The European aviation sector is under enormous pressure as a jet fuel supply crisis threatens to severely disrupt the summer travel season. The Strait of Hormuz, through which 25 to 35 percent of global jet fuel supplies flow, has remained largely closed since late February due to armed conflict in the Middle East. The International Energy Agency warned last week that Europe could run out of jet fuel inventories within just six weeks. President Trump's announcement of a ceasefire extension has so far brought no relief to the market, with the maritime transit corridor remaining unstable.

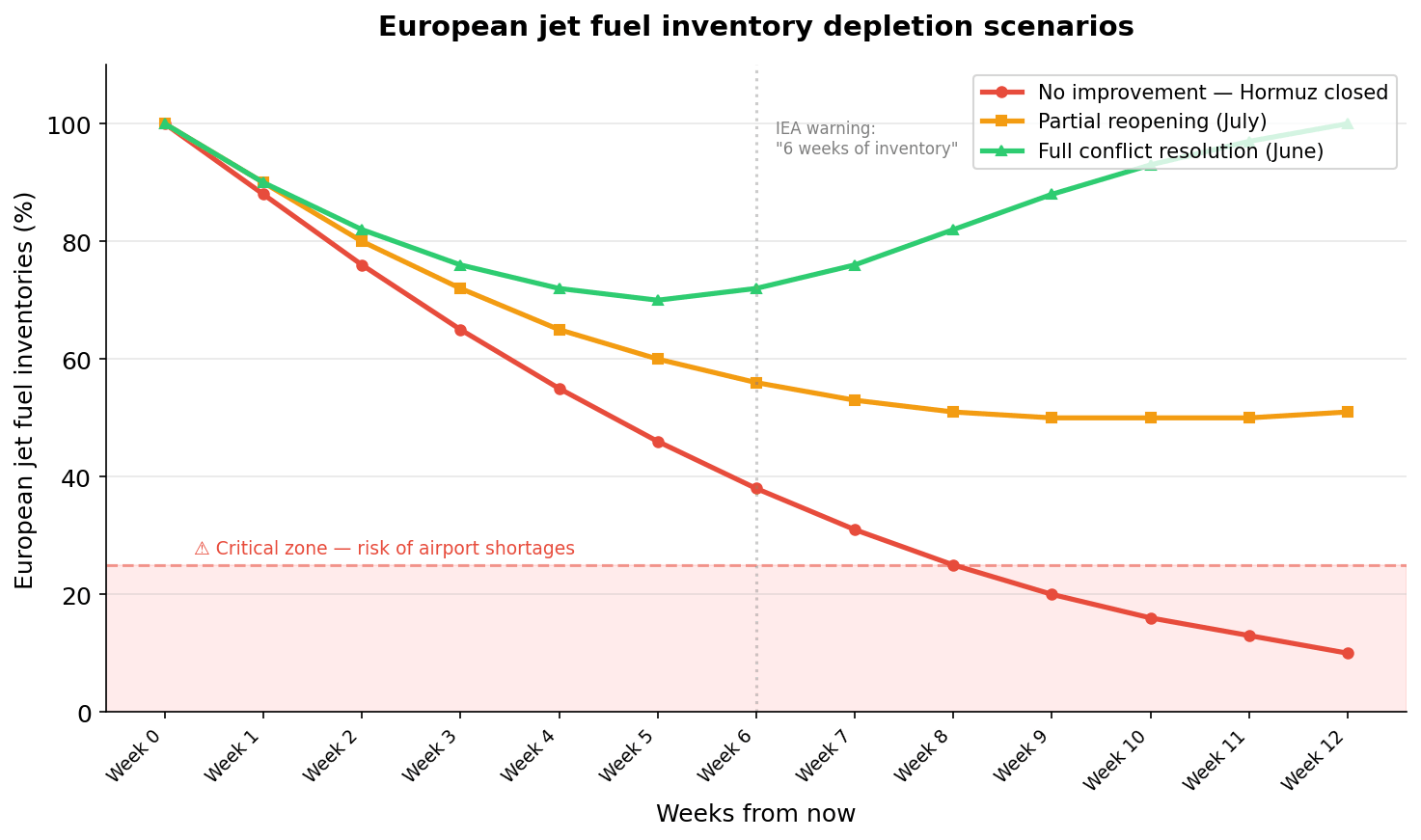

European jet fuel inventory depletion scenarios Three scenarios illustrate how quickly Europe could exhaust its jet fuel reserves depending on developments in the Strait of Hormuz. In the worst-case scenario, inventories drop to critical levels within 8–9 weeks. Source: CNBC, XTB based on Morningstar data

