The easing of tensions in the Middle East is allowing investors to shift their focus back to macroeconomic data from major economies. However, the beginning of the week is not overly packed in this regard, and today's most crucial data releases are already behind us.

Macroeconomic Data

Monday

- German factory orders disappointed heavily, recording a deep decline of 3.8% month-on-month in April. This is yet another data point that does not inspire optimism regarding economic growth within the common bloc.

- The ECB interest rate decision and President Christine Lagarde’s press conference are scheduled for Thursday. If she highlights economic bottlenecks, the euro could come under pressure.

- According to a survey conducted by the New York Fed, one-year inflation expectations in the United States fell slightly from 3.6% to 3.5%. However, markets are already eagerly awaiting Wednesday's CPI report.

Tuesday

- German industrial production data came in slightly better than consensus, easing concerns sparked by yesterday's factory orders reading. The year-on-year decline was just 0.5%.

- China recorded a surprisingly strong rebound in trade. May exports surged by as much as 14.1% YoY. Despite an even more dynamic growth in imports (27.4% YoY), the trade balance increased.

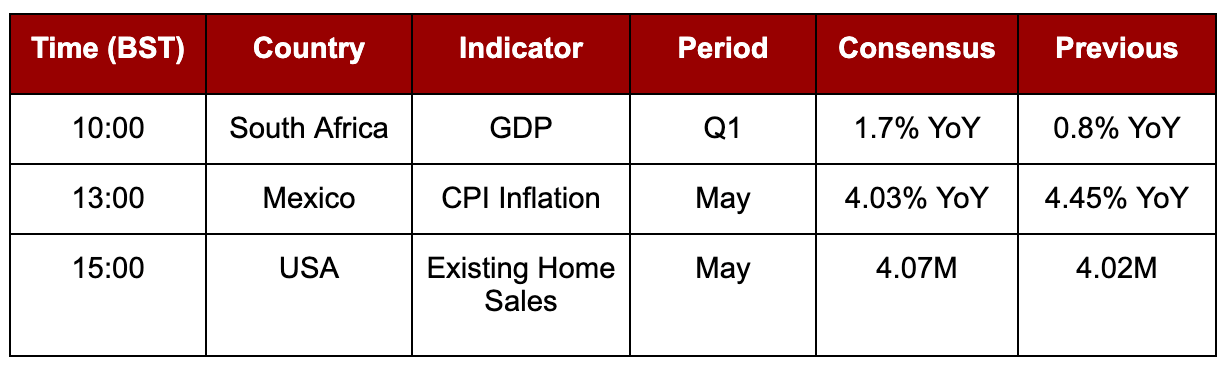

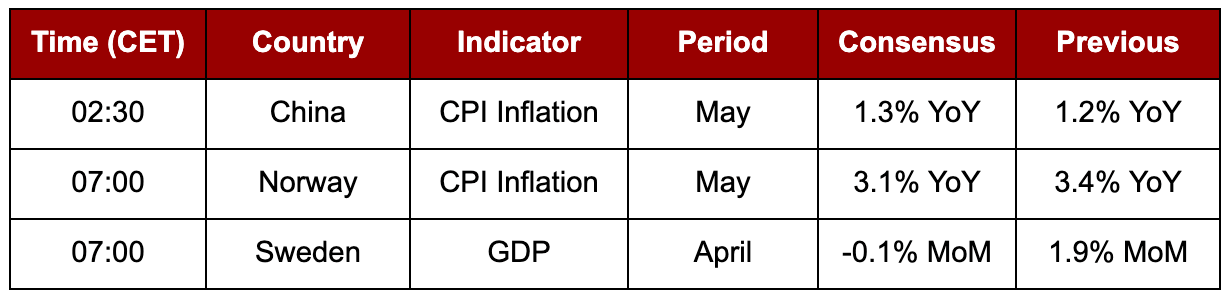

Macroeconomic Calendar

Tuesday

Wednesday (Morning Hours)

Earnings Calendar

Europe

- Bellway PLC (BWY.LN) – BMO (Before Market Open)

- Oxford Instruments (OXIG.LN) – AMC (After Market Close)

USA

- J.M. Smucker Co. (SJM.US) – BMO (Before Market Open)

- Casey’s General Stores (CASY.US) – AMC (After Market Close)

- Cracker Barrel (CBRL.US) – AMC (After Market Close)

3 Markets to Watch

- Euro (EUR) The common currency is awaiting Thursday's ECB meeting. The central bank is expected to make a decision regarding the first interest rate hike in the current cycle. This is already fully priced in by the markets, so attention will shift toward President Lagarde's press conference.

- US100 Following Friday's decline, US indices are beginning to find their footing. Investors remain concerned about the prospect of a deeper correction. News from the Middle East remains critical.

- Norwegian Krone (NOK) The Scandinavian currency remains heavily dependent on shifts in market sentiment and highly volatile energy commodity prices. Tomorrow morning, it faces another challenge with the release of May's inflation data.

—

Michał Jóźwiak, Financial Markets Analyst at XTB

Cocoa loses 4% amid news from Ghana 🚩 What's next for the market?

Oil Pulls Back After Strong Gains 🚩 Markets Assess the Strait of Hormuz Impasse

Chart of the Day: USDJPY Rises Again. Intervention Is Not Enough — Markets Await BoJ Action

Economic Calendar: RBA Holds Rates, Markets Await US Housing Data

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.