Markets continue to break their historical highs, at a time when central banks are starting more aggressive rate cut programs than expected just a few weeks ago. In this scenario, understanding the state of fixed income is key to deciding what we want to invest in. But what is happening in the United States and European markets? And what is the most convenient fixed income option for investors?

Fixed income in the United States

In the United States, the Federal Reserve, the body chaired by Jerome Powell, decided to cut interest rates by 50 basis points at the last meeting on September 18. Since then, and despite the market discounting new rate cuts, the 10-year bond, a type of fixed income, has not stopped rising. How is this possible?

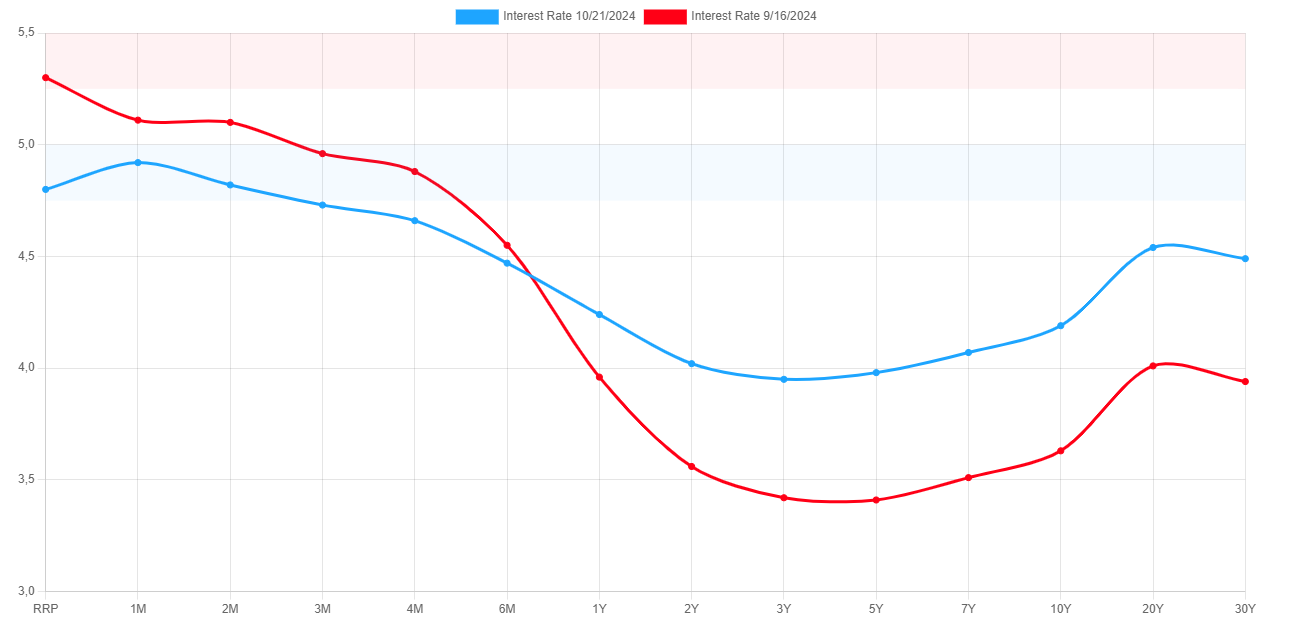

The red line is the yield on bonds before September 18 and the blue line is currently. Source: www.ustreasuryyieldcurve.com

As can be seen in the image, 1-month to 6-month US bonds offer a lower return than they did before the rate cuts. However, starting with the 1-year bond, the return is higher than it was before the cuts. This is because the short-term fixed-income tranches are much more dependent on monetary policy decisions than the longer-term tranches, which, however, depend on other factors.

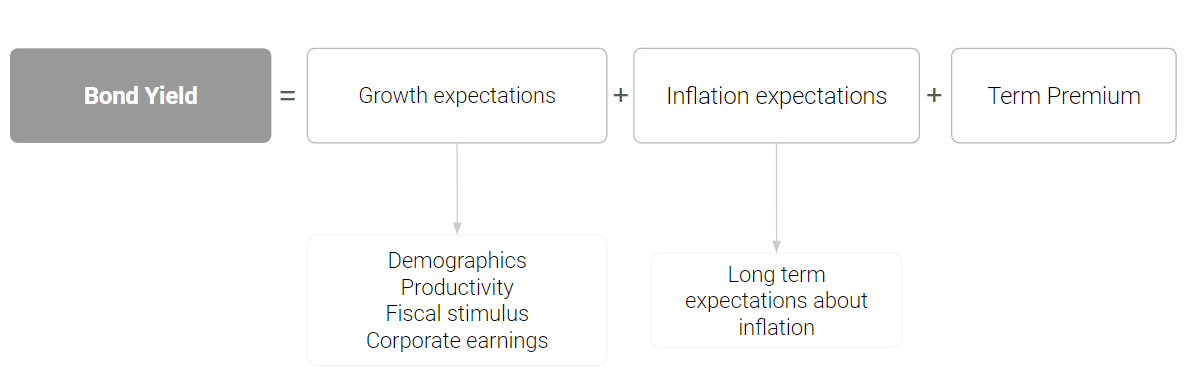

If we analyze the specific situation in the United States, we see that GDP growth is above 3%, the unemployment rate is again approaching its historical lows and that manufacturing and services are growing steadily. In addition, productivity is at its best and companies are reporting very positive corporate results.

