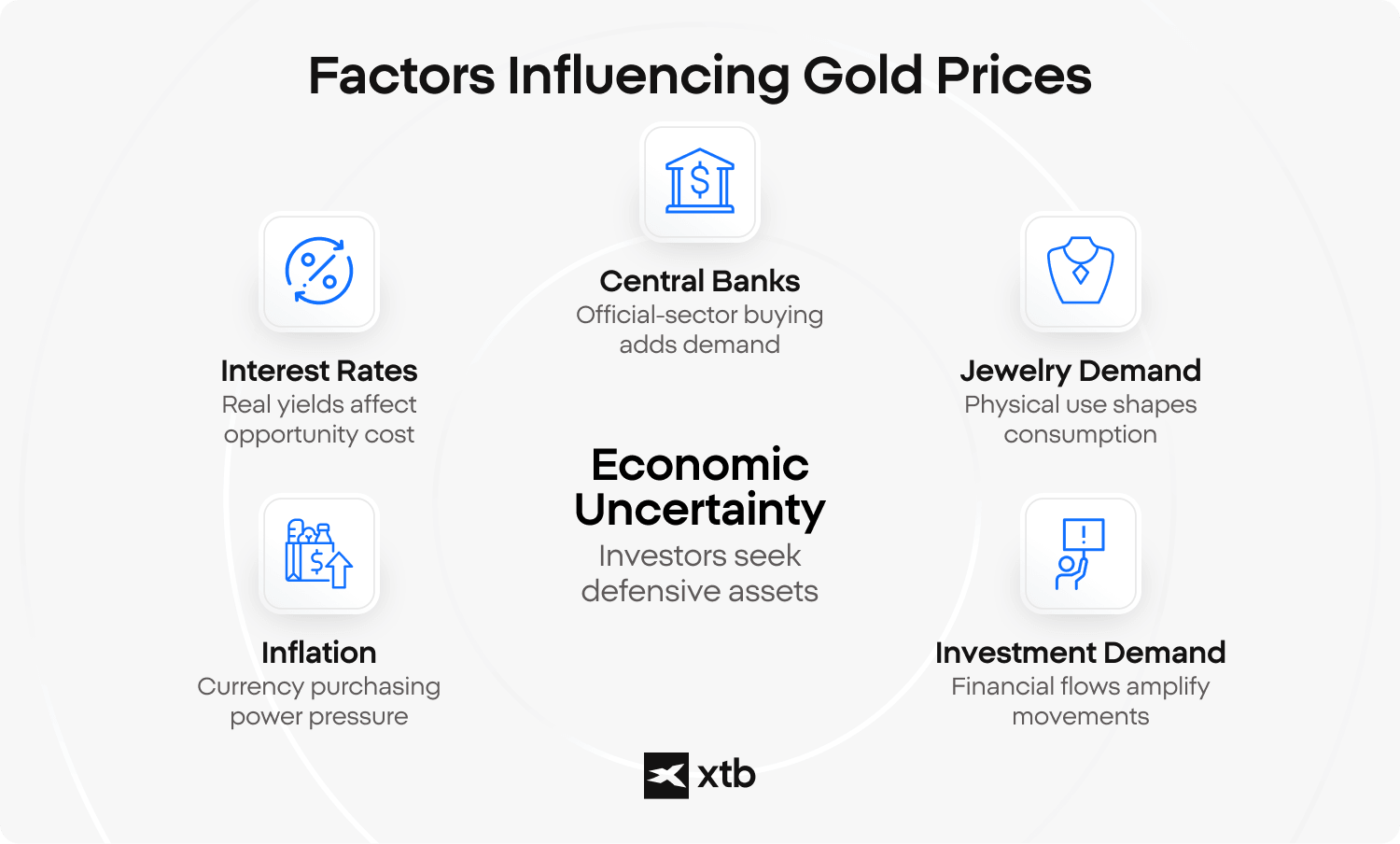

Gold prices are shaped by six main forces: economic uncertainty, inflation, real interest rates, central bank demand, physical consumption, and investment flows. No single factor explains every move, because gold usually reacts to several market forces at once. This means there is rarely one simple answer to what affects gold prices, because the same price move can reflect both defensive demand and changing expectations about currencies, rates, or global risk. Understanding these six forces helps explain what drives the price of gold without treating gold as a guaranteed hedge or an investment recommendation.

