Consumer Inflation (CPI) – USA

-

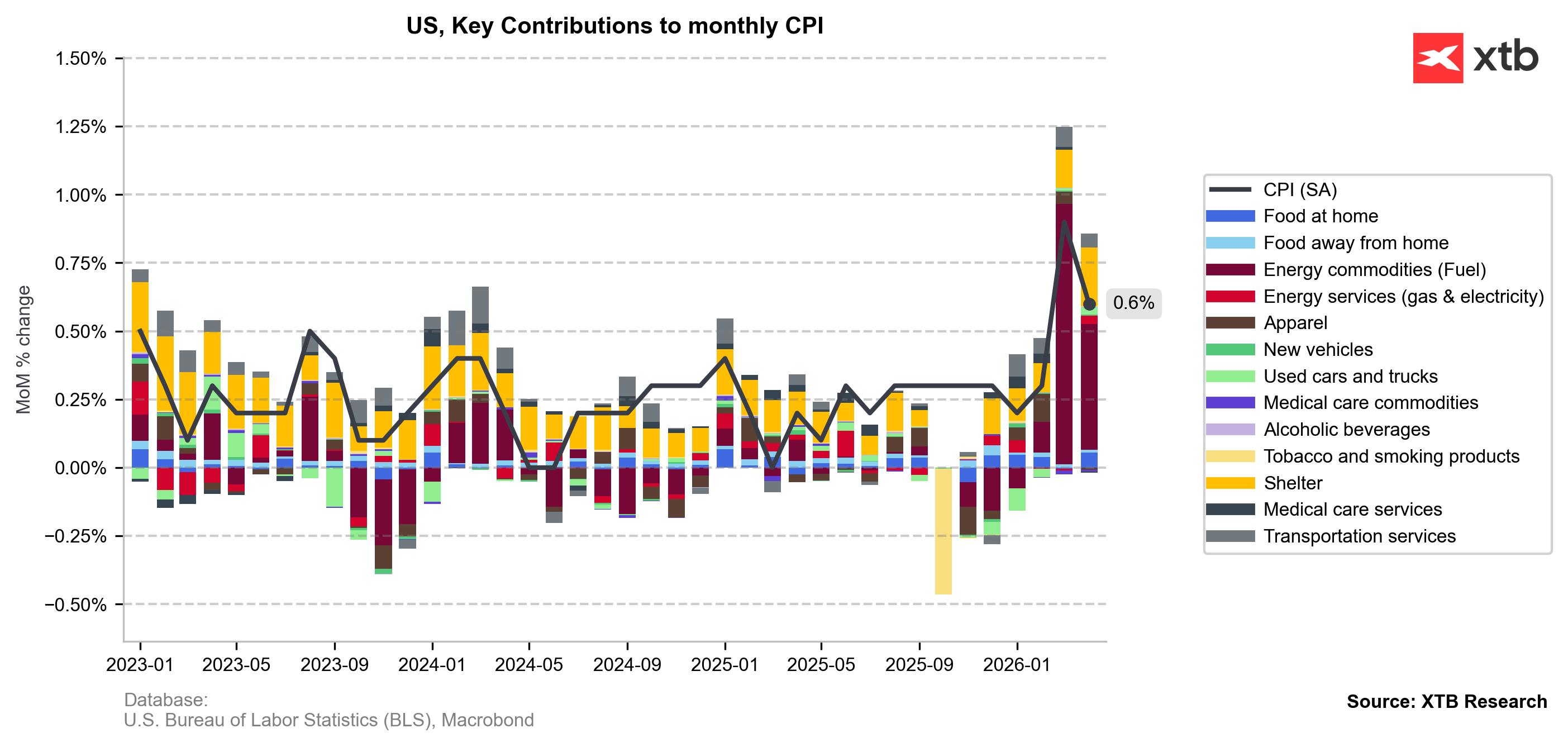

CPI Inflation (m/m): actual 0,6% forecast 0.6% (previously 0.9%)

-

Core CPI Inflation (m/m): actual 0,3% forecast 0.4% (previously 0.2%)

