- Apollo argues that the market may be overly optimistic about the pace of AI monetization, with consensus expecting hyperscalers' free cash flow to more than double over the next several years.

- Declining token prices and intensifying competition from Chinese AI models could make current earnings forecasts harder to achieve, putting additional pressure on the profit margins of the largest technology companies.

- If returns on AI investments take longer to materialize than expected, the impact could extend well beyond the technology sector, triggering a re-rating of the Magnificent 7, weighing on the broader S&P 500, and potentially slowing the global economy.

- Amazon remains the largest debt issuer among the leading hyperscalers, having raised more than $100 billion to help finance the expansion of its AI infrastructure.

- Apollo argues that the market may be overly optimistic about the pace of AI monetization, with consensus expecting hyperscalers' free cash flow to more than double over the next several years.

- Declining token prices and intensifying competition from Chinese AI models could make current earnings forecasts harder to achieve, putting additional pressure on the profit margins of the largest technology companies.

- If returns on AI investments take longer to materialize than expected, the impact could extend well beyond the technology sector, triggering a re-rating of the Magnificent 7, weighing on the broader S&P 500, and potentially slowing the global economy.

- Amazon remains the largest debt issuer among the leading hyperscalers, having raised more than $100 billion to help finance the expansion of its AI infrastructure.

The world's largest technology companies are expected to invest roughly $3 trillion in artificial intelligence infrastructure over the coming years, raising a critical question: will these enormous AI investments generate returns quickly enough?

- This marks a subtle but highly important shift in the market narrative. Investors are no longer debating whether AI is a transformative technology—that point is largely settled. Instead, the discussion has rightly shifted toward the economics of the AI boom.

- Analysts at Apollo Global Management argue that current market expectations may be built on an overly optimistic timeline. The commercialization of AI could take significantly longer than investors currently anticipate. If that proves true, the consequences would extend far beyond technology stocks and could ultimately affect the broader equity market.

- Adding to the uncertainty is the emergence of China as a serious competitor to Western AI models. According to Apollo, Chinese models have been gaining popularity in recent months, steadily increasing their share of the global AI market and narrowing the competitive gap with their U.S. counterparts.

History suggests that revolutionary technologies often need more time

This is far from the first time investors have become captivated by a transformative technology. During the nineteenth century, capital flooded into railroad construction. Railways ultimately became one of the most important innovations in economic history, yet many investors failed to earn the returns they expected. Too many rail lines were built, competition expanded faster than demand, and capital took much longer to generate attractive returns than originally projected.

Railroad stocks eventually collapsed after years of spectacular gains, even though the tracks themselves were built and fundamentally transformed global commerce. It would therefore be naive to assume that the expansion of AI infrastructure must automatically translate into a sustained bull market for technology stocks.

A remarkably similar pattern emerged during the fiber-optic boom of the late 1990s. The internet undoubtedly changed the world, but much of the infrastructure remained underutilized for years, while numerous telecommunications companies failed following the dot-com crash.

The paradox of major technological revolutions is that the technology often succeeds long before many of its early investors do. Apollo argues that today's AI market may be facing precisely this type of risk.

