The oil price surged above $100 per barrel at one stage on Thursday morning, although it is backing away from this level as we move through the morning. Reports that more ships were the targets of Iranian drones outside of the Strait of Hormuz, is okeeping upward pressure on commodities. Two ships were struck off the coast of Iraq, and Oman’s oil terminal, Mina Al Fahal, has also been closed as a precaution. This shows how the conflict is now spreading and threatening the few ports that have remained open throughout this crisis.

Elevated oil prices for the long haul

Brent crude surged to a high of $101.59 per barrel earlier on Thursday, although it is currently trading below $98, still a 6% jump this morning. The conflict has intensified this week, and the longer the oil price remains elevated, the more damaging and long-lasting the inflation shock will be for the global economy. We mentioned earlier this week that when oil prices hit $100 per barrel, they tend to be sticky around this level. Back in 2022, WTI crude stayed above $100 for 87 days, thus the market needs to be prepared for elevated oil prices for the long haul.

Commodity price volatility is here to stay

Today’s price jump comes after Wednesday’s announcement that the IEA will release 400mn barrels of oil from global reserves. This is failing to control the oil price rise and is highlights how limited global policy makers are in this crisis. Overall, pictures of oil tankers on fire across the Gulf region, a large release of global oil reserves including 40% of US reserves, and no clear strategy from President Trump of the aims of this war are not indicators of stable oil prices, even if Bent crude is backing away from $100 per barrel this morning. Commodity price volatility is here to stay, and this is bad news for Asia and Europe, in particular.

Mild stock market sell off expected for Europe

Asian stocks were down approx. 1% on the back of this news, and European stock index futures are pointing to relatively mild losses so far on Thursday, with a 0.7% decline expected for the Eurostoxx 50 index, and a 0.1% sell off expected for the FTSE 100, as the UK index is bolstered by elevated oil prices.

The equity market reaction has been fairly mild, and in contrast to the deeper sell off in bonds. There was some expectation that equities might align with bonds and face a deeper sell off, but this has not materialized so far this week. While stocks are still in the red, the events in the Middle East have not caused a rout in global markets yet, even though the Eurostoxx 50 index has had 6 losing days so far this month.

A flurry of negative headlines is adding up for stocks, and it is worth watching them closely. There is a clear underperformance for Asian and European equity indices, while US stocks are the winners so far from the conflict. The Nasdaq is posting a small gain for this month, as the main US tech index walks to the beat of its own drum.

Private credit fears around software rise, as software stocks recover

Private credit fears are also building. The Illiquid part of the private credit market has been roiled by news that several high-profile funds are now closed to redemptions, and credit fund prices have tumbled. Fears about private credit’s exposure to software firms is high, however, there is a risk that fears are misplaced, and the fact that stocks have not fallen heavily on the back of the drip feed of news and media hysteria about private credit is worth noting. These funds are not designed to trade like equities or regular bonds.

It is also worth noting that fears around the private credit space are linked to angst around loans to the software space. However, at the same time, the software sector in the S&P 500 is in recovery mode and is the 4th best performing sector in the main US index so far this month, it is higher by nearly 5%. The recovery in software stocks after a deep sell off earlier this year may ease fears in the private credit space if it continues.

Rate hike priced back in for the UK

Ahead today, we expect another rough day for global bonds, as oil prices remain elevated and bonds remain more sensitive than equities to inflation fears. Interest rate volatility is back, and the futures market is now predicting rate hikes for the UK once more.

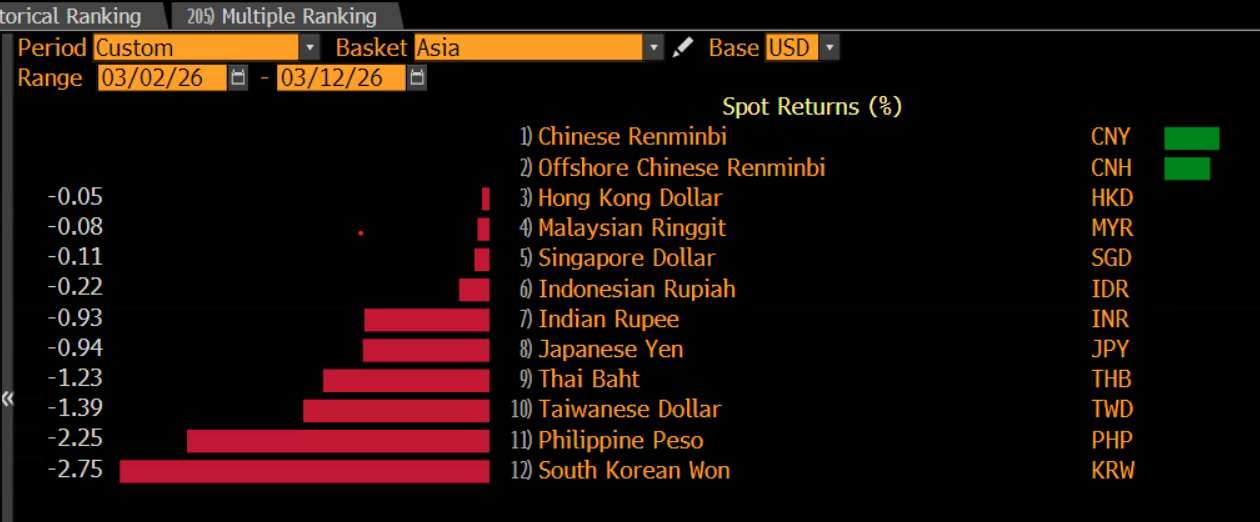

In the FX space, the dollar is higher again today, although it has backed away from earlier highs around $99.50 and is following the oil price down. The dollar is particularly strong vs. Emerging market currencies, and Asian FX right now, as inflationary fears weigh heavily on Asian FX , as you can see below.

Chart 1: USD vs Asian FX month to date

Source: XTB and Bloomberg

Samsung Enters the Era of “Physical AI” and Robotics; Shares Rise 3% 🤖

Healy makes first move as Chancellor, but bond market not impressed

Economic calendar: Strong reading from the UK labour market, German ZEW in focus

Chart of the day 🔼Nasdaq gains 1.2% as semiconductors rebound (21.07.2026)

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.