Carl von Clausewitz, one of the most important military theorists in history, once said that “War is merely the continuation of diplomacy by other means.” This statement describes relations between the US and the Middle East remarkably well, and in recent months Donald Trump has put it into practice, allowing markets to observe these diplomatic struggles in real time.

Continuing the thread from this article: [LINK], the market may, over time, be forced to do something it has clearly avoided in recent months: pricing in scenarios that are difficult and painful for the economy.

Summary of the current status of negotiations between Iran and the US:

- A memorandum has been signed regarding the end of the conflict in Iran. Importantly, this is an arrangement, not a treaty.

- The actual end of the war is supposed to occur by 17 August. Until then, both sides are meant to reach agreement on disputed issues, such as the status of Iran’s nuclear program.

- In exchange for a series of military concessions, Iran is expected to receive a gradual lifting of sanctions, the return of frozen assets, and even investments.

Both the alleged concessions and the lifting of sanctions are deeply problematic.

- As for concessions, nothing suggests that Iran has any intention of scaling back its nuclear program in any capacity. It explicitly points out that there is no question of allowing inspectors from the International Atomic Energy Agency anywhere near Iranian facilities.

- To provide the necessary context: Iran is working on nuclear weapons. The Islamic Republic admits it is enriching uranium to roughly 60%. The vast majority of nuclear reactors use fuel enriched up to 5%, while some specialized reactors and devices use uranium enriched to 20%. Every additional percentage point of enrichment is a battle between humans and physics. It is expensive and time consuming, and it produces a material with only one practical use: a nuclear weapon.

- This nuclear program is one of the two instruments of pressure available to Iran, and it is also the threat that prevents the US from fully disengaging from the conflict.

On sanctions, the situation is even more complex

- Setting diplomatic and geopolitical issues aside, lifting sanctions requires Congress’s approval. Both parties in Congress, and Republicans in particular (Donald Trump’s faction), have spent decades systematically degrading

- Iran’s economy since the 1979 revolution. It will be difficult to expect them to agree to lift sanctions simply to save, statistically, the most unpopular president in history from failure. This is before even considering the list of entities responsible for terrorism, which includes most of Iran’s decision makers.