The market assumes cash flows will accelerate rapidly

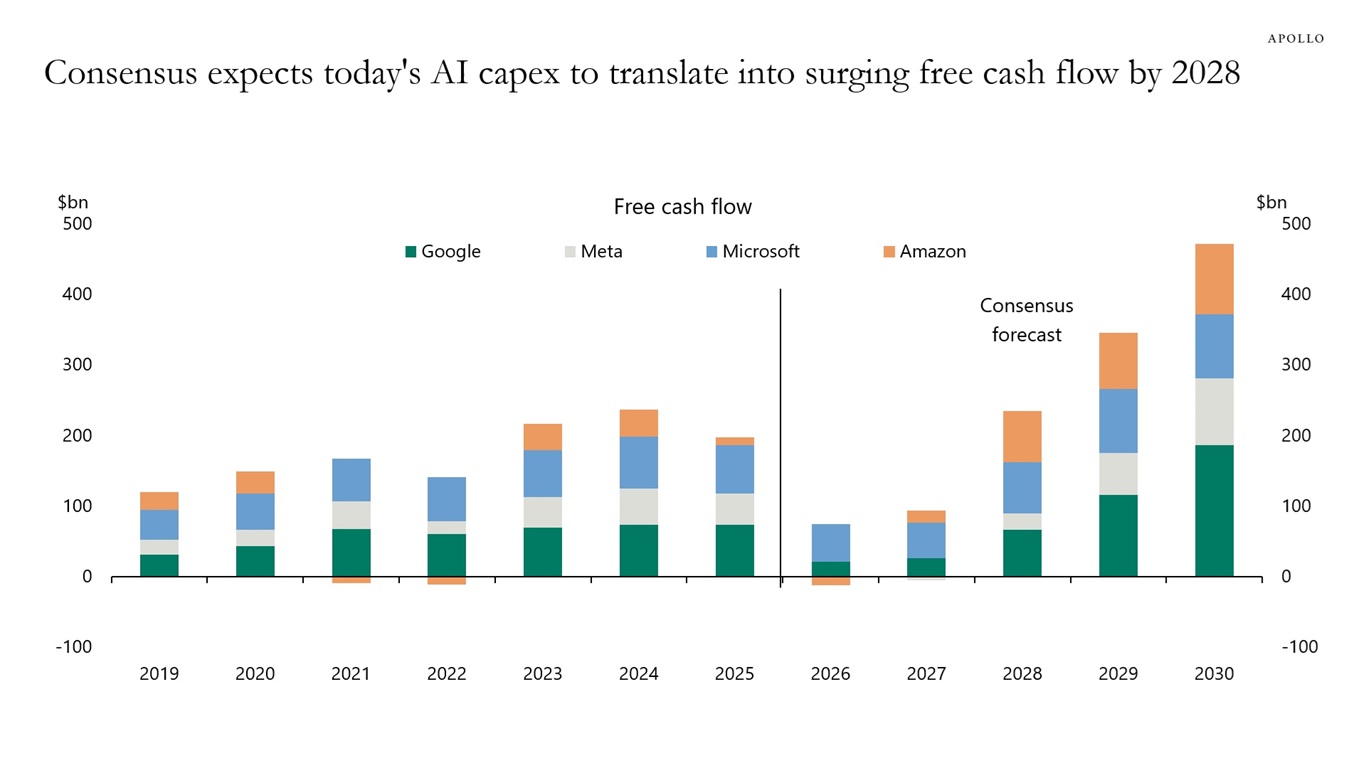

Wall Street consensus expects the free cash flow generated by hyperscalers—including Microsoft, Amazon, Alphabet and Meta—to more than double over the next several years. This assumption underpins much of today's valuations.

Technology giants are committing hundreds of billions of dollars to data centers, GPUs and power infrastructure because investors expect AI services to begin generating extraordinary cash flows in the near future. But what if meaningful returns arrive in five or seven years rather than two?

That would not necessarily mean these investments were misguided. It would simply imply that investors underestimated the time required for them to produce attractive economic returns—and that timing difference could prove extremely costly.

Current forecasts assume that free cash flow at the largest hyperscalers will begin accelerating as early as 2027 before inflecting sharply higher in 2028. Achieving those projections would require cash generation to expand well beyond already record-breaking capital expenditures. In other words, profits would have to accelerate at an unprecedented pace.

The obvious question is: what if they don't?

Or what if entirely new costs emerge along the way—costs that are difficult to quantify today, such as expensive connections to the U.S. electricity grid or significantly higher operating expenses required to support increasingly power-hungry AI infrastructure?

Source: Apollo Global

Two developments are beginning to raise concerns

Apollo highlights two trends that could make today's forecasts more difficult to achieve.

The first is the rapid decline in token prices.

Every new generation of AI models becomes more efficient, competition intensifies, and the cost of processing the same amount of information continues to fall. This benefits customers, but it also places increasing pressure on pricing and profit margins for AI providers.

Like most technologies, AI services are likely to become cheaper over time.

