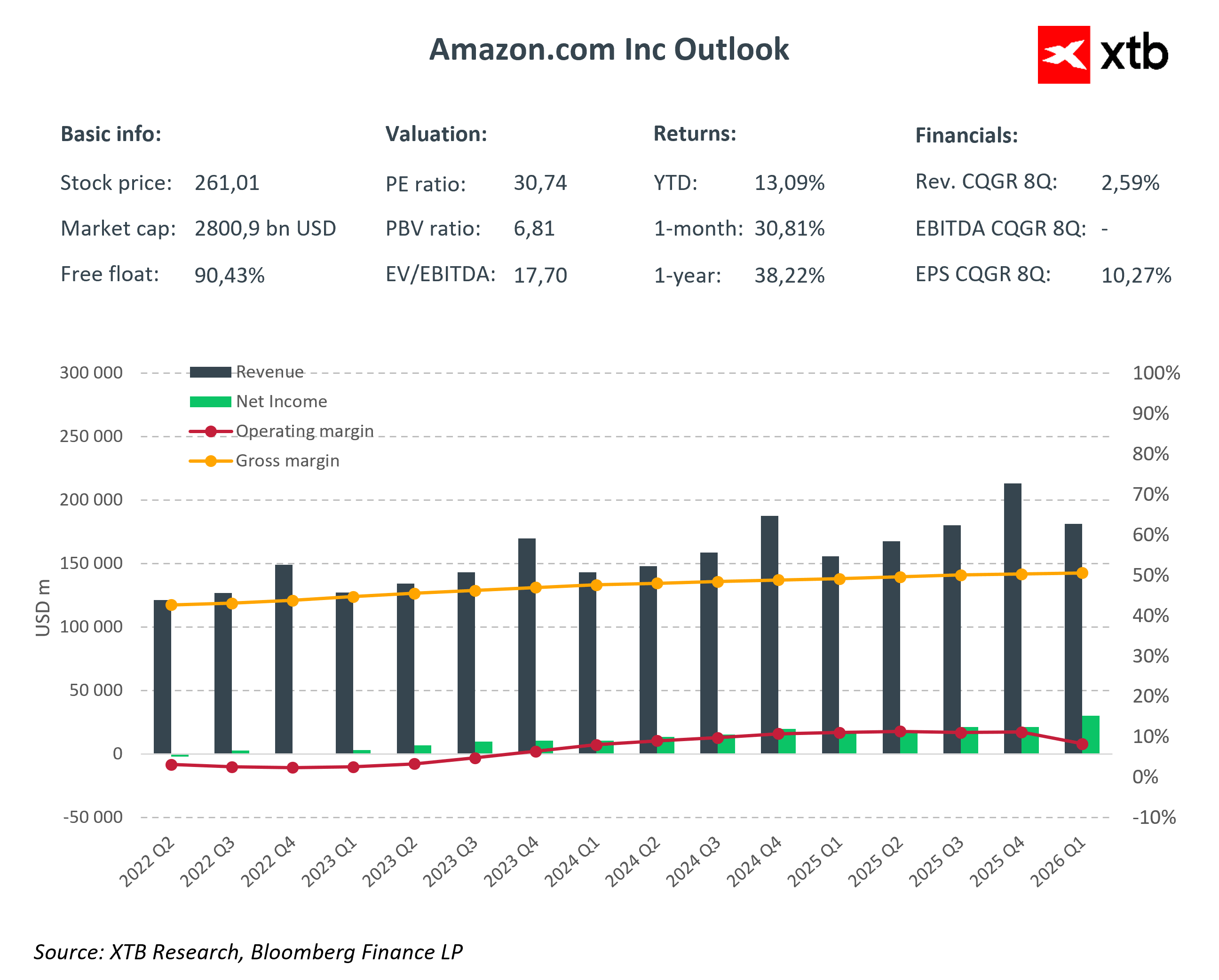

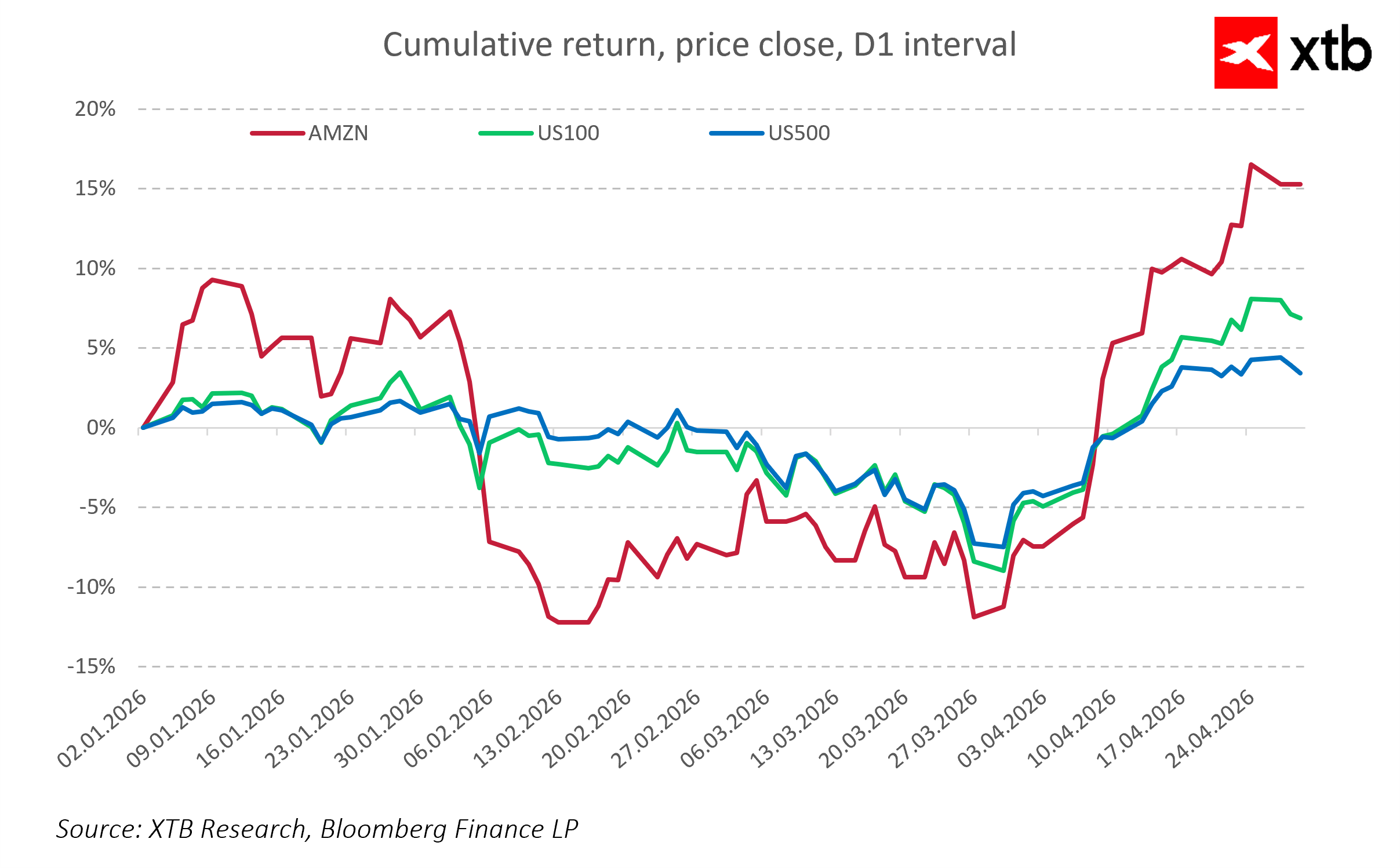

Amazon reported its first-quarter 2026 results, showing that the company continues to maintain a very strong operational position. However, the market reaction remains clearly negative. The stock is declining in after-hours trading, suggesting that investors are not questioning the quality of the business itself, but are instead disappointed by the lack of a more pronounced acceleration in key growth segments.

