The Personal Consumption Expenditure (PCE) price index, Fed’s preferred inflation gauge, will take center stage as the most anticipated data release in today’s macroeconomic calendar. The main difference between CPI and PCE is that the latter covers a broader range of goods and services, as well as indirect payments like employer-paid healthcare.

Although markets are broadly expecting the uptick in monthly (MoM) PCE change (in line with the most recent CPI dynamics), the signals from personal consumption levels may appease Fed’s hawkish stance on further cutting. Consumer spending is expected to increase by 0.1%, compared to the 0.7% hike in December 2024. This, accompanied by increased savings and expected slowdown in wage growth, may result in higher rate cut expectations, albeit the consumer inflation fears creeping in have a potential to outweigh market’s positioning in that matter.

What to expect from the upcoming report?

-

Monthly core PCE likely to increase to 0.27% (from 0.16% in December)

-

Driven by price resets in accommodation, recreation services, and nondurable goods

-

Year-over-year core PCE inflation expected to decline to 2.6% (from 2.8% in December)

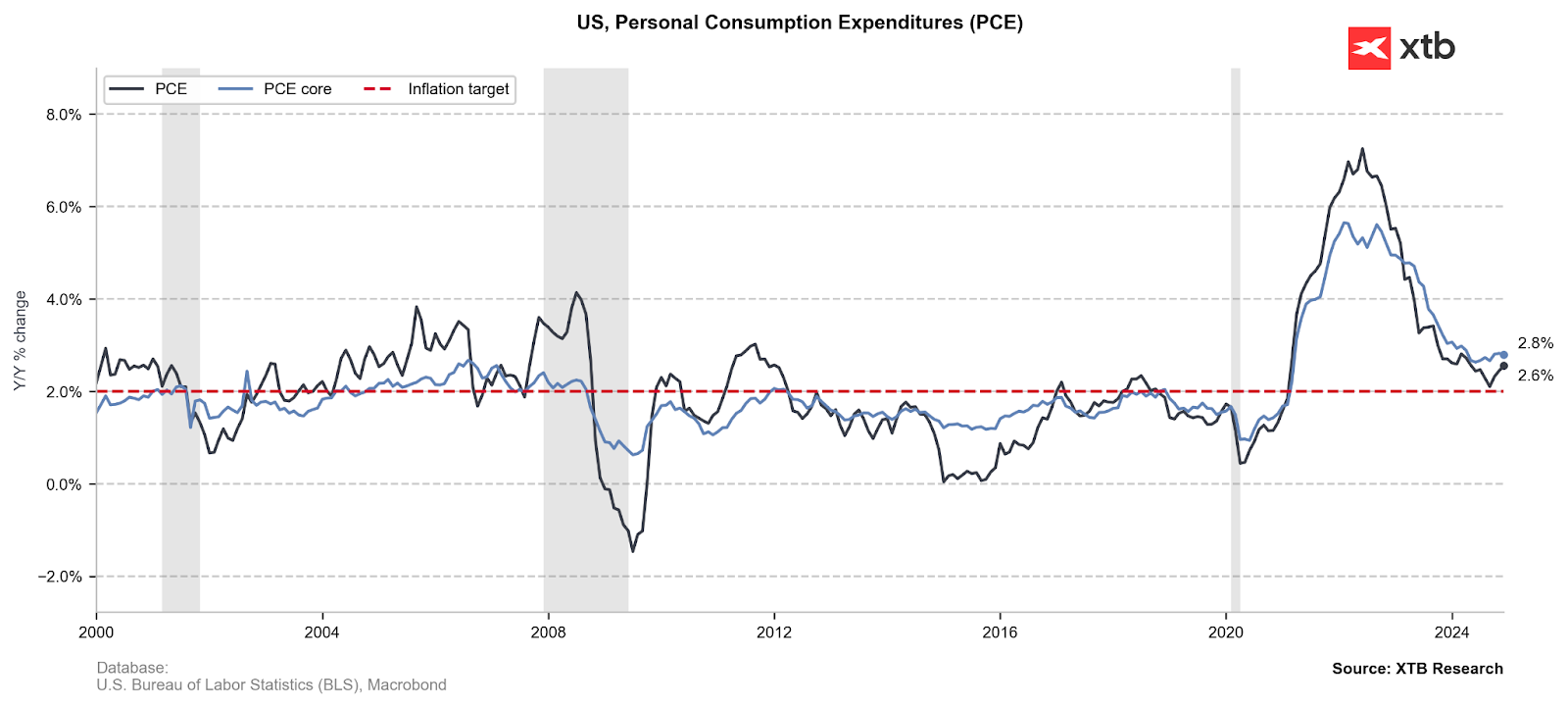

December’s PCE hiked considerably from near target to 2.6%, while core reading remained rather sticky, holding onto 2.8% for the third consecutive month. Source: xStation5