Gold prices are shaped by six main forces: economic uncertainty, inflation, real interest rates, central bank demand, physical consumption, and investment flows. No single factor explains every move, because gold usually reacts to several market forces at once. This means there is rarely one simple answer to what affects gold prices, because the same price move can reflect both defensive demand and changing expectations about currencies, rates, or global risk. Understanding these six forces helps explain what drives the price of gold without treating gold as a guaranteed hedge or an investment recommendation.

- Economic uncertainty - demand may rise when investors seek assets perceived as more defensive.

- Inflation - gold is often monitored when currency purchasing power is under pressure.

- Interest rates - real yields affect the opportunity cost of holding a non-yielding asset.

- Central bank reserves - official-sector buying can add large structural demand.

- Jewelry and technology demand - physical use shapes part of global gold consumption.

- Investment demand and ETFs - financial flows can amplify short-term price movements.

Key takeaways

- Gold prices are influenced by more than geopolitics alone. Inflation, rising public debt, and declining purchasing power of fiat currencies can increase long-term demand for gold, which cannot be created by monetary policy decisions, although short-term volatility is still heavily influenced by speculation and ETF flows.

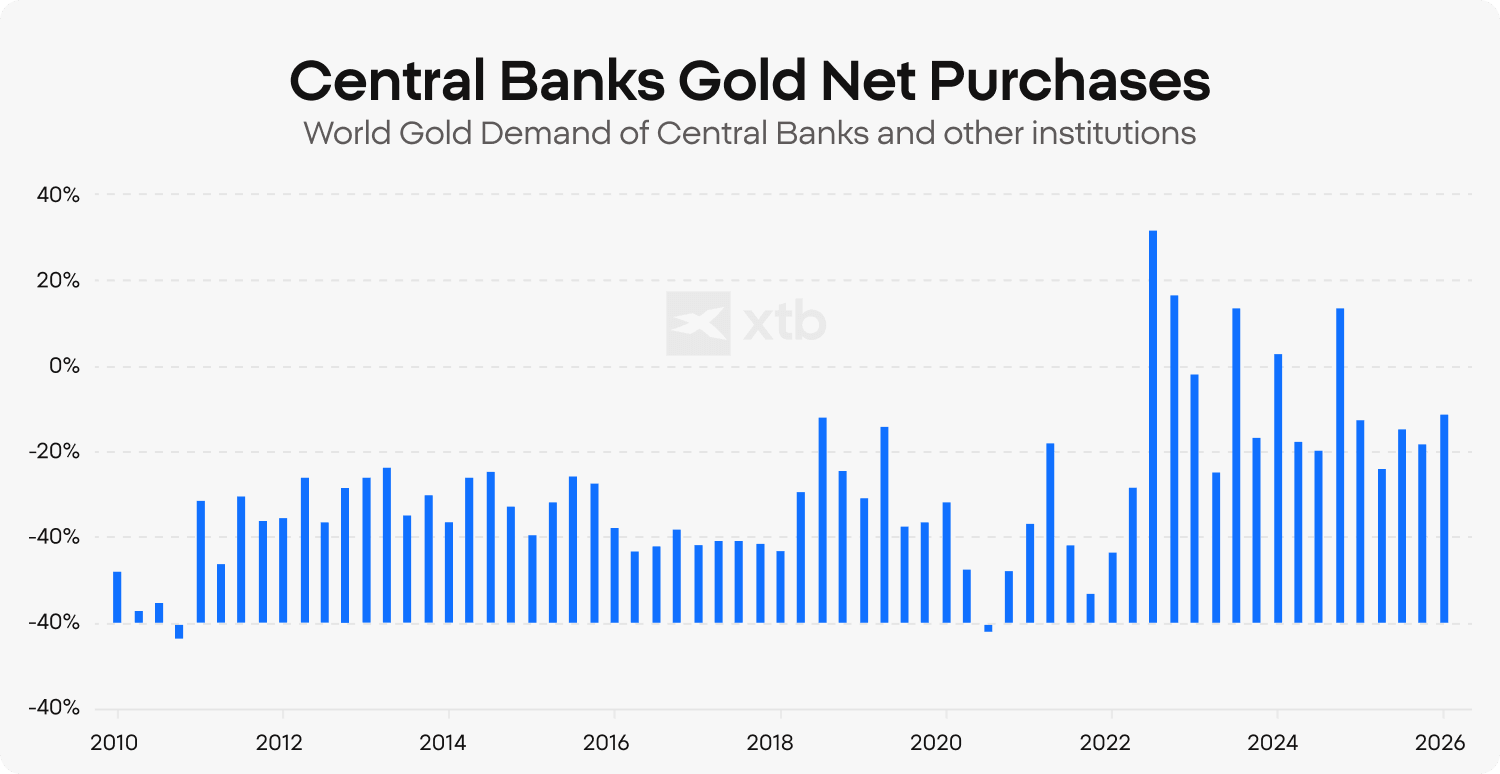

- Central bank demand has become one of the clearest examples of gold price drivers in recent years. According to the World Gold Council, central banks bought 1,136 tonnes of gold in 2022, 1,037 tonnes in 2023, 1,045 tonnes in 2024, and 863 tonnes in 2025.