Furthermore, inflation expectations at 5 and 10 years have broken analysts' forecasts in the latest reported data, offering a historic upward push. Given these circumstances, it is normal that fixed-income securities such as longer-term bonds are increasing in their profitability, consequently weighing down their price.

In this scenario, investors trust the markets, as demonstrated by asset allocation statistics, in which it can be seen that American investors trust the current opportunities offered by sectors such as technology, semiconductors, utilities or real estate.

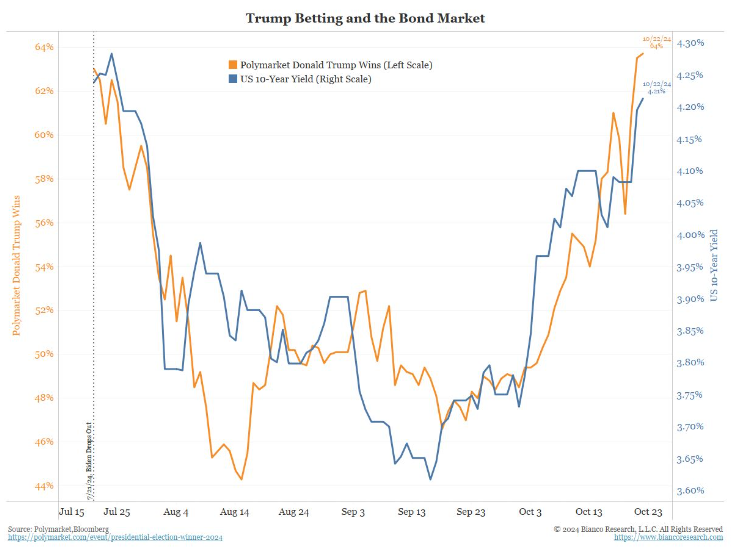

Other reasons that we are seeing with greater relation to the performance of bonds are the probability of Donald Trump's victory in the next presidential elections. The tax cuts, protectionist policies and proposed fiscal stimuli are driving up their profitability,

Fuente: James Bianco

Corporate bonds

Corporate bonds are fixed-income securities issued by companies to raise financing. These securities are characterized by offering a spread or premium on the yield higher than that offered by the country's bonds: since they have a higher risk, they must pay a higher return to compensate and attract investors. Despite the theory, these fixed-income securities are trading at the lowest of the last 25 years. In economic situations where we enter a recession or instability, these spreads rise, as was seen in 2000, 2008 or 2020, while in times of growth, or in times when a soft landing scenario is discounted, they fall.

In this scenario, marked by a complex geopolitical situation, high debt levels, global fragmentation and rising inflationary risks, we do not believe that it is worth investing in corporate bonds, since their profitability is only slightly higher than that offered by governments.

European Fixed Income

In this scenario, Europe is, without a doubt, the best opportunity we find in the fixed income market. While in the United States the macroeconomic data discount a strong growth in the country, in Europe we see a completely different situation.

This context is particularly marked by Germany, which could enter a technical recession this quarter. The manufacturing and services PMI data show a downward trend, and inflation is growing below the 2% target. Business results are leaving much to be desired and some of the most relevant indicators are showing data similar to 2008, such as employment. Demographics are declining and productivity growth is limited. Therefore, we believe that long-term European government bonds are facing a historic moment that investors can take advantage of.

In the case of the United States, the long-term tranches are not so dependent on rate cuts, but in Europe we have seen a greater correlation. While we believe that the fiscal impulse will not be as negative throughout the euro zone as it was this year, we expect it to continue to exert some drag on euro zone growth, mainly due to fiscal consolidation efforts in France, Italy and Germany. This means that the responsibility for stimulating growth falls almost entirely on the ECB's policy, which must be aggressive in its rate-cutting programmes.

How to invest in European fixed income?

CFDs

Within the XTB offer we can invest in CFDs that allow us to replicate the price of bonds. In this case we could also invest up or down.

If the profitability of bonds in Europe, as we have previously explained, evolves upwards, we could invest in the bund (German 10-year bond) waiting for a fall in the bond's yield that would drive its price up, while in the event that American treasuries gradually rise to levels higher than the current ones we could invest down in the TNOTE.

Source: Xstation

Stocks and ETFs

To invest in government fixed income and be able to generate an appreciation via price when bond yields fall, we believe that doing so with ETFs is more efficient than with any other product due to their liquidity and low cost, which will allow us to sell our position at any time in a simple way and without commissions.

Within the XTB offer we have a wide range of ETFs that will allow us to replicate the performance of European government fixed income. However, the Eurozone Government Bond ETF, under the acronym XGLE.DE, seems to us to be the best alternative of all, due to its low costs and characteristics given that it has a modified duration of slightly more than 7 years.

BREAKING: Eurozone recovery? Positive PMI data tempered by high oil and gas prices

Economic Calendar: Big Tech, Tensions Over Iran, and the ECB’s Decision ⏰

Daily Summary: Wall Street Stabilizes Despite Higher Oil Prices

Economic Calendar: Time for Tesla and Google Earnings (22.07.2026)

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.