by inflation. The goal is to own things that can expand over time, even if the ride gets bumpy.

- Stocks are the long-term growth engine because they represent ownership in real businesses. When companies grow revenues, raise prices, innovate, and compound profits, shareholders tend to benefit. The short term can be chaotic, but over decades, equities have historically done the heavy lifting. However, stocks are very volatile and may lead not only to capital gains but also substantial loses.

- ETFs and so-called index funds give you diversification without needing to play stock picker every weekend. Instead of betting your future on one company, you buy a slice of whole markets across sectors and regions. For most people, broad ETFs are the backbone of a sensible passive investing plan. Investing is always risky - ETFs do not guarantee positive investing returns.

- Dividends add a cash flow element that can feel reassuring, especially as you approach financial independence. Some investors use dividends for income, others reinvest them to speed up compounding. Either way, dividends can be a helpful component, as long as you do not treat them like guaranteed rent checks.

- Passive investing strategies work because they reduce the two big enemies of results: high fees and emotional decisions. A systematic approach, investing regularly into diversified funds, is not flashy, but it is brutally effective over long periods. If you want your plan to survive real life, boring is often your friend.

- Bonds can improve stability and reduce overall portfolio swings. Returns are usually lower than stocks, but bonds may cushion downturns and make withdrawals feel less stressful later on. Think of them less as a growth rocket and more as suspension on a rough road.

Risks of Financial Independence

Financial independence is empowering, but it comes with real risks you need to plan around. The goal is not to fear these risks, it’s to make sure they can’t knock you off the path the moment life or markets get messy.

Market downturns are unavoidable. Even the best portfolios go through periods where values drop fast and headlines get dramatic, sometimes for months. Volatility is a normal price of admission for long-term returns. The practical question is whether you have a plan that still works when your portfolio is down and your confidence is wobbling.

Sequence of returns risk is the one that surprises people, especially right after they hit “freedom.” If the market falls hard early in retirement, and you’re withdrawing at the same time, you can do lasting damage to the portfolio. It’s not just the decline that hurts, it’s the combination of declines plus withdrawals while the account is already shrinking.

CAUTION: Panic selling can permanently damage your portfolio

Retiring into a downturn can feel like finally reaching the finish line, then realizing the track has moved. Withdrawing heavily during falling markets can reduce the capital base that a recovery needs to rebuild. This is why many financially independent investors keep a cash buffer or adopt flexible spending so they are not forced to sell at the worst possible moment.

Inflation risk is quieter, but it never takes a day off. If your costs rise faster than expected, your “freedom number” stops feeling so free. A portfolio built only for stability may struggle to keep up over long time horizons, which is why growth assets still matter even after you reach independence.

Behavioral risk and lifestyle inflation are the most personal threats. People panic sell in downturns, chase what’s already pumped, or slowly upgrade their lifestyle until the finish line moves further away. Discipline is the part nobody can outsource. The market will do what it does, but your habits decide whether your plan survives it.

First Steps: What To Do If You’re Starting Today

If you’re serious about becoming financially free, the starting point usually isn’t a stock tip or a crypto trade. It’s clarity, the boring kind that quietly changes everything. People keep Googling what is financial freedom or what is financial independence, but the real switch flips when the financial freedom definition becomes your own numbers, on your own calendar, in your own bank account.

- Calculate your monthly expenses. Track what you actually spend for a full month, not what you hope you spend. This is where the whole plan begins, because independence is always built on lifestyle costs.

- Determine your annual spending. Multiply your monthly number by twelve, then sanity-check it for one-offs like travel, insurance, gifts, car repairs, the annoying stuff that happens every year whether we plan for it or not.

- Estimate your Freedom Number using the 25× rule. Take your annual expenses and multiply by 25. It’s a simple way to translate “financial independence” from a motivational phrase into a concrete target.

- Set a realistic savings rate. Pick a percentage you can hold through good months and bad months. A lower rate you maintain beats an ambitious rate you abandon after two weeks of “new me” energy.

- Start automated investing. Set it up so money moves on payday, before you can talk yourself out of it. Automated investing is like brushing your teeth: not exciting, but skipping it for long enough gets expensive.

- Increase your savings rate gradually. When income rises, try to capture at least part of it for investing before lifestyle inflation grabs it. A few percentage points here and there feels small, but over years it becomes a different life.

Becoming financially free isn’t about doing everything perfectly. It’s about stacking a few smart habits and repeating them long enough for time and compounding to do the heavy lifting.

Key Takeaways

- Savings rate shapes your timeline more than income level. A high earner who saves little may stay dependent for decades, while a moderate earner with disciplined habits can reach independence far sooner.

- The Rule of 25 and the 4% Rule turn freedom into a number. Multiply annual expenses by 25 to estimate the portfolio size needed to sustain your lifestyle.

- Raising your savings rate compresses time dramatically. Moving from 10% to 40% is not a small upgrade, it can redefine your entire trajectory.

- Consistency and risk awareness outperform perfection. Long-term discipline usually beats chasing the next “ideal” investment strategy.

FAQ

Financial freedom is when your investments pay your bills so your job becomes optional. Not irrelevant. Optional. You can still work, build things, trade markets, start projects. But you’re no longer working because you have to. That psychological shift changes everything.

Most people use the terms interchangeably. Technically, financial independence refers to the math. Your assets generate enough income to sustain you. Financial freedom is what that math feels like in real life. Less pressure. More choice. Same foundation, different emphasis.

At its core, it’s based on two numbers: your annual expenses and a sustainable withdrawal rate. Multiply your yearly spending by 25 and you get a practical benchmark. It’s not magic. It’s simply aligning capital with lifestyle.

You control what you keep more than what you earn. Raise your savings rate gradually. Avoid lifestyle creep. Invest consistently in diversified assets. Average salaries with above-average discipline often outperform high salaries with careless spending.

Freedom of time. Lower stress. The ability to say no. That’s huge. When your survival doesn’t depend on your boss, your confidence changes. Your decision-making improves. You stop reacting and start choosing.

Yes, if you treat it like a guarantee. No, if you treat it like a guideline. Markets move. Inflation fluctuates. Flexibility matters. The rule works best when combined with margin of safety and adaptable spending.

There’s no perfect number, but 30% to 50% is common among people who reach independence earlier than average. The key insight is this: every 5% increase in savings rate does more than you think. It compounds in time saved.

Start with what you actually spend in a year, not what you wish you spent. Multiply it by 25. That’s your rough independence target. From there, adjust based on risk tolerance and lifestyle flexibility.

It can be. Growth assets are important, especially early on, but emotional tolerance matters just as much as expected returns. If volatility makes you panic, your strategy is too aggressive. A plan only works if you can stick with it.

It removes drama. No second-guessing. No waiting for the “perfect” entry. Money moves into investments whether headlines are optimistic or chaotic. Over time, that consistency quietly builds wealth.

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.