- China’s reserve diversification strategy highlights part of what drives the price of gold globally. In recent years China reduced its holdings of US Treasuries below USD 800 billion while continuing to increase official gold reserves, reflecting broader efforts among central banks to diversify reserve assets after 2022.

1. Economic Uncertainty - Why Gold Rises When Markets Fear

Economic and geopolitical uncertainty is one of the main reasons why investors move capital toward gold. During periods of recession risk, banking instability, military conflict, or financial market stress, investors often reduce exposure to assets perceived as more volatile and increase exposure to assets considered more defensive. This mechanism helps explain what influences gold price during crises, even when inflation or interest rates are not the dominant market theme.

The relationship between uncertainty and gold is not accidental. Rising gold demand during periods of stress usually reflects a conscious attempt to protect capital and reduce exposure to currency weakness or declining confidence in financial markets. Because gold is globally traded, highly liquid, and not directly tied to the credit risk of a single government or company, it is often monitored as a so-called “safe haven” asset during unstable periods. Also, gold mining stocks usually follow gold bull and bear markets.

Investing in gold is not a guarantee that investor will profit from crisis. Gold does not always rise immediately during every economic downturn or crash. In some short-term market shocks, investors initially move into cash or highly liquid government bonds before reallocating part of their capital toward gold, which can temporarily increase price volatility. This is one reason why understanding what affects gold prices requires looking at broader market conditions rather than assuming that uncertainty automatically pushes gold higher in every situation.

📌 EXAMPLE

Economic uncertainty drives the demand for gold.