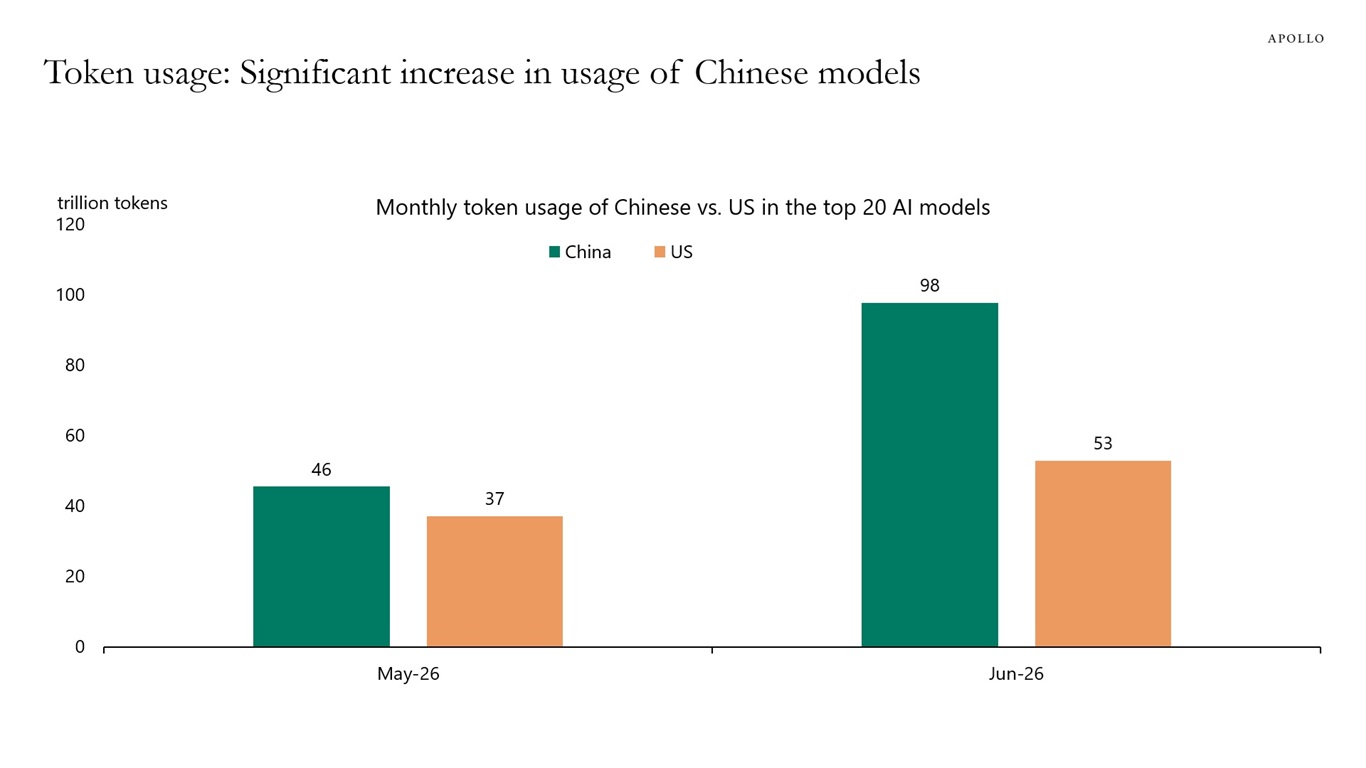

The second concern is China's growing competitive position.

Until recently, many investors assumed that U.S. models would maintain a comfortable technological lead. Apollo's data, however, suggest that Chinese models are steadily increasing both their global market share and their share of total token usage.

If customers increasingly prioritize price-to-performance rather than simply choosing the most advanced model, today's market leaders may enjoy a smaller competitive advantage than investors currently expect.

The challenge is that the bills arrive immediately

The biggest issue is not capital expenditure itself. The problem is timing. Data centers must be built today. GPUs must be purchased today. Electricity contracts must be secured today. Financing must also be arranged immediately.

The revenues, however, may arrive much later.

This creates a potentially dangerous mismatch in which costs rise exactly as planned while profits fail to keep pace.

If AI monetization continues to be pushed further into the future, operating margins at the largest technology companies could come under pressure precisely when investors expect them to expand dramatically.

Why a problem for a handful of companies could become a market-wide issue

Ten years ago, a similar scenario would have been far less consequential. Today, however, the largest technology companies account for an enormous share of both the S&P 500's market capitalization and overall earnings growth.

As a result, any meaningful re-rating would almost certainly extend beyond Microsoft, Amazon or Nvidia.

Lower-than-expected demand for AI infrastructure would likely affect semiconductor manufacturers, data center operators, utilities, cooling equipment suppliers, networking companies and virtually the entire ecosystem built around artificial intelligence.

