If you’ve been looking at Cash ISAs, you’ve probably seen the word ‘flexible’ come up especially when comparing different Cash ISA options.

Whether an ISA is flexible or not can make a real difference to how useful it is especially if you might need access to your money during the year. Here’s what it actually means and why it’s worth checking before you open an account.

If you’ve been looking at Cash ISAs, you’ve probably seen the word ‘flexible’ come up especially when comparing different Cash ISA options.

Whether an ISA is flexible or not can make a real difference to how useful it is especially if you might need access to your money during the year. Here’s what it actually means and why it’s worth checking before you open an account.

What is a flexible Cash ISA?

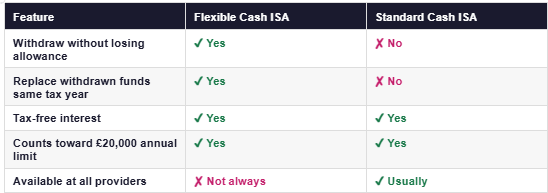

A flexible Cash ISA is a type of ISA that lets you withdraw money and replace it within the same tax year without it counting as a new contribution.

With a standard Cash ISA, every pound you put in counts toward your £20,000 annual allowance permanently. Withdraw £5,000 and then try to put it back, and you’ve used another £5,000 of your allowance. If you’ve already used your full £20,000, you simply can’t replace it.

With a flexible ISA, that rule doesn’t apply. Withdraw £5,000 and replace it before 5 April, and it’s as if the withdrawal never happened. Your allowance is restored.

Example: You deposit £20,000 into a flexible Cash ISA in April, using your full allowance. In August you need £3,000 for an unexpected cost, so you withdraw it. With a flexible ISA, you can put that £3,000 back later in the same tax year without any allowance penalty. With a standard ISA, you couldn’t.

Flexible vs standard Cash ISA: what’s the difference?

The key differences come down to what happens when you make a withdrawal:

In practice, both types shelter your money from tax in the same way. The difference is purely about what happens when you take money out and whether you can put it back.

Why does it matter?

For a lot of people, an ISA is a long-term savings vehicle they never touch. In that case, whether it’s flexible or not makes little practical difference.

But flexibility becomes important if:

- You might need access to funds during the year but still want to make the most of your allowance

- You’re using your ISA as part of your day-to-day cash management

- You want the option to move money in and out without worrying about permanently eating into your £20,000

- You’re not sure how much you’ll need to set aside over the course of the year

Essentially, a flexible ISA gives you a safety net. You can commit your full allowance without the worry that a withdrawal will cost you tax-free space you can’t get back.

A few things worth knowing

Flexibility only applies within the same tax year. If you withdraw money and don’t replace it before 5 April, the allowance is lost for that year. The clock resets on 6 April.

Not all providers offer it. Flexible ISAs are common but not universal. It’s always worth checking the product terms before opening an account.

It doesn’t change the annual limit. You still can’t contribute more than £20,000 in total across all your ISAs in a single tax year. Flexibility only affects your ability to replace withdrawals, not to exceed the cap.

It applies to the current tax year only. Previous years’ deposits can be withdrawn and replaced flexibly, but you can only replace up to the amount you’ve contributed in the current tax year.

Is a flexible Cash ISA worth it?

If you’re choosing between two providers with similar rates and terms, flexible wins every time. There’s no downside to having the flexibility, you simply don’t have to use it.

Where it really earns its keep is if you’re putting in a significant chunk of your £20,000 allowance but want to retain access. It removes the all-or-nothing dynamic that puts some people off committing their full allowance.

Some providers offer introductory rates for new Cash ISA clients. These can be higher for a limited period before reverting to a standard rate, so it’s worth checking the details before opening an account.

The 5th of April deadline is approaching. If you’re planning to use your £20,000 ISA allowance before the tax year closes, a flexible ISA means you can do so without locking your money away permanently.

Understanding ISAs: A Tax-Efficient Way to Save and Invest

Why You Should Maximise Your ISA Allowance Before April 5th with XTB

Why XTB Offers One of the Best Low-Cost ISAs in the UK

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.