Key inflation drivers last month

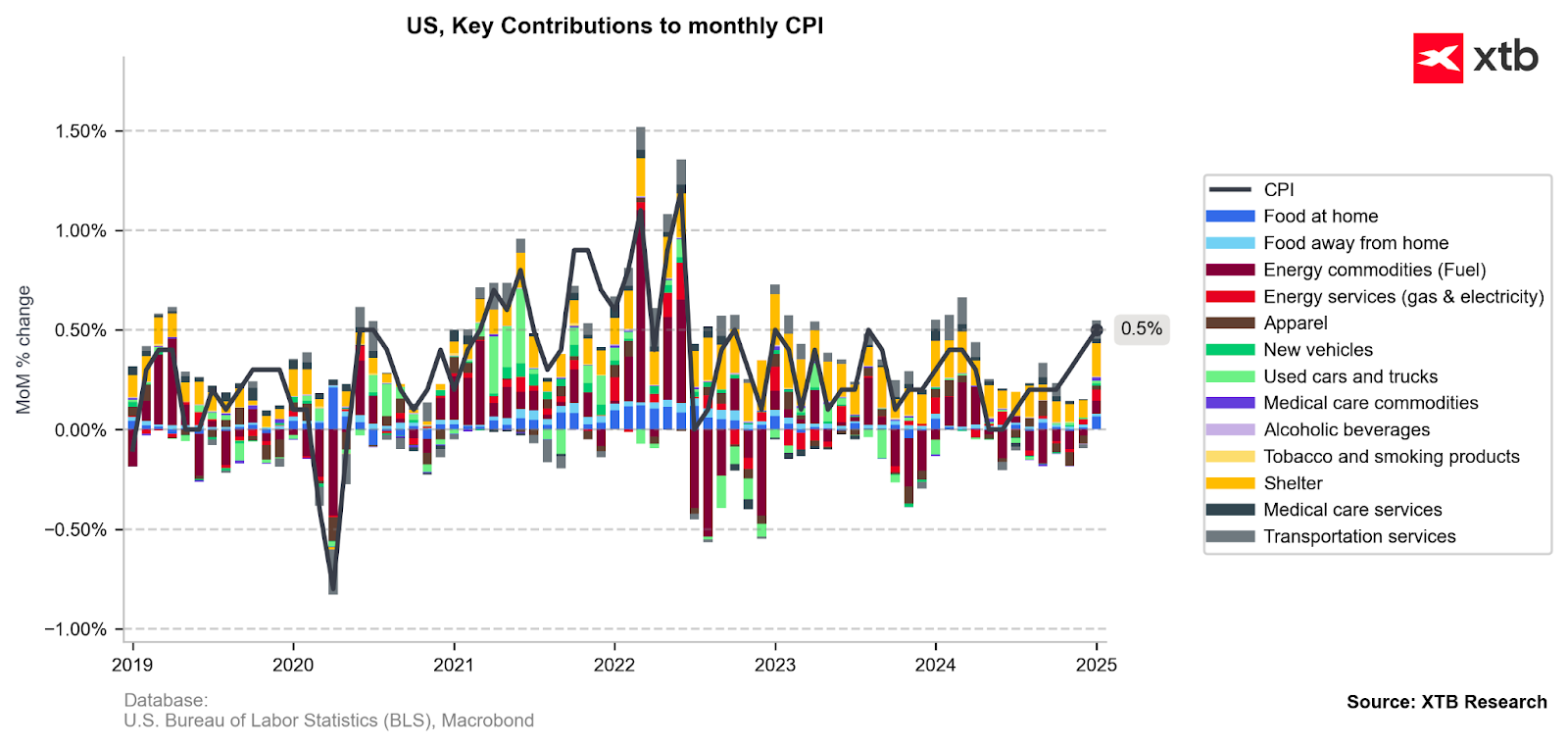

Aside from shelter inflation, last month’s elevated CPI reading was driven mainly by food and energy prices, which justifies the expected drop in less volatile core PCE YoY reading. What will likely contribute to the index, however, are the recreational services and durable goods prices, as well as an overall price reset at the start of the year, higher than expected due to the elevated inflation expectations.

All main CPI categories weighed on prices in January’s CPI reading. Source: xStation5

