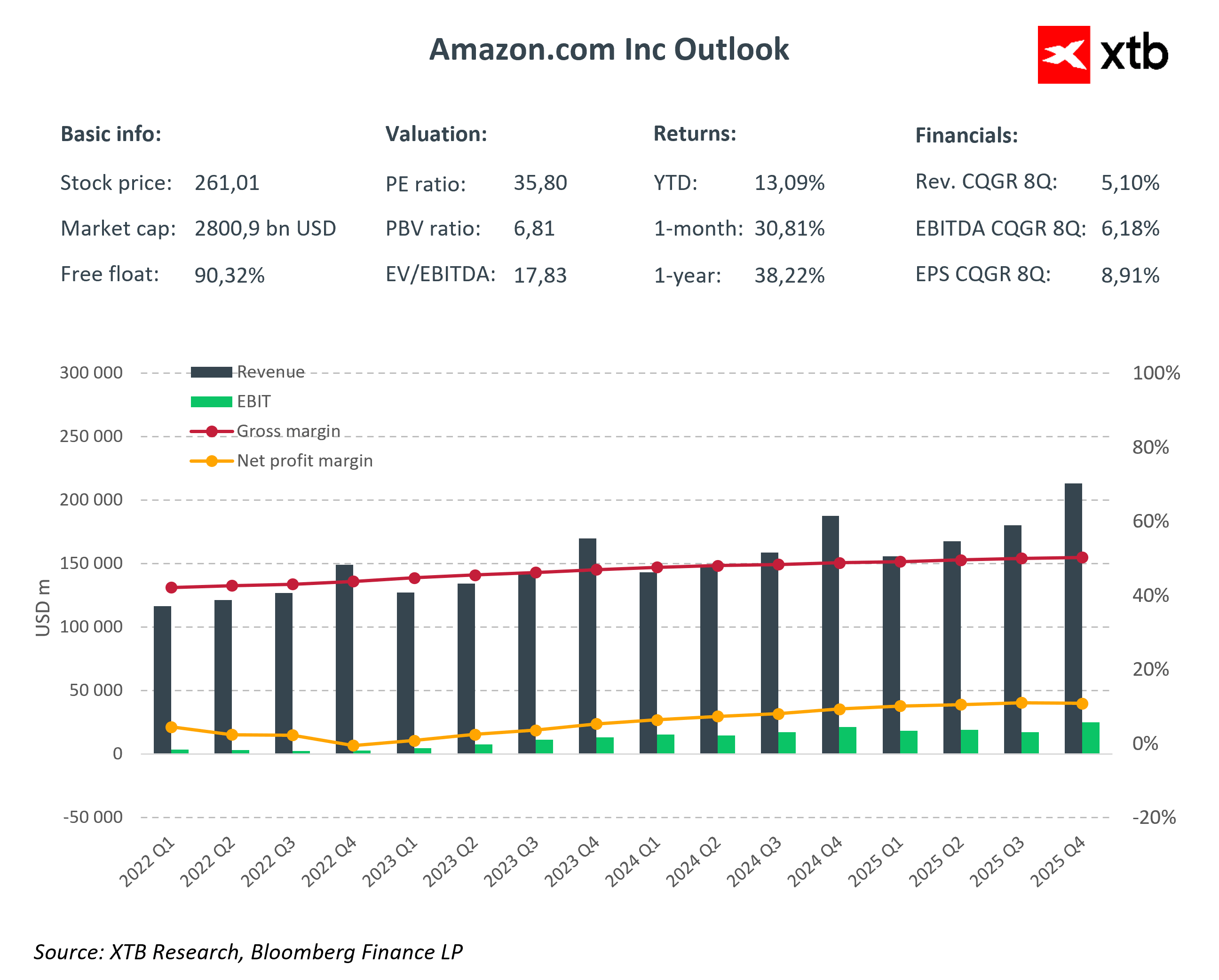

Amazon enters its Q1 2026 earnings release at a point where the market is increasingly less focused on the company as an e-commerce platform and more on its role as a core layer of the global artificial intelligence infrastructure. This shift in narrative is crucial, as it moves the focus away from growth speed toward the quality and durability of that growth.

Behind the story sits a record investment cycle, with CapEx approaching 200 billion USD annually. In this environment, Amazon is being priced simultaneously as a future AI winner and as a company under pressure to prove that this scale of investment is already translating into real returns. As a result, this earnings report will not be interpreted as a set of standalone numbers, but rather as a test of whether massive capital deployment is starting to improve the quality of the overall business model.