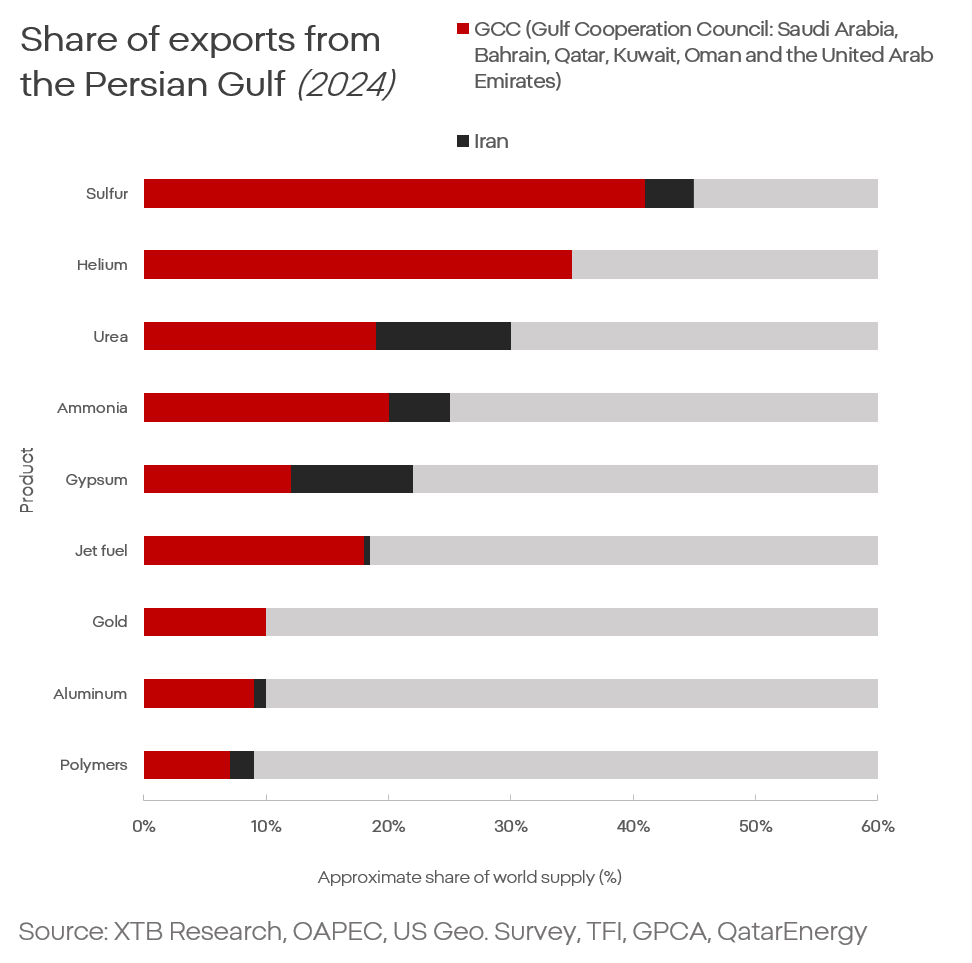

Gulf region share in trade volume (exports) [2024]

What this means for the market: a prolonged, relatively low intensity conflict

This brings the market to a single conclusion: a long lasting conflict of relatively low intensity. There are around 130 active armed conflicts of varying intensity worldwide. The conflict involving Iran is not unique. What is unique is that it is being waged in a region that supplies around 25% of global oil and gas, 30% of jet fuel, 30% of helium, and around 10% of aluminum.

What does this mean for the global economy?

First and foremost, we must abandon the expectation that the conflict will end due to economic pressure and an “apocalyptic crisis” that would supposedly inevitably follow from continued disruption of the Strait of Hormuz.

- First, today’s global economy, especially in Europe, is less dependent on fossil fuels than it was in the past.

The displacement of fossil fuels by renewable energy is not a utopian vision of activists. It is market reality and a trend that has lasted for decades and will accelerate as unrest in the Middle East escalates.

- Second, the biggest losers from a closed strait are not Europe (in economic rather than financial market context) or the US, but Asia (and to a lesser extent Africa due to fertilizers).

- Third, even if the Strait of Hormuz becomes impassable, the world is not defenseless against oil shortages, especially as wealthier and more developed countries are better prepared to handle higher prices.

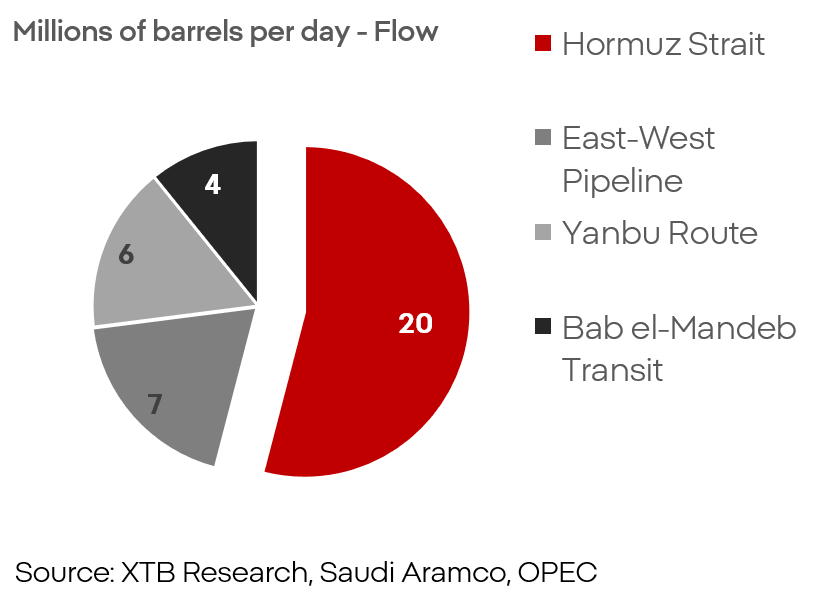

Share of transport routes in exports from the Gulf states

With that in mind, even assuming a total and permanent blockade of the Strait of Hormuz, the sea route accounts for “only” around 50% of transport volume from the region. This means the potential supply shock would affect roughly 10% of global supply, not more than 20%.

VLCC supertanker orders (1995-2026)

That the market is not pricing in a full and permanent blockade of the strait is visible in supertanker orders. Fleet expansion is at a record level, and analysts in this industry have good reasons for confidence. The risk posed by Iranian forces is real, but not sufficient to keep the strait under genuine control.

