Booz Allen Hamilton (BAH.US) is one of the most important technology contractors serving the U.S. government. The company operates at the intersection of defense, intelligence, cybersecurity, and artificial intelligence. Despite its undeniably strategic position, the stock has fallen more than 67% from its all-time highs, making it one of the biggest casualties of the political and budgetary shifts that have taken place in Washington.

- Booz Allen is also among the 12 companies expected to participate in the development of the U.S. Golden Dome missile defense initiative. The company is set to serve as a key systems integrator and has been awarded a contract to design and build a prototype space-based interception system known as Brilliant Swarms, an orbital interceptor concept designed to enhance missile defense capabilities.

- The valuation has compressed dramatically. Booz Allen currently trades at roughly 10x trailing earnings and approximately 12x forward earnings. Leverage remains relatively conservative compared with many peers. The stock trades at an EV/EBITDA multiple of around 9 and a price-to-sales ratio of approximately 0.8x, levels that appear unusually low relative to most defense contractors.

- In its most recent quarter, adjusted earnings per share came in at $1.78 versus consensus expectations of $1.34. Revenue declined 6.4% year-over-year to $2.78 billion, while headcount was reduced to approximately 31,500 employees from 35,800 a year earlier. At the same time, backlog increased 3.1% year-over-year to $38.2 billion. Management's fiscal 2027 guidance calls for revenue between $11.2 billion and $11.7 billion and adjusted EPS of $6.00 to $6.35.

What Triggered the Sell-Off?

The primary issue over the past several quarters has been revenue concentration. Approximately 97-98% of Booz Allen's revenue comes from U.S. federal contracts, making the company exceptionally sensitive to changes in government spending priorities. In addition, Booz Allen has historically generated a large portion of its business through high-end consulting and professional services. Investors increasingly question the long-term growth profile of labor-intensive consulting models as artificial intelligence expands the scope of automation across knowledge-based industries.

During the 2025-2026 period, investors began pricing in the impact of the DOGE cost-efficiency initiative, which aimed to reduce federal consulting and technology expenditures. The result was slower procurement activity, contract reviews, and, in Booz Allen's case, the cancellation of several contracts within its civilian segment.

The company also reduced guidance multiple times throughout fiscal 2026. The Civil Business segment experienced revenue declines of as much as 20-28%, leading investors to view the weakness as a potential structural problem rather than a temporary slowdown, even as demand from defense and intelligence customers remained healthy.

Why Were Investors So Concerned?

The market's concerns centered around several factors:

-

Heavy dependence on a single customer: the U.S. government;

-

Cancellation of numerous federal contracts following spending reviews;

-

Slowing growth after many years of strong execution;

-

Roughly 2,500 job cuts and restructuring within the civilian segment;

-

Risk of additional budget reductions under changing political priorities;

-

Repeated downward revisions to revenue and earnings expectations.

Where Might the Market Be Wrong?

Ironically, the strongest investment argument may have emerged only after the stock's collapse.

Investors have focused almost exclusively on the weakness in the civilian segment while largely ignoring the fact that the company's defense, intelligence, cybersecurity, and AI-related operations remain relatively resilient. Booz Allen ended fiscal 2026 with a record backlog of approximately $38 billion. More importantly, management continues to highlight accelerating demand across National Security, cyber, and AI-native product offerings.

Unlike traditional consulting firms, Booz Allen is deeply embedded within the U.S. national security infrastructure. Rising geopolitical tensions, the global AI race, and the modernization of military systems continue to drive demand for capabilities the company has spent decades building.

Fourth-quarter fiscal 2026 results highlighted an interesting paradox. Revenue growth has clearly slowed, but earnings per share, free cash flow generation, and profitability all exceeded expectations thanks to aggressive restructuring and cost optimization.

That said, the sell-off was not entirely irrational. The company entered a period of slower growth, lost several contracts, and faced meaningful political pressure tied to federal spending reductions. The key question is whether those challenges justify the current valuation.

