If you’re investing or saving in the UK, understanding when the ISA allowance resets is essential. Timing your contributions correctly can mean the difference between maximising tax-free growth and losing valuable allowance forever.

If you’re investing or saving in the UK, understanding when the ISA allowance resets is essential. Timing your contributions correctly can mean the difference between maximising tax-free growth and losing valuable allowance forever.

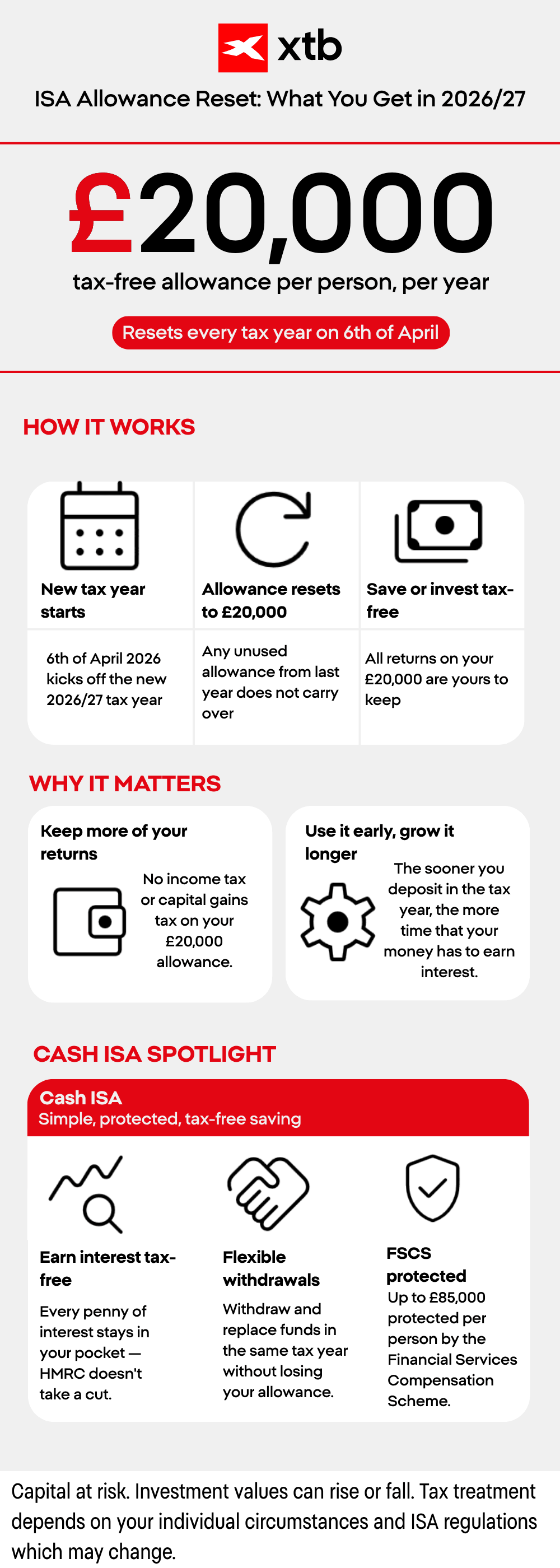

When Does the ISA Allowance Reset?

The ISA allowance resets every year on 6 April, which marks the start of the new UK tax year.

For the 2025/2026 tax year:

- Deadline to use your allowance: 5 April 2026 (midnight)

- New allowance becomes available: 6 April 202

This means that from 6 April 2026, you get a fresh £20,000 ISA allowance to use.

How the ISA Tax Year Works

The UK ISA system follows the tax year:

- Starts: 6 April

- Ends: 5 April (following year)

Each tax year gives you a fixed allowance (£20,000) that you can:

- Invest in a Stocks & Shares ISA

- Save in a Cash ISA

- Split across multiple ISA types

However, there’s one crucial rule:

Use it or lose it - unused allowance cannot be carried forward.

Why the ISA Reset Date Matters

Understanding the reset date isn’t just technical - it’s strategic.