A precedent for how quickly an economic bloc can recover after a deep supply shock is the outbreak of war in 2022. Europe was eventually cut off from enormous gas supplies, and later oil. Russia was convinced Europe would not survive economically without Russian gas. Despite severe turbulence, the continent was ultimately able to almost fully decouple from imports from Russia. However, this did not happen without heavy blows to the economy and markets.

Is there something to fear?

Absolutely. The risk is real, but its nature is completely different from what most of the market expects. The risk is not an economic or market catastrophe on the scale of 2008. The risk is prolonged inflationary pressure, heightened risk premia, more expensive financing, a weaker consumer, and weaker growth. The situation today is not so dire as to expect another “lost decade” like the 1970s, but the pressure is and will remain real.

The greatest risk currently lies in the countermeasures and their effectiveness.

Renewable energy sources and electric vehicles are becoming less a matter of worldview and more a condition for survival, especially for Europe and many Asian countries. However, these technologies have drawbacks and issues that will need to be addressed, just as dependence on the Gulf states or Russia must be addressed.

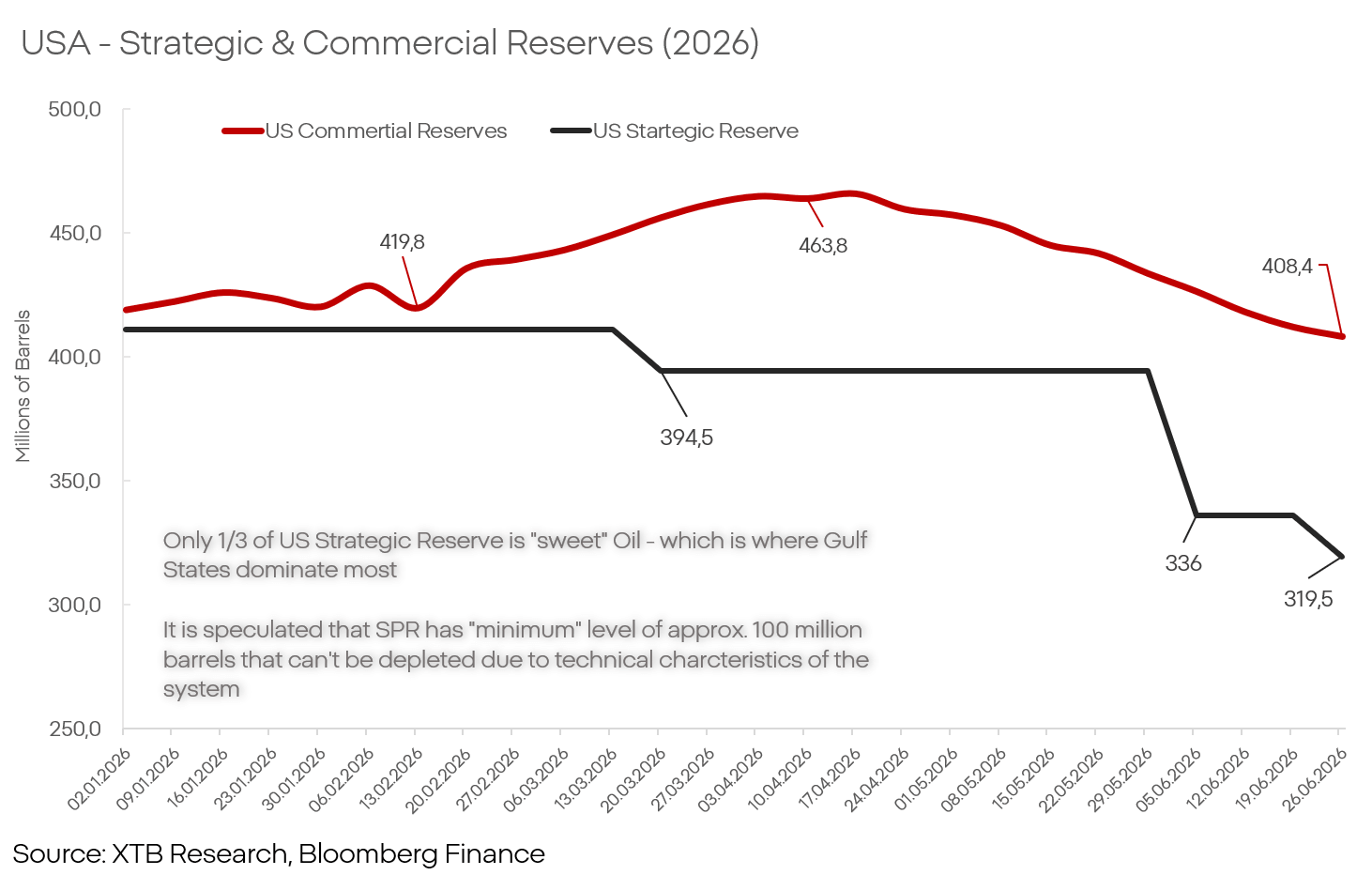

US: Strategic and commercial oil inventories (2026)

Oil inventories in the US, Europe, or China are sufficient to cushion price increases for several months up to even over a year, but they are not unlimited.

The wild card, again: China

China is one of the most important pillars of the global economy, yet it is only during periods of heightened inflationary pressure that it becomes clear how crucial Chinese factories are to maintaining the economic and market status quo.

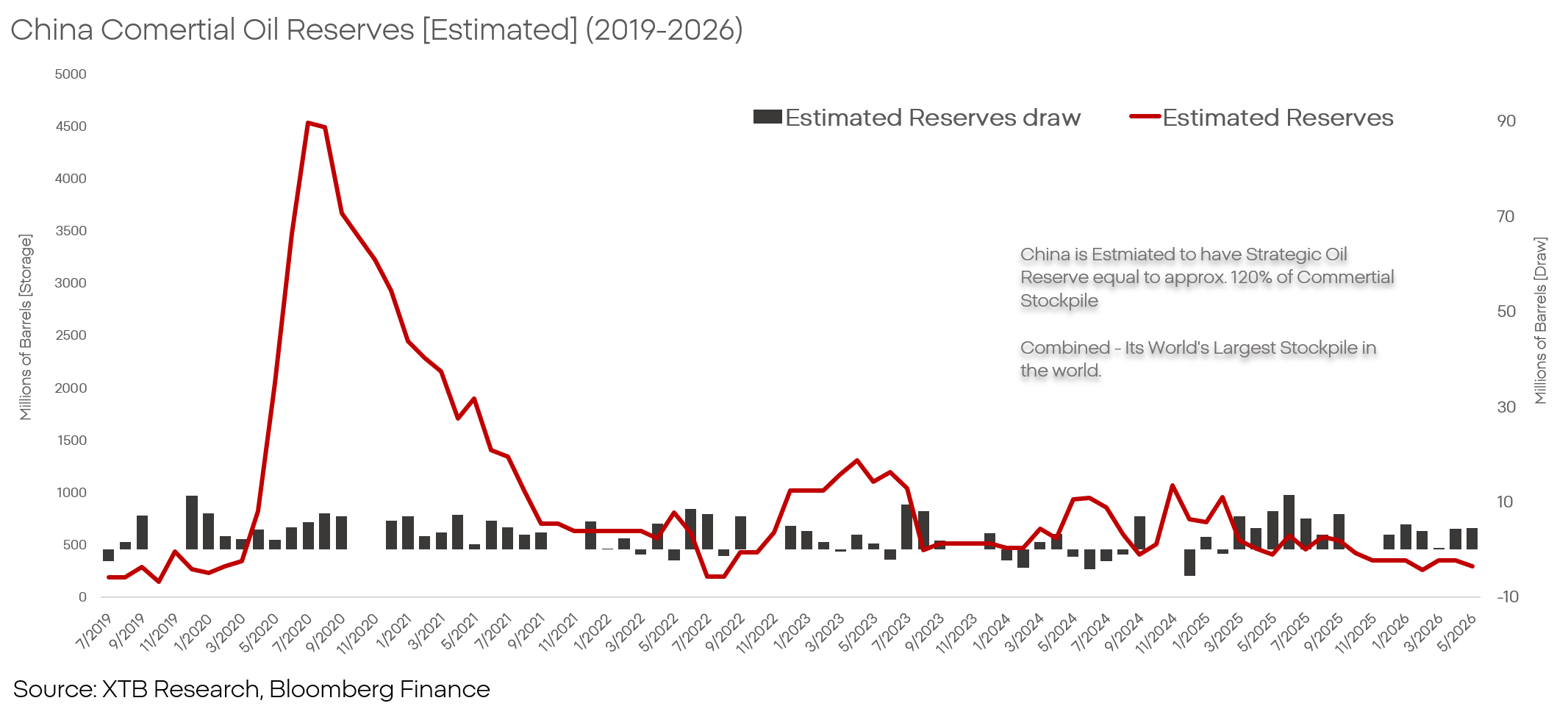

China: Estimated commercial oil inventories (2019-2026)

