Market expectations for the results:

- Revenue above USD 22 billion

- Earnings per share (EPS) above USD 2

However, there is no shortage of optimists even among the most prestigious institutions.

- Jefferies and Morgan Stanley expect revenue to rise to around USD 29 billion. What will matter more than the headline results, however, will be specific figures in the key segments (cloud and AI) and the outlook.

- AI-related revenue could reach around USD 17 billion, primarily thanks to growth in the networking segment, deployment of new switches, and increasing share in optics.

- A key factor here will be Anthropic’s USD 10 billion order, which has been shifted from deliveries of full server racks to chips only. As a result, revenue from this contract could come in around USD 2.0 - 2.5 billion.

- Morgan Stanley, meanwhile, notes that it is seeing AI rack-related demand being pushed out to 2027, but views this as a timing issue rather than lost orders. The bank’s analysts believe production capacity is being redirected to other TPU customers.

The most important element of the earnings release may not be the current quarter itself, but management’s commentary regarding 2027.

Semiconductor companies are currently experiencing a growth wave rarely seen in developed markets. This is the result of massive CAPEX spending by so-called hyperscalers and entities developing AI solutions. In this context, operating leverage is enormous, while the reliability of current forecasts is limited. Company statements about the pace of further growth will be crucial for the market in terms of future valuations.

- Broadcom’s revenue from AI chips could then exceed USD 120 billion, above management’s earlier indication of more than USD 100 billion.

- Analysts note, however, that recent discussions in the Asian supply chain have been less optimistic than expected, limiting the scope for potential positive revisions.

- Some investment banks still see room for further guidance upgrades as ASIC programs expand.

A separate topic is the risk of competition from MediaTek in Google’s TPU supply chain. Morgan Stanley believes the threat is manageable and estimates that around 15% of TPU content could realistically be at risk.

In analysts’ view, Broadcom should retain most of the business, as replacing an incumbent supplier at this scale is difficult. This could become an important theme if management decides to address it.

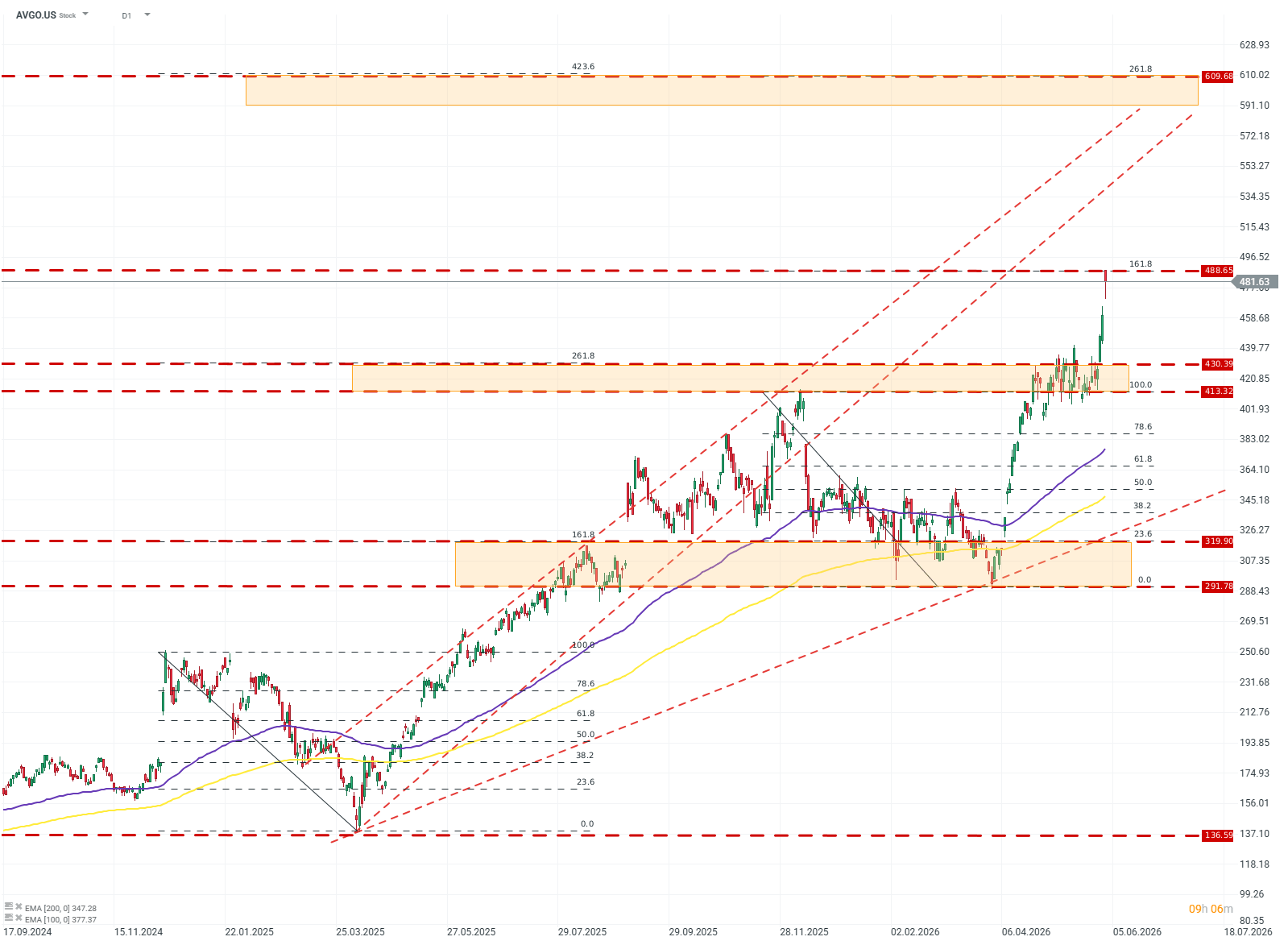

AVGO.US (D1)

From a technical standpoint ahead of the earnings release, the share price has stalled at the 161.8% Fibonacci extension level, drawn from the price move between December 2025 and April 2026. If the bullish scenario continues to play out, a potential upside target for buyers could be around USD 600, where Fibonacci extensions (423.6%) from 2025 overlap with a new extension from 2026. Potential resistance could also come from the trend channel (marked in red). If a correction occurs, the first support level and downside target for sellers would be around USD 430. Source: xStation5.

Daily Summary: Nasdaq 100 Up 3.2% – Is the Bull Market Back? (04.08.2026)

Palantir Earnings: High Expectations and Even Bigger Gains

Daily Summary - The market starts to doubt rate hikes after Warsh, but Trump destroys the rebound

US OPEN: Wall Street Holds Its Breath Ahead of Fed Decision and Tech Giant Earnings

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.