AI is no longer simply another technology sector. It has become one of the primary engines driving today's investment cycle.

Is this another dot-com bubble?

Not necessarily.

There is one major difference between today's AI boom and the internet bubble of the late 1990s.

The largest technology companies are financing their investments using businesses that already generate tens of billions of dollars in annual cash flow. Microsoft, Alphabet and Meta are not speculative companies hoping to become profitable—they are among the most profitable corporations in history.

That significantly reduces the probability of a complete collapse similar to the dot-com era.

Nevertheless, history teaches another valuable lesson: a revolutionary technology does not automatically become a great investment at every stage of its development. More often than not, investors overestimate how quickly new technologies begin producing meaningful returns on invested capital.

The key question is no longer whether AI will change the world

The market has largely answered that question already. A far more interesting question today is whether current valuations assume that AI commercialization will happen too quickly. That is precisely where Apollo believes investors should focus.

If AI pricing continues to decline, competition intensifies and returns on hundreds of billions of dollars of investment are pushed several years into the future, markets may be forced to reassess today's optimistic expectations.

This would not signal the end of the AI revolution. The histories of railroads, electricity and the internet suggest something quite different: transformational technologies often reshape the world much faster than they generate attractive returns for their earliest investors. For equity markets, the distinction between those two processes could prove far more important than many participants currently appreciate.

Perhaps the most underappreciated risk is China's growing presence in AI. U.S. companies may increasingly find themselves competing for market share against Chinese models that continue improving while remaining significantly cheaper. If those lower-cost models experience stronger-than-expected adoption, they could create a competitive headwind that investors have only recently begun to recognize. According to Apollo, Chinese models already account for a larger share of total token usage than their U.S. counterparts.

Source: Apollo Global Report (July 2026)