China is currently undertaking an interesting economic maneuver. It has enormous oil reserves, and since the beginning of the conflict these reserves have been released so that the Chinese economy can operate without disruption even under supply shock conditions.

By sustaining exports, and in some places even increasing them at the expense of its own oil reserves, China acts as a huge “sponge” that neutralizes inflationary pressure while continuing to increase its market share, driving out companies that do not have access to oil at “off market” prices.

China can continue this policy, or it can abandon it over time. Both scenarios will have enormous ramifications for the global economy and markets.

Market participants

Despite the unstable and hard to predict geopolitical situation in the region, and the decision making processes in both Washington and Tehran, the biggest losers and winners from further unrest in the Persian Gulf can already be identified today with a certain degree of confidence.

Winners

- Chevron (CVX.US): A rise in companies involved in oil production and refining seems only a matter of time. The market cannot ignore such strategically positioned companies forever, although it is worth noting that not all companies are equal. Fundamentally, the leader of the pack is Chevron. This is supported not only by its exposure to a strategic sector, but also by its purchase of Hess (diversifying growth beyond the Permian Basin), its stakes in Guyana, and the best positioning to restore operations in Venezuela.

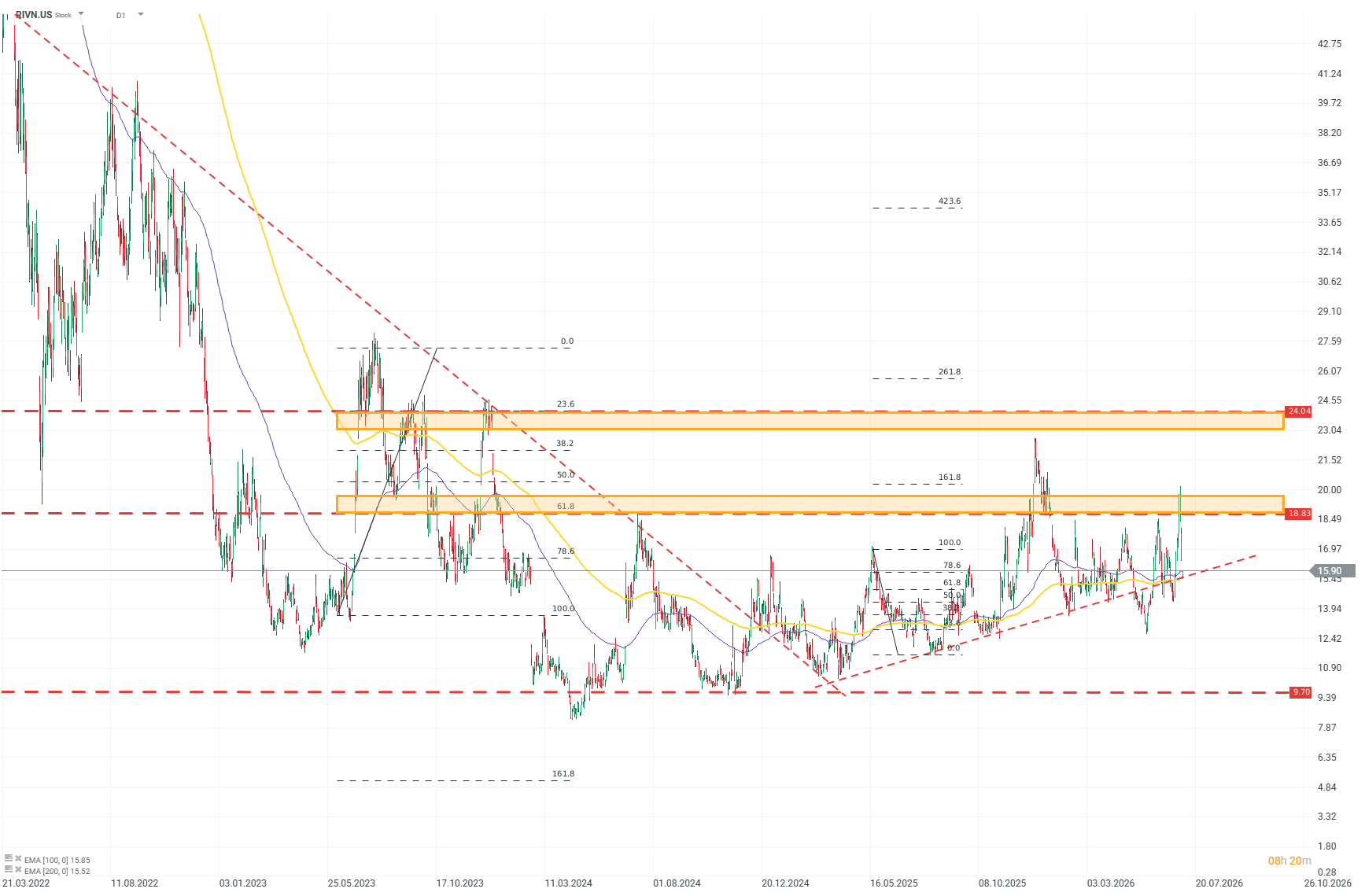

- Rivian (RIVN.US): The electric vehicle market, even under the most favorable circumstances, is intensely competitive. Tesla’s conglomerate, EV models from “legacy” automakers, and huge Chinese brands are compressing margins in the sector to the low teens, which does not justify the risk and spending required to develop new technologies. To succeed in this sector, you need a clear concept. Rivian has one.

- In house solutions and an agile, lightweight corporate structure allow the company to exploit competitors’ shortcomings and respond to the market in ways that are impossible for larger firms. Given Tesla’s valuation still completely detached from fundamentals, the grim outlook for European automakers, and the margin killing environment created by Chinese producers, Rivian could become the sector leader in the coming years.

Technical analysis of Rivian (D1)