1. Double Your Investment Window

If you act around the deadline, you can invest:

- Up to £20,000 before 5 April

- Another £20,000 after 6 April

That’s £40,000 invested within days, all tax-free.

2. Protect More of Your Money from Tax

ISAs shield your:

- Interest (Cash ISA)

- Dividends (Stocks & Shares ISA)

- Capital gains

Without an ISA, these may be taxable - especially as dividend and CGT allowances have been reduced in recent years.

3. Build Long-Term Wealth Faster

The earlier you use your allowance, the longer your money compounds tax-free.

Missing even one year could mean:

- Losing £20,000 of tax-efficient space forever

- Missing years of compounding growth

What Happens If You Miss the ISA Deadline?

Nothing dramatic happens immediately - but financially, it can be costly.

If you don’t use your allowance by 5 April:

- It expires permanently

- You start again with a new £20,000 on 6 April

- You cannot “top up” missed years later

Over time, this lost allowance can significantly reduce your tax-free wealth potential.

ISA Allowance for 2026/2027

For the new tax year starting 6 April 2026, the ISA limits remain:

- £20,000 total ISA allowance

Future change:

The Cash ISA allowance is expected to drop to £12,000 from April 2027 for under-65s

How XTB Fits Into Your ISA Strategy

XTB is a platform offering both:

All within a single account ecosystem.

Key Features of XTB ISAs

- £20,000 annual ISA allowance

- Allowance resets every 6 April

- Tax-free growth on investments

- Ability to invest in stocks and ETFs

- 0% commission up to 100k EUR

- *6% boosted rate to all new clients that open an ISA between 1 March and 30 April 2026. T&Cs apply.

Flexible ISA Benefits

One standout feature is flexibility:

- Withdraw money and redeposit within the same tax year

- No loss of allowance (on flexible ISAs)

This is particularly useful if you want:

- Emergency access to funds

- Short-term liquidity without sacrificing tax efficiency

This makes it appealing for both:

- Passive savers

- Active investors

Stocks & Shares ISA vs Cash ISA

Choosing between ISA types depends on your goals:

Cash ISA

Best for:

- Short-term savings

- Lower risk

- Predictable returns

Stocks & Shares ISA

Best for:

- Long-term growth

- Investing in equities, ETFs

- Beating inflation over time

XTB allows you to combine both approaches on one platform, which is useful for diversification.

Smart ISA Strategies Around the Reset Date

Here’s how to maximise your ISA each year:

1. Use Your Allowance Early

Don’t wait until April - investing earlier increases compounding time.

2. Use the “Double Dip” Strategy

Invest:

- Before 5 April

- Again after 6 April

This accelerates portfolio growth significantly.

3. Prioritise Tax Efficiency

Move:

- Dividend-paying stocks

- High-interest savings

…into an ISA first.

4. Choose the Right Platform

Look for:

- Low fees

- Flexibility

- Ease of use

XTB has been recognised as Best for Low-Cost ISA by BoringMoney.

Final Thoughts

The ISA allowance reset is one of the most important dates in the UK financial calendar.

Key takeaway:

- ISA deadline: 5 April 2026

- Reset date: 6 April 2026

- Annual allowance: £20,000

Used correctly, ISAs can:

- Shield your investments from tax

- Accelerate long-term wealth

- Provide flexibility and control

Platforms like XTB make it easier to combine saving and investing under one tax-efficient umbrella - but the real advantage comes down to using your allowance consistently, every year.

*XTB offers 6% AER (variable) to new clients who open an account between 1 March and 30 April 2026. The 6% AER includes a 2% boost for 90 days from the ISA open date. After the boost ends, the rate reverts to our standard variable rate of 4% AER. Your Cash ISA must be opened before 30th April to qualify. Existing clients receive our standard variable rate of 4% AER for current or new ISAs. Tax treatment depends on your individual circumstances and ISA regulations which may change.

What Is a Flexible Cash ISA - And Why Does It Matter?

Best Cash ISA Comparison 2026

Your New ISA Allowance Starts Now

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.