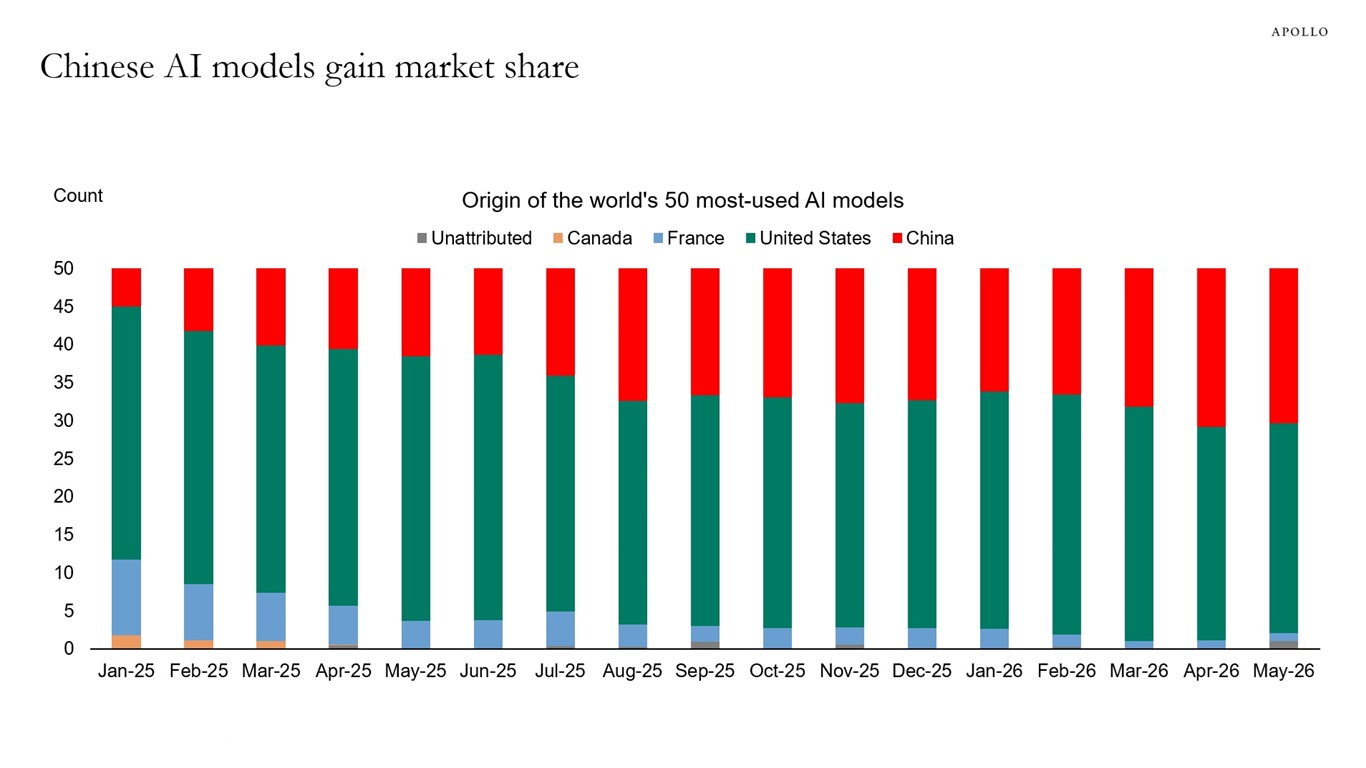

China has also been steadily increasing its presence among the world's 50 leading AI models. Data from April and May indicate that Chinese models have reached a record market share approaching 30%, underscoring how quickly the competitive landscape is evolving.

Source: Apollo Global Report (July 2026)

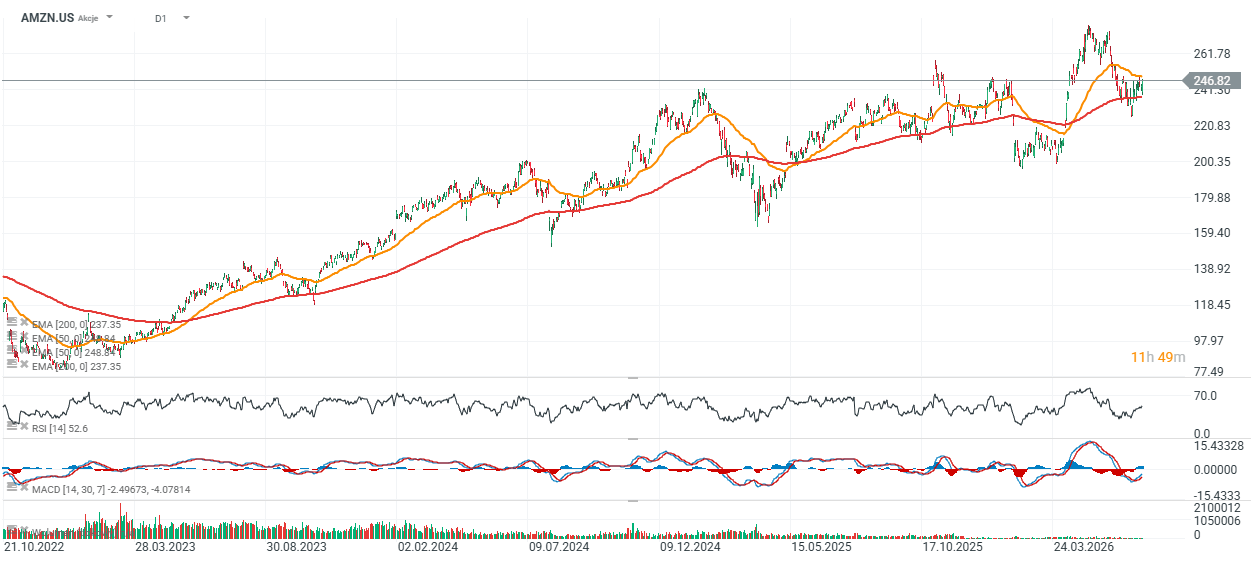

Amazon stock technical outlook (AMZN.US, Daily)

Amazon shares have remained in a long-term uptrend since 2023, rising by more than 300% from their cyclical lows. Despite this impressive performance, the stock has underperformed several other Big Tech names over the same period and currently trades only around 2% above its 200-day exponential moving average (EMA200), shown by the red line.

The primary support zone is located between $230 and $240, while the key resistance remains near the recent highs around $270 per share.

Source: xStation 5

What July can tell us about where stocks go next

Market Wrap: European equities at 3-week highs! Apple dips in US premarket!

Morning Wrap: AI Fuels the Rebound. Technology Makes a Strong Comeback

Apple is still impressive, but the market is no longer impressed

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.