-

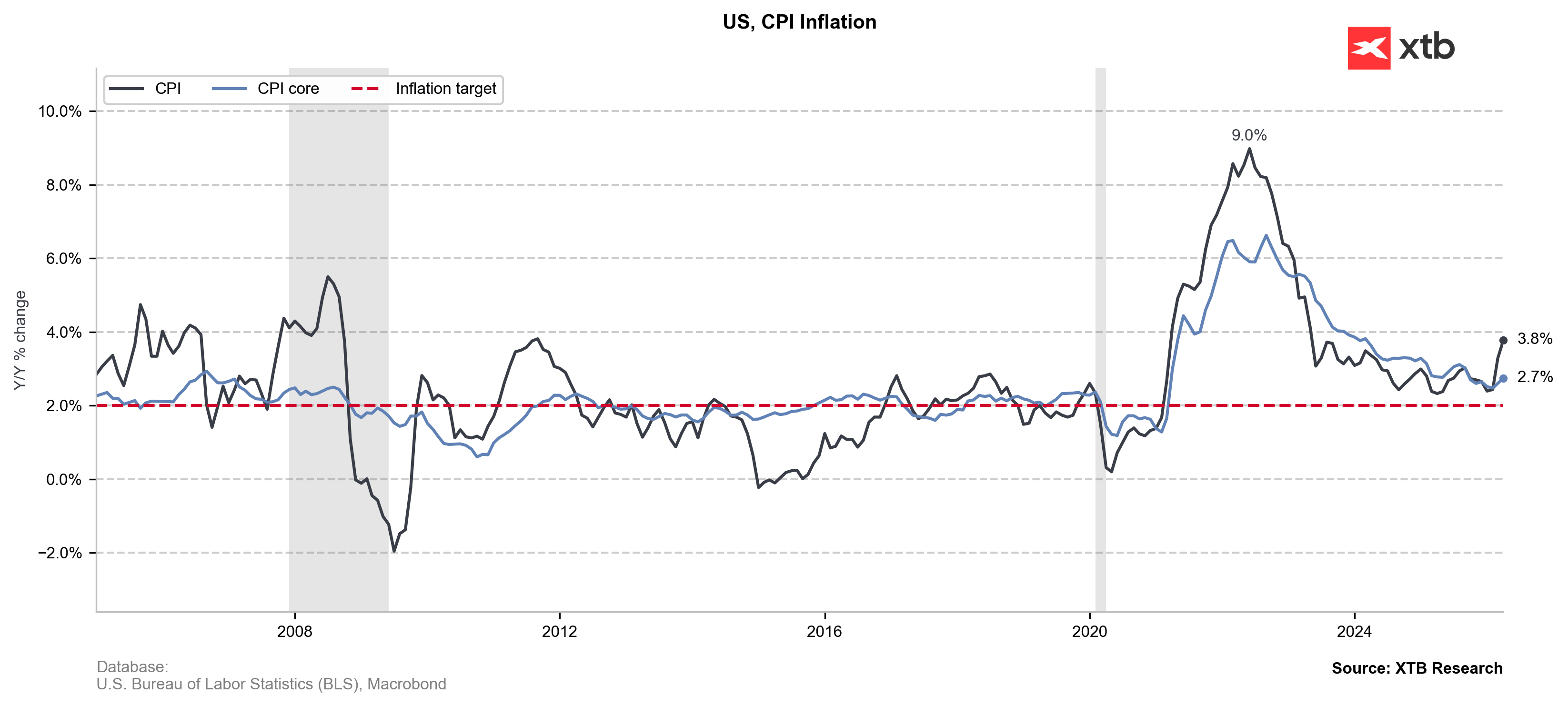

CPI Inflation (y/y): actual 3,8% forecast 3.7% (previously 3.3%)

-

Core CPI Inflation (y/y): actual 2,8% forecast 2.7% (previously 2.6%)

Why is this data important?

Consumer inflation (CPI) is the most important indicator measuring the pace of price growth for goods and services from the consumer’s perspective. It shows how the cost of living for households is changing and serves as a key reference point for the monetary policy of the Federal Reserve (Fed).

A higher-than-expected CPI reading suggests persistent inflationary pressure in the economy, which may increase the likelihood of interest rates remaining higher for longer or even further monetary tightening. On the other hand, weaker data may support expectations for interest rate cuts and a more dovish Fed stance.

Particularly important is Core CPI inflation, which excludes the most volatile components such as food and energy. This provides a clearer picture of long-term inflation trends and is closely monitored by the central bank.

The CPI report has a major impact on financial markets. Higher inflation typically supports the U.S. dollar and pushes Treasury yields higher, as investors anticipate a more restrictive Fed policy. Conversely, lower-than-expected inflation data may weaken the dollar, support equity markets, and increase expectations for future rate cuts.

Actual Data

The latest U.S. CPI report delivered mixed signals for the market. Monthly headline inflation matched expectations at 0.6%, while Core CPI came in slightly above forecasts at 0.4% versus the expected 0.3%, suggesting some moderation in underlying price pressures in the short term.

However, annual inflation figures surprised slightly to the upside. Headline CPI accelerated to 3.8% y/y, above the 3.7% consensus and significantly higher than the previous 3.3%. Core CPI also rose to 2.8% y/y, exceeding expectations of 2.7%.