Hedging — partial protection, not full

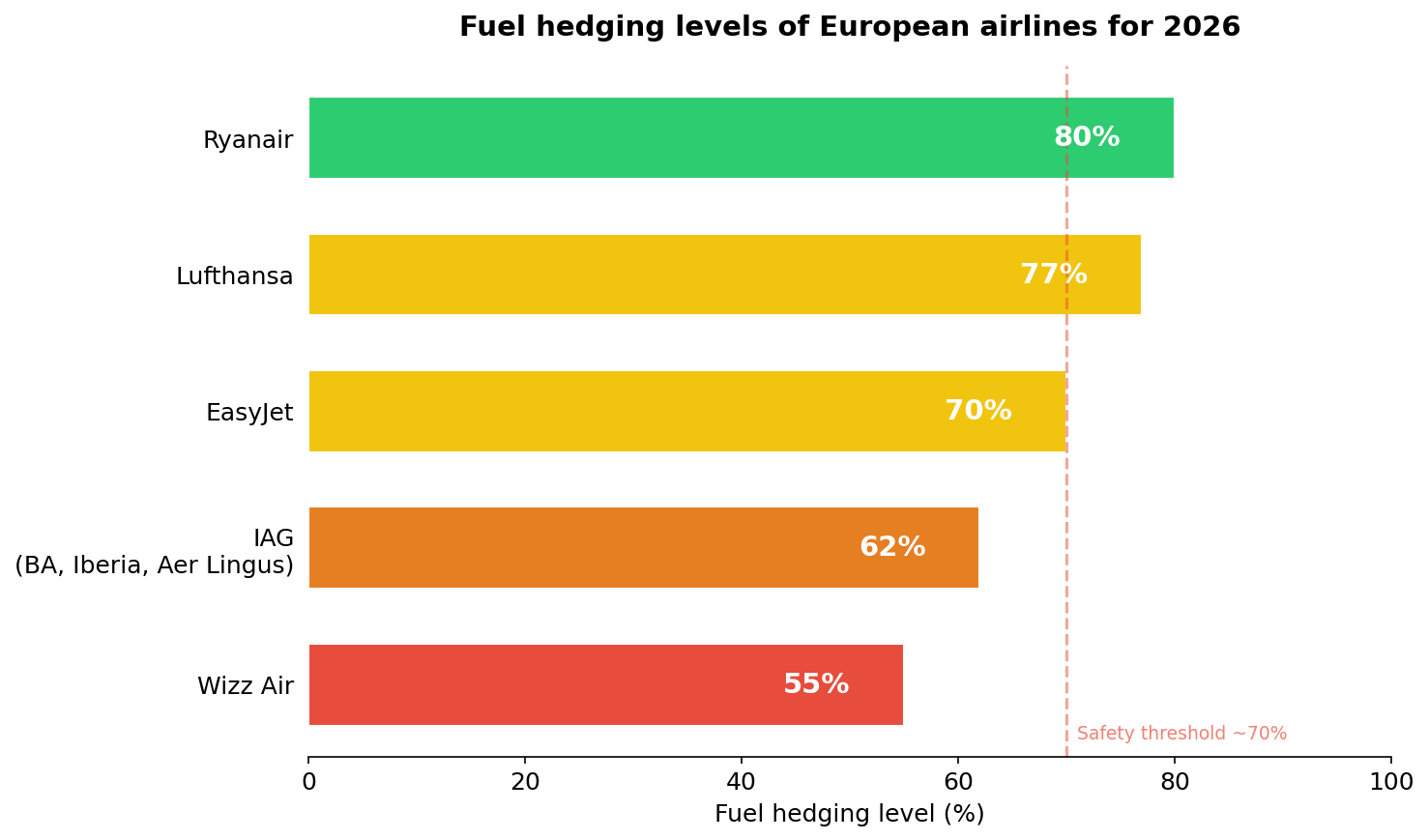

Wizz Air has been hit the hardest, as it is the least hedged among European carriers. Here is how fuel hedging levels for 2026 compare across airlines:

- 🟢 Ryanair — 80% (high buffer)

- 🟡 Lufthansa — 77%

- 🟡 EasyJet — ~70%

- 🟠 IAG (British Airways, Iberia, Aer Lingus) — 62%

- 🔴 Wizz Air — 55% (low buffer)

Fuel hedging levels of European airlines for 2026 The hedging gap across the sector is significant. Ryanair with 80% coverage has a much larger buffer than Wizz Air at 55%, which faces potential operational losses on unhedged flight as fuel prices double. Source: CNBC, XTB based on Morningstar data

These numbers can create a false sense of security. Hedging is a contract on price, not on physical availability of fuel. If kerosene simply runs out at European airports, price hedging becomes useless. Moreover, unlike strategic petroleum reserves, Europe does not maintain comparable reserves of jet fuel. Kerosene is a refined product, far more difficult to stockpile at scale.