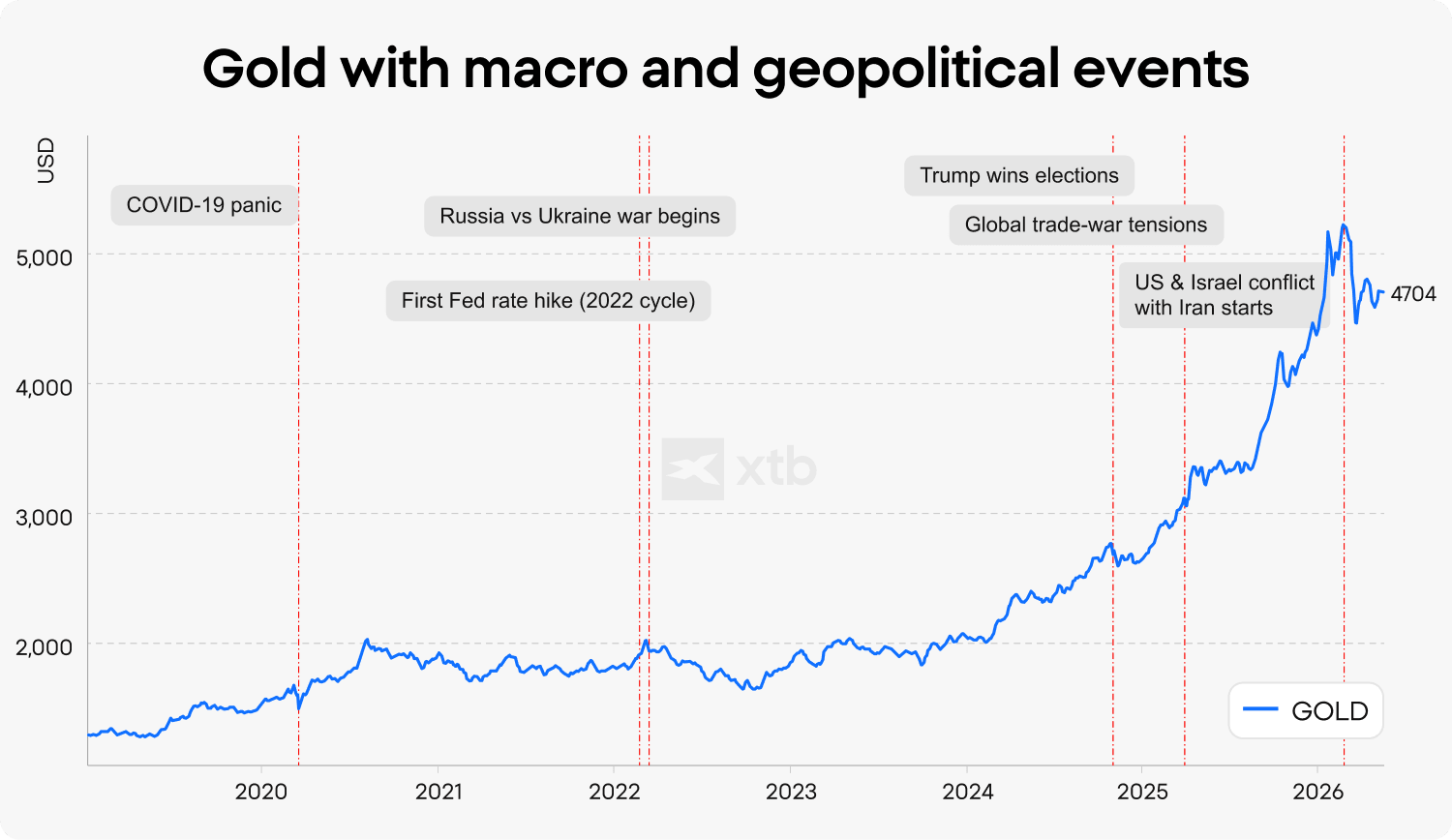

Gold prices surged during the COVID-19 crisis in 2020 as investors reacted to recession fears, aggressive monetary stimulus, and collapsing real yields. Gold also moved sharply higher during renewed US tariff tensions in 2025 amid concerns about global trade disruption and slowing economic growth, while during the 2008 financial crisis gold initially fell alongside other assets before later recovering strongly as central banks introduced large-scale stimulus.

COVID-19 (2020): prices reached new all-time highs in August 2020 as investors reacted to recession fears, massive monetary stimulus, near-zero interest rates, and falling real yields.

April 2025 tariff fears and Trump trade escalation: the gold rose strongly during renewed tariff tensions and uncertainty around global trade, inflation risks, and economic slowdown concerns. But it was not driven only by tariffs: central bank demand, ETF inflows, and interest-rate expectations also contributed.

2. Inflation - Why Gold Holds Value When Currencies Don't

Gold is often treated as a hedge against inflation because rising prices reduce the purchasing power of fiat currencies over time. When inflation accelerates, investors and institutions may look for assets perceived as more resistant to currency depreciation, especially during periods of aggressive monetary expansion or rapidly growing public debt. This is one of the most important mechanisms explaining what drives the price of gold over the long term.

The relationship between inflation and gold is closely connected to expectations about future monetary policy. Gold prices often react not only to current inflation levels, but also to whether central banks are expected to control inflation through higher interest rates or allow inflationary pressures to persist for longer. Because of this, high inflation alone does not automatically guarantee rising gold prices in every market environment.

The US dollar also plays an important role in global gold pricing. Since gold is traded internationally in US dollars, a weaker USD can make gold cheaper for buyers using other currencies, which may increase global demand and support prices. Conversely, a stronger dollar can reduce international purchasing power and become one of the factors affecting short-term gold price movements.

⚠️CAUTION

Interest rates are not the biggest gold price factor

After the 2008 Global Financial Crisis, the US Federal Reserve cut interest rates close to zero and launched large-scale monetary stimulus programs. At the same time, inflation expectations remained positive, which pushed real interest rates (interest rates adjusted for inflation) into negative territory for extended period, which supported the gold bull market.

A similar environment appeared again during the COVID-19 crisis in 2020, when central banks rapidly lowered rates and expanded liquidity programs to support the global economy. Gold prices climbed to new record highs above USD 2,000 per ounce in 2020 as falling real yields and economic uncertainty increased demand for defensive assets.