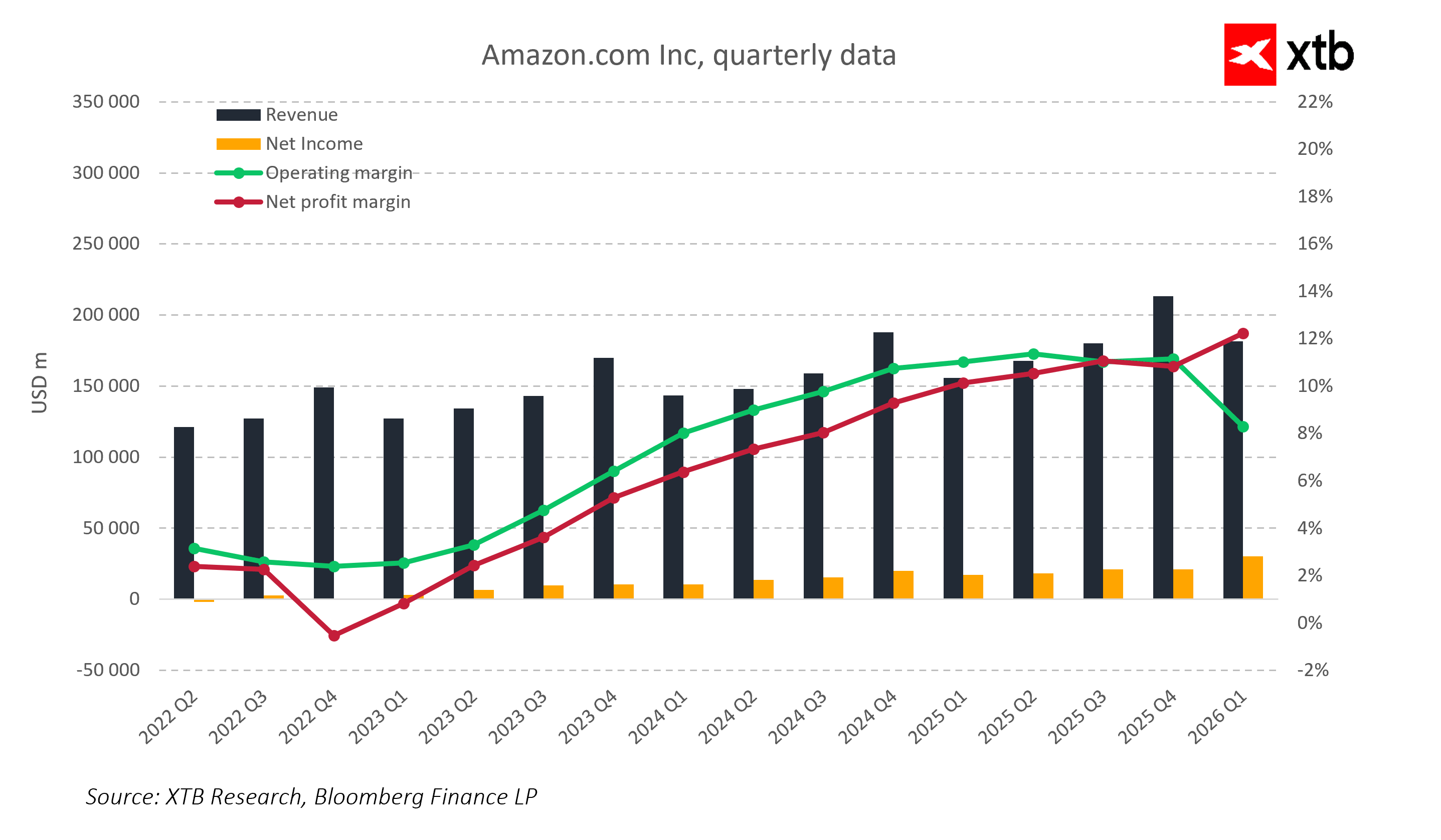

Revenue came in at $181.5 billion versus expectations of $177.2 billion, representing a solid beat versus consensus and confirming continued scale expansion. Operating income reached $23.85 billion, also significantly above forecasts, while operating margin increased to 13.1%, reflecting ongoing improvements in overall business efficiency. Earnings per share came in at $2.78 versus expectations of $1.62; however, this figure was materially boosted by a one-off gain related to the revaluation of Amazon’s investment in Anthropic, which distorts the picture of underlying operating profitability.