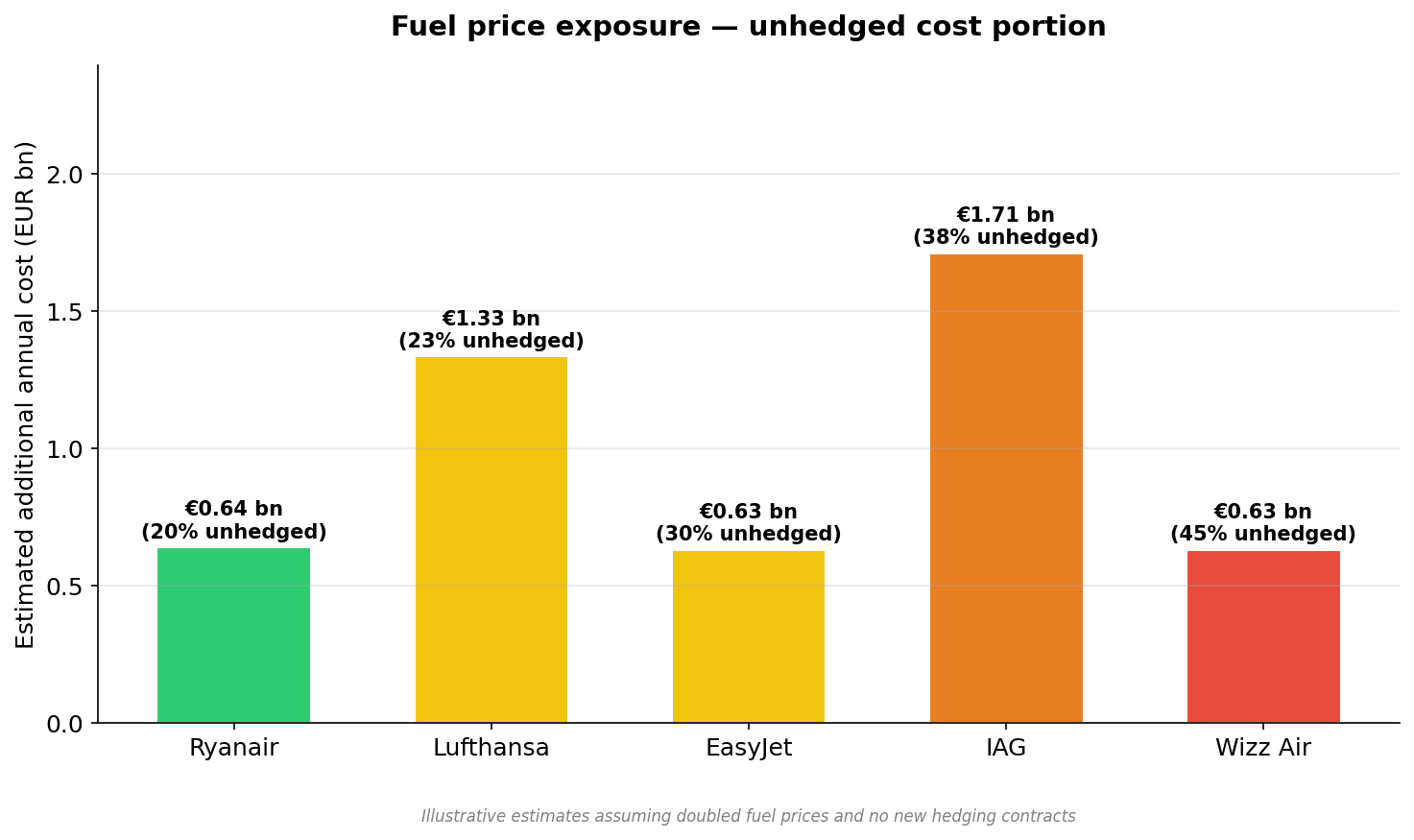

Fuel price exposure — unhedged cost portion Even with high hedging levels, the unhedged portion of fuel costs generates additional exposure measured in billions of euros annually. Lufthansa and IAG face the largest absolute exposure, while Wizz Air carries the highest proportional risk relative to its revenue base. Source: CNBC, XTB based on Morningstar data