Market expectations for Q1 2026

Consensus expectations point to a relatively stable quarter, where the key question is not the level of growth itself, but its composition and quality.

-

Revenue: 177–188 billion USD (13–14% year over year growth)

-

EPS: 1.61–1.65 USD

-

AWS: growth around 25% or higher, supported by strong demand for AI-related workloads

-

CapEx: sustained at a very high level, driven by continued investment in AI infrastructure and data centers

What is increasingly important is that the market no longer interprets these figures in a linear way. Each segment now plays a different role in the overall narrative, with AWS acting as the re-rating engine, advertising as a high-margin stabilizer, and retail as the cash flow backbone of the entire model.

AWS and AI: from cloud to AI infrastructure layer

Amazon Web Services is becoming the central pillar of the entire investment story. It is no longer just a cloud business, but increasingly an infrastructure layer for the development and commercialization of artificial intelligence.

The market will focus on whether AWS can sustain growth in the mid-20% range or higher, but an equally important question is the quality of that growth. At the center of attention is the relationship between accelerating AI demand and profitability, which may come under pressure from rising compute costs.

Another key element is the development of in-house silicon, such as Trainium and Graviton. These are no longer just part of a technology strategy, but an attempt to take greater control over the economics of the AWS ecosystem and reduce dependence on external GPU suppliers.

At the same time, the monetization of artificial intelligence remains a key reference point. The previously indicated level of around 15 billion USD in annual revenue from AI-related services is increasingly treated as a benchmark for assessing whether Amazon is entering an acceleration phase or still remains in the early stages of adoption.

Retail and advertising: stability in the shadow of transformation

The retail segment remains less exciting from a narrative perspective, but it continues to play a critical role in the overall business model. It is the primary source of stable cash flows that finance Amazon’s intensive investment cycle in artificial intelligence and infrastructure.

The market will pay close attention to North American margin stability, expected to remain in the low single-digit range. The key question is whether ongoing automation and technological transformation translate into real operational efficiency gains, or whether they are offset by rising structural costs.

Advertising remains one of the most profitable segments in the entire ecosystem, but its role in the current cycle is more about stability than narrative re-rating. It continues to generate high-quality cash flow that supports the most capital-intensive phase of Amazon’s development.

CapEx: the price of the future

The scale of capital investment remains one of the main points of tension between the company and the market. Amazon is in a phase where CapEx is both the foundation of future competitive advantage and a source of short-term pressure on financial performance.

On one hand, the dominant narrative is the construction of a long-term infrastructure advantage in AI, where current spending is strategic in nature and intended to secure leadership for years to come. In this scenario, investment scale acts as a barrier to entry and a foundation for future AWS dominance.

On the other hand, the market is increasingly focused on the pace of return from these investments. High CapEx in a structural technology transition implies pressure on free cash flow and greater sensitivity to any delays in AI monetization.

As a result, the report will be judged less on the size of investment itself and more on whether it is already improving the economics of AWS and the broader business model.

Limited room for error

Amazon is currently priced with a clear premium for its exposure to artificial intelligence, which means that the margin for disappointment is limited. The market is not only expecting growth, but growth of the right quality.

The main areas of sensitivity include AWS momentum, cloud operating margins, the pace of AI revenue conversion, and the trajectory of free cash flow in a high CapEx environment.

In this context, even a solid report may be received neutrally if it does not confirm that Amazon is transitioning from a phase of heavy investment into a phase of higher-quality, more efficient growth.

Key takeaways

-

Amazon is in a phase where the market is no longer evaluating growth speed, but its quality under an intensive investment cycle

-

AWS and AI are becoming the main re-rating engine of the company rather than just incremental growth drivers

-

Retail and advertising provide stability to the model but no longer define its valuation

-

CapEx remains the key balancing factor between expansion and profitability

-

The market is testing whether AI within Amazon is moving from an investment phase to real monetization

US Open: S&P 500 Tries to Halt the Decline 🗽 GE Vernova Falls 5%

Wall Street Fears the Peak of the AI Bull Market. Have Semiconductors Already Seen Their Best Days?

Alphabet and Tesla Ahead of Earnings: Will the Tech Giants Shake Wall Street?

Defense sector ahead of earnings: Summary

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.