Key Q1 2026 financial highlights

-

Revenue: $181.5 billion vs. $177.23 billion expected, a clear beat and continued stable scale growth

-

Operating income: $23.85 billion vs. $20.75 billion expected, indicating stronger-than-expected operational efficiency and higher profitability

-

Operating margin: 13.1% vs. 11.7% expected, confirming improved cost structure and a higher contribution from more profitable segments

-

EPS: $2.78 vs. $1.62 expected, but significantly inflated by a one-off gain, limiting its interpretation as a purely operational result

-

AWS: $37.59 billion vs. $36.68 billion expected, +28% YoY vs. 25.7% expected, confirming continued strong momentum in the cloud segment

-

Capital expenditures: $44 billion out of a planned ~$200 billion for full-year 2026

Business segments

Amazon Web Services remains the key growth pillar and the central focus of the artificial intelligence narrative. The segment generated $37.6 billion in revenue, representing 28% year-over-year growth and beating expectations. This is also the strongest growth rate in several quarters, confirming sustained demand for cloud infrastructure and AI-related services. However, while growth remains strong, it did not show a meaningful acceleration versus investor expectations, which limited the market’s positive reaction.

The e-commerce segment remains a stable foundation of Amazon’s business. Online store revenue reached $64.25 billion, also above forecasts, highlighting the resilience of the core retail business despite increasing competition. Growth was also visible in third-party seller services and advertising, which reached $17.24 billion in revenue and continues to post double-digit growth, gradually increasing its contribution to overall profitability.

Capital expenditures and outlook

A key element of the report is the scale of capital investment, reflecting the ongoing global race in artificial intelligence and computing infrastructure. Amazon is currently executing one of the most aggressive investment programs in the technology sector, with total capital expenditures expected to reach around $200 billion in 2026. In the first quarter alone, capex exceeded $44 billion, highlighting the rapid expansion of data centers and AWS infrastructure.

The increasing scale of capital spending means that the market is shifting its focus away from current earnings performance and toward the question of how quickly these investments will translate into sustained acceleration in cloud growth and meaningful AI monetization.

Outlook and conclusions

Amazon remains one of the most diversified and operationally efficient technology companies in the world. Stable e-commerce growth, the expanding role of advertising, and the strong position of AWS provide a solid foundation for further expansion. However, the current market reaction shows that strong results alone are no longer sufficient in an environment of extremely high expectations around AI and cloud computing.

The company delivered very strong financial results but failed to generate a clear acceleration in the growth narrative that investors were looking for.

The market reaction also reflects a broader shift in how Amazon is being valued. Increasingly, it is not enough to beat expectations; what matters is whether the company delivers a visible acceleration in its most forward-looking segments. Investors are now primarily focused on AWS growth dynamics and the pace of AI monetization, treating these as key drivers for future revaluation.

At the same time, the scale of capital expenditures has become an additional source of uncertainty. While strategically justified, rising capex is raising questions about how quickly these investments will translate into higher free cash flow and improved profitability in the medium term.

As a result, Amazon remains in a transitional phase, where the key variable will be the speed of AWS transformation in the context of artificial intelligence, and the ability to convert record capital investments into sustained acceleration in revenue and earnings growth.

US Open: S&P 500 Tries to Halt the Decline 🗽 GE Vernova Falls 5%

Wall Street Fears the Peak of the AI Bull Market. Have Semiconductors Already Seen Their Best Days?

Alphabet and Tesla Ahead of Earnings: Will the Tech Giants Shake Wall Street?

Defense sector ahead of earnings: Summary

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.