Today's market pricing appears to reflect a scenario of prolonged stagnation. Yet the company's most strategic businesses—defense, cybersecurity, artificial intelligence, and intelligence services—continue to expand. Backlog remains near record levels, suggesting investors should ask not whether Booz Allen encountered problems, but whether the market has begun pricing those problems as if they will persist indefinitely.

The Ultra Mission Solutions Acquisition Is More Important Than It Looks

Booz Allen recently announced the acquisition of Ultra I&C Mission Solutions for $720 million, marking its largest acquisition since the $725 million purchase of Liberty IT Solutions in 2021.

Ultra Mission Solutions is a relatively small company with approximately 220 employees, including around 135 specialized engineers. At first glance, the purchase price may appear steep. However, Booz Allen is not acquiring revenue scale—it is acquiring technologies that are increasingly critical to modern military communications and battlefield management systems.

The company operates across three primary business areas:

-

Mission Software – command-and-control and battlefield management software;

-

Edge Compute – processing data directly at the point of collection;

-

Encryption Management – secure communications and encryption systems.

Its portfolio includes platforms such as Apex, ADSI, ACTS, Rain, and Knox, which support command-and-control operations, secure data transfer, edge computing, and encryption management in contested or disconnected environments.

Ultra's customers include programs supporting the U.S. Army, Air Force, Navy, and allied defense organizations.

Management expects the acquired business to generate double-digit revenue growth for several years while maintaining EBITDA margins above 20%.

For comparison, Booz Allen generated approximately $1.23 billion of EBITDA on $11.2 billion of revenue during fiscal 2026, implying an EBITDA margin of roughly 11%. Ultra therefore operates at nearly twice the profitability of the broader company.

A few years ago, Booz Allen was primarily viewed as a consulting firm and federal services contractor. Today, an increasing share of investment is being directed toward artificial intelligence, cybersecurity, command-and-control systems, edge computing, resilient communications, and next-generation defense technologies.

These are precisely the areas management identified as the company's key long-term growth engines during its fiscal 2026 results presentation. Despite a 6.4% decline in revenue to $11.2 billion, Booz Allen maintained strong profitability and finished the year with a record $38 billion backlog.

The acquisition of Ultra Mission Solutions strengthens the very businesses currently experiencing the strongest demand. Rather than simply waiting for government spending conditions to improve, Booz Allen is using this period of weakness to expand its exposure to defense, cyber, and AI markets that are already becoming the fastest-growing parts of its order book.

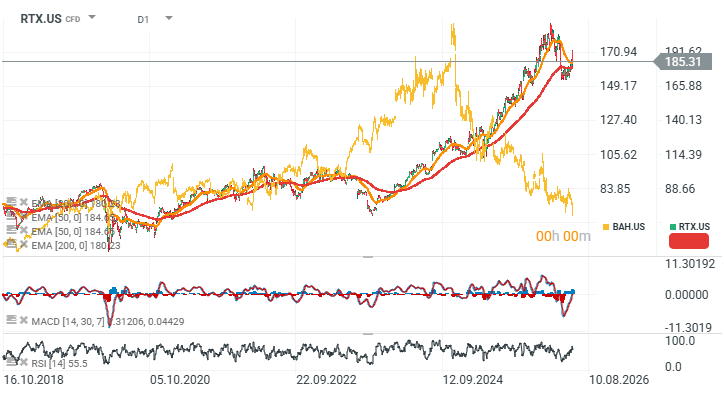

RTX vs. Booz Allen Hamilton (Daily Chart)

The chart below compares RTX (formerly Raytheon), one of the strongest defense contractors in the United States, with Booz Allen Hamilton (the golden chart). Investor sentiment has diverged sharply. While RTX continues to benefit from strong defense spending trends, Booz Allen is increasingly being viewed as vulnerable to AI-driven disruption within its consulting operations.

Source: xStation5

Eryk Szmyd Financial Markets Analyst

The Week Ahead

What July can tell us about where stocks go next

Market Wrap: European equities at 3-week highs! Apple dips in US premarket!

Morning Wrap: AI Fuels the Rebound. Technology Makes a Strong Comeback

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.