However, the relationship between gold and interest rates is not always straightforward. For example, gold reached fresh all-time highs again in 2025 and 2026 despite significantly higher interest rates rates from institutions such as the Federal Reserve and the European Central Bank. This clearly suggests that factors like geopolitical risk, central bank buying, fiscal concerns, and reserve diversification became more influential drivers of the gold market during this period.

3. Interest Rates - Why Falling Yields Make Gold More Attractive

Gold prices often move inversely to real interest rates, which are interest rates adjusted for inflation. When real yields fall, assets such as government bonds may generate weaker inflation-adjusted returns, reducing the opportunity cost of holding gold. This relationship is one of the clearest examples of factors behind gold prices in the global macroeconomic environment.

Unlike bonds or savings products, gold does not generate interest, coupons, or dividends. Its relative attractiveness tends to increase when inflation rises faster than nominal interest rates or when central banks begin lowering rates during periods of slowing economic growth. In these environments, investors may become less focused on income generation and more focused on preserving purchasing power.

The connection between interest rates and gold is also closely linked to expectations about future central bank policy. Markets often react not only to actual rate decisions, but also to signals about future monetary easing, recession risks, or slowing inflation-adjusted returns on debt instruments. This is why changes in expectations around Federal Reserve policy can influence gold prices even before interest rates officially change.

❓ DID YOU KNOW

EUR 100 from 1991 buys only about EUR 54 worth of goods in Germany today

Gold is often linked with long-term value preservation because it has been treated as a scarce and valuable asset for thousands of years. Fiat currencies work differently: their purchasing power can decline when prices rise, money supply expands, and public debt increases faster than the economy’s ability to absorb it.

For example in Germany, consumer prices rose from a CPI level of 65.5 in 1991 to 121.9 in 2025, meaning prices increased by about 86% over that period. In practical terms, goods that cost EUR 100 in 1991 would cost about EUR 186 in 2025, so EUR 100 in 2025 buys only around 54% of the same consumer basket.

Global liquidity means the amount of money and credit circulating in the financial system. When liquidity expands and public debt rises, currencies can face long-term devaluation pressure, while governments may also face higher costs to service bonds. This does not make gold risk-free, but it helps explain why falling purchasing power is one factor behind long-term gold demand.

4. Central Bank Reserves - Large-Scale Buying Moves Gold Prices

Central banks hold gold as part of their official reserves, and large-scale purchases can directly increase demand in the global market. Since 2022, central banks have bought more than 1,000 tonnes of gold annually according to World Gold Council data, making the official sector one of the strongest structural drivers of gold prices in recent years.

The trend accelerated after the freezing of Russian foreign reserves in 2022, which intensified discussions around reserve diversification and reduced dependence on the US dollar. Countries such as China, Poland, India, Turkey, Singapore, and Qatar became some of the most significant reported gold buyers between 2022 and 2025, while many emerging-market central banks increased gold holdings as part of broader de-dollarization strategies.

Central bank buying also matters because it can remain relatively stable even during periods of weaker investor sentiment. Unlike short-term speculative flows, reserve accumulation is often linked to long-term monetary strategy, geopolitical risk management, and diversification of foreign exchange reserves, which helps explain what influences gold price beyond daily market volatility.

5. Jewelry and Technology Demand - The Physical Use Still Shapes Gold Prices

Gold demand does not come only from financial markets, because jewelry consumption still represents a major part of global physical demand. According to the World Gold Council, jewelry accounted for around 40–50% of annual gold demand in recent years, with China and India remaining the two largest markets due to cultural traditions, wedding demand, and seasonal buying patterns. High gold prices can reduce jewelry consumption in the short term. For example, global jewelry demand fell in 2024 as record prices weakened affordability in several Asian markets.

Physical gold demand also tends to fluctuate seasonally. Demand often increases during India’s wedding season and major festivals such as Diwali, while Chinese New Year periods can also temporarily strengthen retail demand and local premiums. These patterns help explain what causes gold prices to move beyond macroeconomic and financial-market factors alone.

Technology demand represents a smaller but increasingly important source of gold consumption. Gold is widely used in electronics, semiconductors, medical devices, and high-performance connectors because of its conductivity and resistance to corrosion, while expanding AI infrastructure and data centre development may gradually increase industrial demand for advanced electronic components containing gold. Although technology demand remains significantly smaller than investment or jewelry demand, it still contributes to understanding what drives the price of gold over the long term.

