Markets are wavering as we start trading on Tuesday. The focus remains firmly on the Middle East, as Donald Trump’s deadline for Iran to reopen the Strait of Hormuz approaches at 2000 ET tonight.

One deadline after another…

The Brent crude oil price had been as high as $111 a barrel, although it has since given back some gains. Overall, although the oil price is giving up earlier gains on Tuesday, there is still a sense of caution and pessimism about Trump’s deadline, as it seems unlikely that Iran will bend to meet Trump’s demands on the Strait of Hormuz before the deadline. The market is braced for a couple of outcomes: 1, the US continue with strikes on Iran, dashing hopes for a ceasefire, which could weigh heavily on risk sentiment and push up oil prices later or 2, Donald Trump does another ‘taco’ later today, including extending the deadline for Iran to reopen the Strait, which could ease upward pressure on oil and help risk sentiment to recover. The market is in limbo for now, and that means a lack of conviction for markets on Tuesday.

The conflict in the Middle East is one long deadline after another and there is a constant stream of promises to end the war coming out of the White House. Ultimately no one knows that the President will do next, and this is causing tensions to remain high in financial markets.

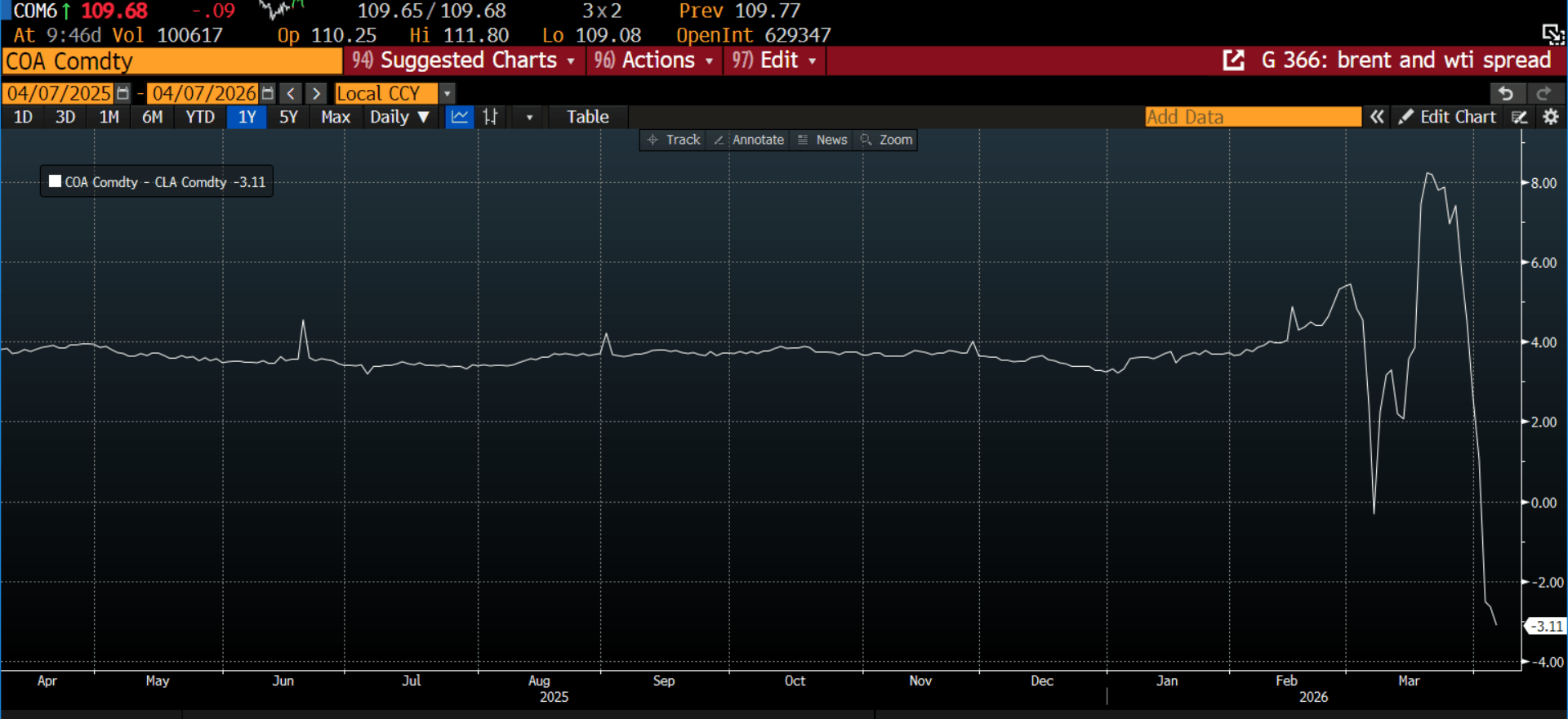

Why is WTI trading at a premium to Brent?

Interestingly, WTI is trading at a higher premium than Brent, it is currently at $114.70 vs. $111.60. This is unusual, as Brent usually trades at a higher price than WTI. The reason for this anomaly is due to the differences between how the two contracts work. The WTI contract delivers oil in May, while the Brent contract delivers oil for June. The oil market is currently in backwardation, whereby current spot prices for oil are higher than futures prices, which indicates immediate supply shortages and is a sign that traders hope that oil prices will be lower in the future. This is also a sign that traders remain hopeful that the conflict will be over with the next two months. Ultimately, it is hard to see the oil market shift out of backwardation until there is a breakthrough in negotiations between Iran and the US, or until the Strait of Hormuz is back open. If the Strait does open soon, then the price of WTI is likely to fall sharply and Brent’s positive premium could return.

Chart 1: Brent and WTI spread.

Source: XTB and Bloomberg

Earnings season meets geopolitical chaos

European equities are posting mild gains as we move through the morning, and the FTSE 100 is bolstered by the oil majors, which are some of the top performing UK stocks today. Looking ahead, the start of earnings season is worth watching this week. Delta Airlines will report Q1 results on Wednesday, which is the traditional start of US earnings season. Thus, geopolitics will meet corporate news in the coming days and weeks, we will be watching to see which ones wins out.

Investors welcome Unilever’s M&A plans

Aside from events in the Middle East, there are some other stories driving markets on Tuesday. Unilever is a top performer in the UK today and is higher by more than 1% after it said that it wants to concentrate on more health and wellness deals after disposing of its food unit to McCormick Foods. The health and wellness sector of Unilever is seen as a growth engine for the firm, and the market is welcoming Unilever’s signal that it intends to engage in future deals.

Bargain hunters go shopping

Other news includes Pershing Capital’s offer to buy Universal Music, which is listed in Amsterdam. Pershing already owns 5% of the company, and its offer is well timed, the Universal stock price has slumped 30% this year, mainly due to AI concerns. This deal is a sign that amidst the conflict in the Middle East, there is dealmaking going on. Companies that have been impacted by the AI sell off could become takeover targets. Some of the weakest sectors on the S&P 500 this year include data processing companies, consumer finance and systems software, which are legitimate takeover targets after falling more than 20% so far this year.

France Challenges Palantir, Market Reacts.

The semiconductors sell-off continues 📉

US OPEN: Deeper sell-off and a SaaS rebound

Mercedes earninigs: Is optimism justified?

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.