Overall, the data still points to persistent inflationary pressure in the U.S. economy, even though the softer monthly core reading may provide some relief to markets. The report is likely to keep the Federal Reserve cautious regarding potential interest rate cuts in the near term.

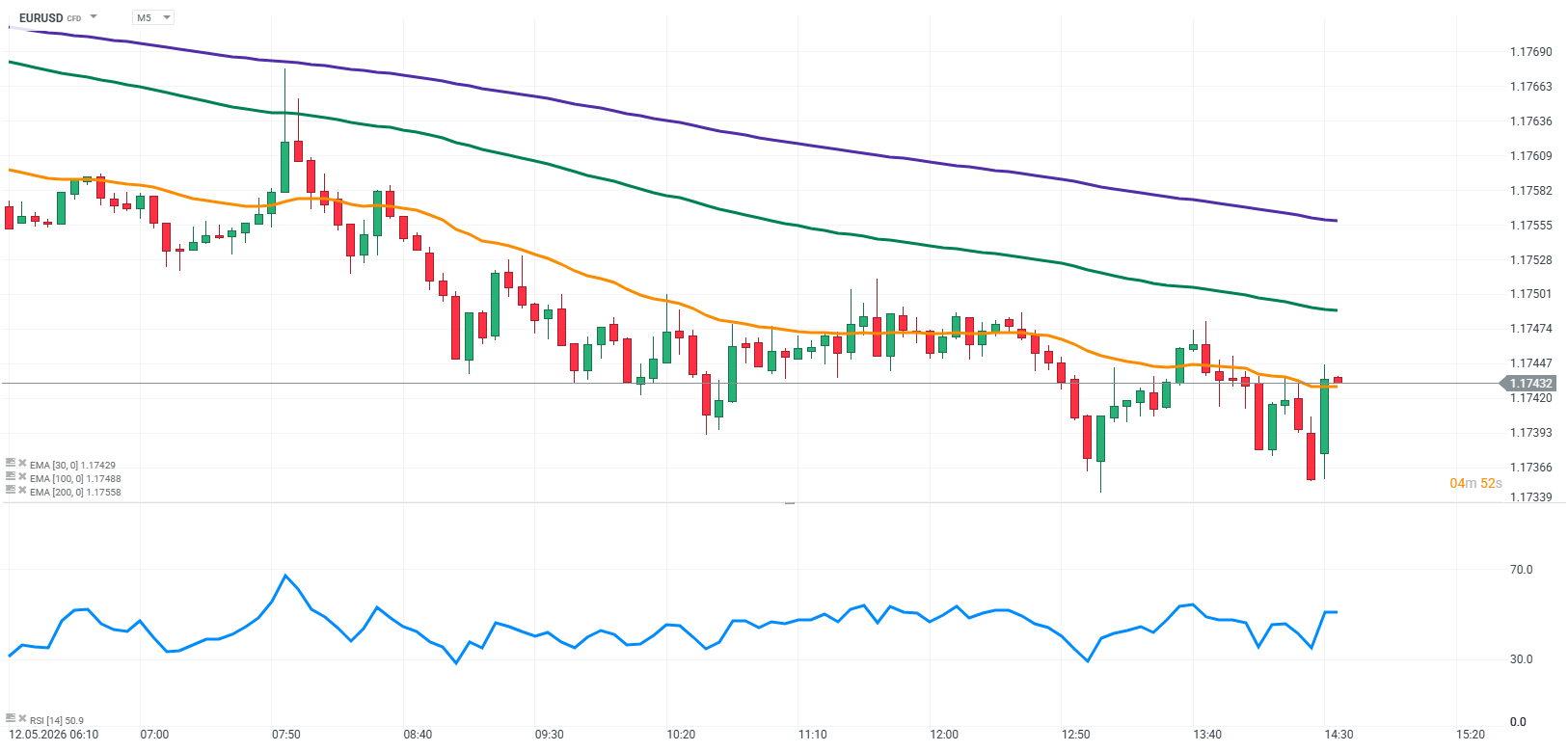

For financial markets, the higher yearly inflation readings may support the U.S. dollar and Treasury yields, while limiting bullish momentum in equities. In the FX market, EUR/USD could remain under pressure as investors continue to price in a relatively hawkish Fed stance.

Source: xStation5

Daily Summary: Wall Street Regains Ground; Another Intervention in the Yen Market❓

Three Markets to Watch Next Week (July 31, 2026)

What July can tell us about where stocks go next

Market Wrap: European equities at 3-week highs! Apple dips in US premarket!

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.