Looking at the chart, it is clear the market is cautiously but steadily regaining confidence in the company. After bottoming in mid 2024, the stock gradually built upward momentum, which clearly accelerated toward the end of 2025. Based on Fibonacci levels, a strong resistance level for buyers can be identified around USD 19, and a potential target around USD 24. Source: xStation5

- SolarEdge (SEDG.US): The company is changing direction and expanding its ambitions, from stabilization to growth. Given the market context, it is hard to imagine a better moment. The company is improving results even under heavy pressure from Chinese competitors. Revenue increased by 31% in 2025 after a 70% drop in 2024, and our 2027 scenario indicates Europe will achieve 20% sales growth versus consensus. Gross margin increased to 17% in 2025. The company’s profile, business model, and portfolio make it one of the key beneficiaries of the ongoing and accelerating transformation in the electricity market.

Losers

- Europe: The biggest loser in terms of the broader financial market is Europe. Far reaching dependence on imports will put pressure on inflation expectations, forcing the ECB to keep interest rates higher for longer than most of the economy would like. Two segments of the European economy are especially sensitive:

- Legacy automakers: The traditional leaders of the automotive industry (BMW, Volkswagen, Stellantis, or Volvo) have been struggling for some time with serious problems and meeting expected results. A weakening consumer and reputational losses, cost pressure and regulation, and a war with China that manufacturers in the US and Europe are consistently losing. US companies will cope somewhat better due to the huge domestic market and extensive US protectionism, but European producers will be hit by negative factors with double force and will lack any buffers that could slow the decline.

- Luxury: Luxury companies (LVMH, Hermès) were until recently considered unbeatable champions in defending margins against inflation, but markets could only tell that story as long as conditions in China and the Middle East were not threatened. Growth momentum for these companies has been clearly slowing for some time, and in the context of capital retreat from the Persian Gulf and slowing growth in China, this legendary margin resilience may become history.

Kamil Szczepański

Financial Markets Analyst, XTB

France Challenges Palantir, Market Reacts.

Morning Wrap: US halt to attacks balanced by semiconductor sector declines (28.07.2026)

Oil Slides Ahead of the Weekend!

BREAKING: Eurozone recovery? Positive PMI data tempered by high oil and gas prices

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.