6. Investment Demand and ETFs - How Markets Amplify Gold Prices

Gold ETFs allow investors to gain exposure to gold without storing physical metal. When capital flows into physically backed gold ETFs, fund providers usually need to hold more gold, which can support market demand; when capital flows out, this support can weaken. This makes ETF flows one clear example of what influences gold price in financial markets.

Gold ETF demand can change quickly because it reflects investor positioning rather than jewelry use or industrial consumption. High trading activity in ETFs and futures can therefore amplify short-term price volatility, especially when markets react to interest-rate expectations, the US dollar, inflation data, or geopolitical risk. Readers who want to compare gold with other assets as a store of value can continue to a separate guide here: [internal link placeholder].

Historical examples show that gold can be perceived as a safe-haven asset not only by institutions, but also by ordinary households during periods of panic. The analysis Investing in Gold in Times of Global Crisis (2022), by Rudiansyag Aggara cites the rush to buy gold during the Japanese invasion of China in World War II and Indonesia’s January 1998 crisis, when gold prices reportedly jumped before President Suharto’s state budget announcement. These episodes show how ETF flows, futures trading, and crisis-driven physical demand can all intensify spot price volatility when confidence in currencies or financial systems weakens.

As we can see on the chart, gold gained shortly after Russia - Ukraine war started in 2022 but significantly fell as Fed started to increase rates in 2022. However, gold is not always geopolitical conflict beneficiary over the short term - prices fell amid the US and Israel conflict with Iran, in 2026 as rising oil prices supported the US dollar and treasuries yields. We can see that the gold price surged shortly after the 2020 pandemic and world trade rensions in 2025, shortly after the Donald Trump won the elections. We can assume that uncertainty as a such and rising deficits support gold more than short-term events.

Remember, past performance is not a reliable indicator of future results.

FAQ

Gold prices are affected by a mix of economic, financial, and physical demand factors. The most important include economic uncertainty, inflation, real interest rates, central bank buying, jewelry demand, technology use, ETF flows, and the strength of the US dollar. No single factor explains every move, because several forces can act at the same time.

Gold often rises during uncertainty because some investors reduce exposure to riskier assets and look for assets perceived as more defensive. This does not mean gold always rises immediately during every crisis, but demand can increase when confidence in currencies, financial markets, or geopolitical stability weakens.

Inflation can support gold demand when investors worry that fiat currencies are losing purchasing power. Gold cannot be created by central bank policy in the same way as paper money, which is why it is often viewed as a long-term store of value. However, short-term gold prices can still fluctuate due to interest rates, speculation, and market sentiment.

Interest rates matter because gold does not pay interest or dividends. When real interest rates fall, the opportunity cost of holding gold becomes lower, which can make it relatively more attractive. When real yields rise, income-generating assets such as bonds may become more competitive.

Central banks buy gold as part of their official reserve strategy. Gold can help diversify reserves because it is not directly tied to one currency, government, or issuer. Since 2022, central bank buying has also been linked to broader discussions about reserve diversification and reduced dependence on the US dollar.

Yes, jewelry demand is an important part of physical gold consumption, especially in large markets such as India and China. Seasonal events, weddings, festivals, and local income trends can influence demand. At the same time, very high gold prices can reduce jewelry buying because the metal becomes less affordable for consumers.

When investors buy gold ETFs, funds must hold more physical gold, supporting prices. Outflows have the opposite effect, reducing demand and adding short-term price pressure.

Gold is often described as a safe-haven asset, but this term should be used carefully. It means gold may attract demand during stress periods, not that it is risk-free or guaranteed to rise. Gold prices can still be volatile, especially in the short term.

Gold is priced globally in US dollars, so changes in the dollar affect international affordability. A weaker dollar can make gold cheaper for buyers using other currencies, while a stronger dollar can make it more expensive. This is one reason why gold and the US dollar often move in opposite directions.

Gold prices cannot be predicted with certainty because they depend on many changing factors at once. Inflation, interest rates, central bank policy, geopolitical risk, ETF flows, and investor sentiment can all shift quickly. Forecasts can help explain possible scenarios, but they are not reliable indicators of future performance.

Cocoa could become a new luxury good - What’s driving the price surge?

Understanding Contango and Backwardation: Key Concepts in Commodity Futures Markets

The Outlook for Commodities in the Second Half of 2024

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.