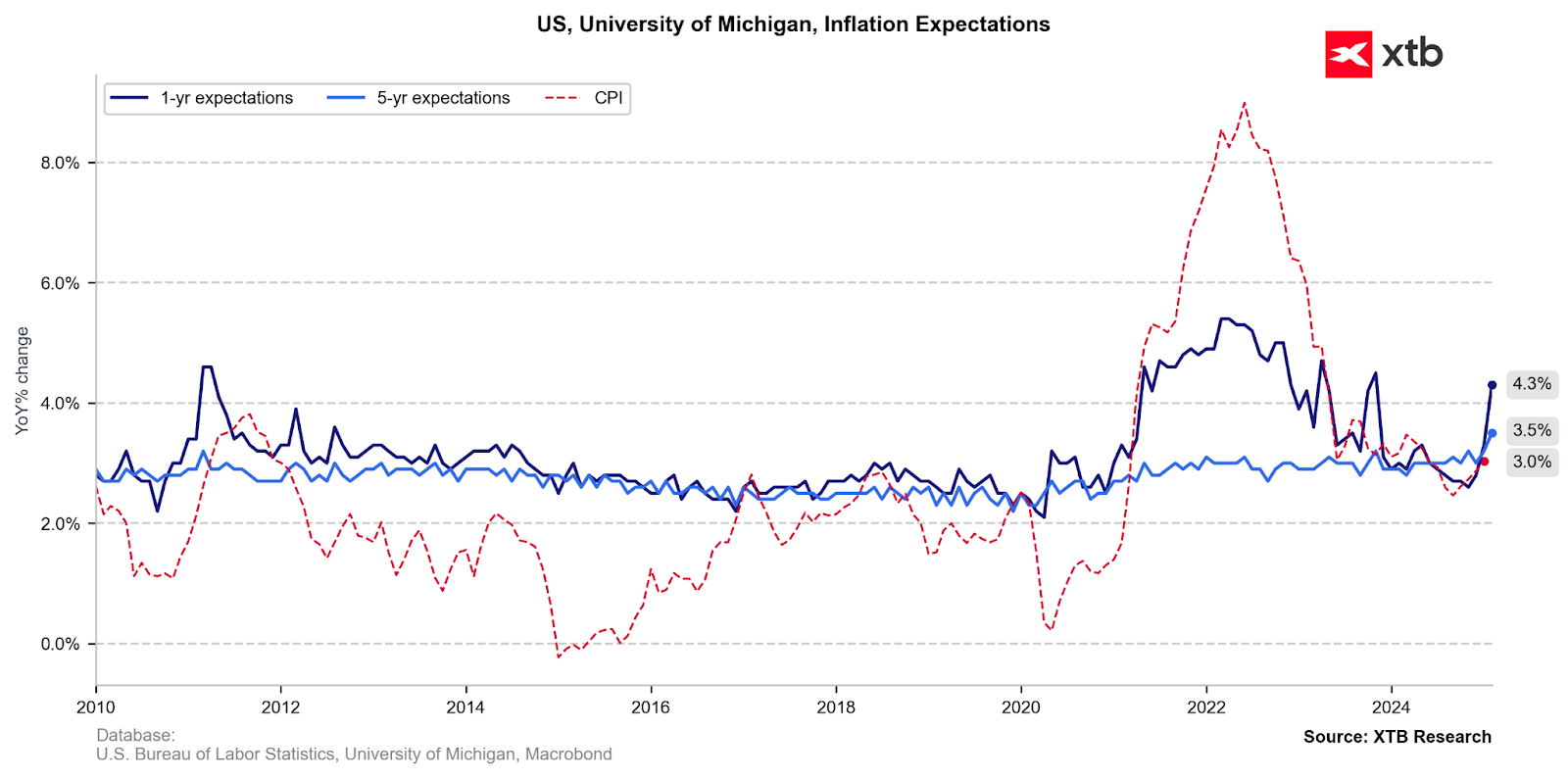

Inflationary expectations continue to climb

The latest report on inflationary expectations by University of Michigan freaked out the markets alongside a rather dismal PMI reading. After previous jump in long-term expectations to 3,5%, one-year expectations followed, surging to 4.3% on fears of consequences of Trump’s trade policies.

Source: xStation5

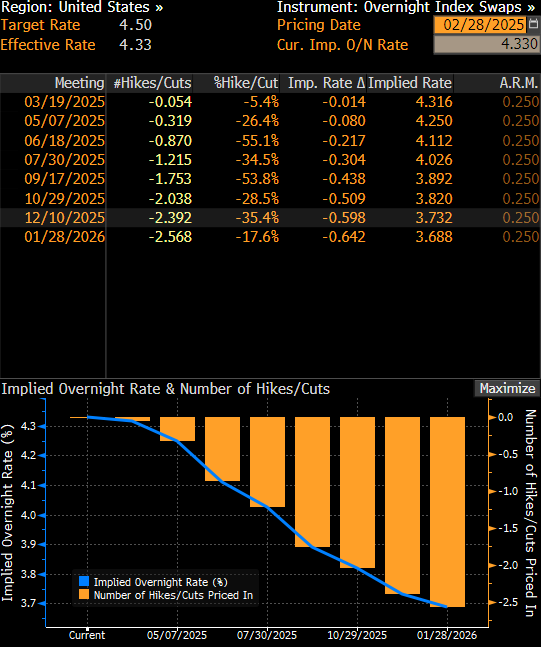

Fed is not expected to cut rates in the first half of 2025, as Trump’s tariffs effect may trigger a return of price pressures in the US economy, as reflected by consumers’ fears. Source: xStation5

EURUSD is recovering slowly from yesterday's dip, caused by the dollar's rally on tariffs announcement. A significant drop in consumer spending may narrow down the gap between cut-expectations for Fed and ECB this year, motivating further appreciation of euro. Source: xStation5

BREAKING: Eurozone recovery? Positive PMI data tempered by high oil and gas prices

Economic Calendar: Industry’s condition in the shadow of oil prices

Daily Summary: Trump's War Threats Weigh on Markets. Wall Street Sinks into the Red

Economic Calendar: Big Tech, Tensions Over Iran, and the ECB’s Decision ⏰

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.