Why jet fuel is rising faster than crude oil

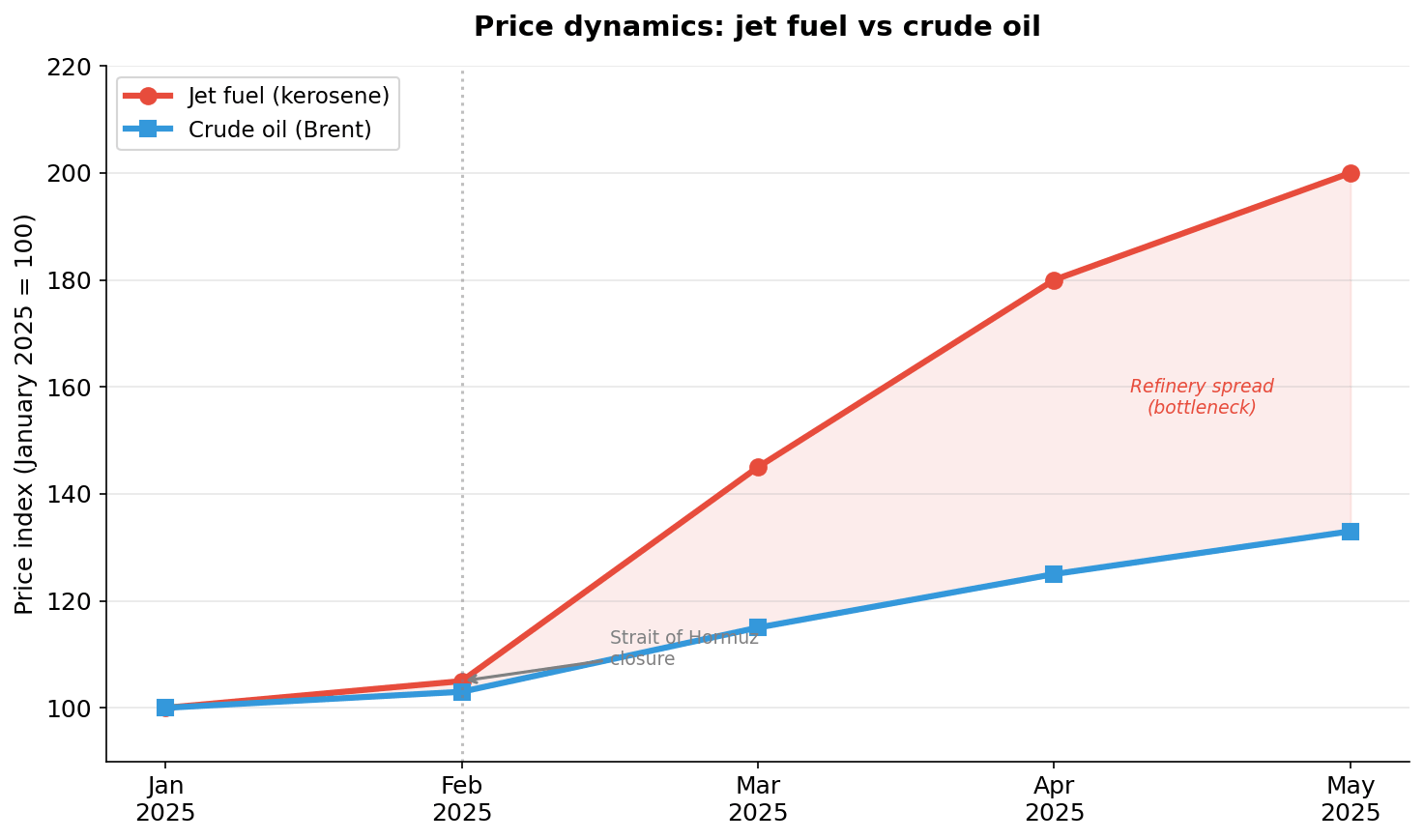

The key issue is not just fuel availability but also its price, which has doubled since the outbreak of the conflict, while crude oil has risen by only about one-third. This asymmetry is no coincidence — it points to a refinery bottleneck. Europe has closed or scaled back numerous refineries in recent years, partly as part of the energy transition. The crisis has exposed a deeper, structural weakness: the continent's growing dependence on imports of finished refined products, not just crude oil. This problem will not disappear once the Strait of Hormuz reopens.

Price dynamics: jet fuel vs crude oil The widening spread between kerosene and crude oil prices (red area) signals a structural refinery bottleneck in Europe. Even after crude prices stabilise, jet fuel may remain expensive for many months to come. Source: CNBC, XTB based on Morningstar data

Even well-hedged airlines are therefore only partially protected against this shock. Worse still, carriers are reluctant to enter new hedging contracts at such elevated prices — locking in at twice the normal rate freezes high costs for months. But if no one hedges, the entire sector remains exposed to the next shock. This is a classic coordination problem: individually rational, systemically dangerous. As a result, earnings volatility across European airlines in the coming quarters will be unprecedented.

Route cuts and a risky bet on the second half of the year

European carriers have already drastically reduced services for April and May, with Lufthansa, Air France-KLM and IAG also cutting transatlantic routes. Some airlines have shifted planned services from the second quarter to the third, banking on an improvement in the second half of the year.

This is effectively a bet on a swift resolution of the conflict. If the situation in Hormuz does not improve by July, carriers will find themselves in an even worse position — forced to serve pent-up demand with still-constrained supplies. The scenario of chaotic cancellations at the peak of summer season is very real.

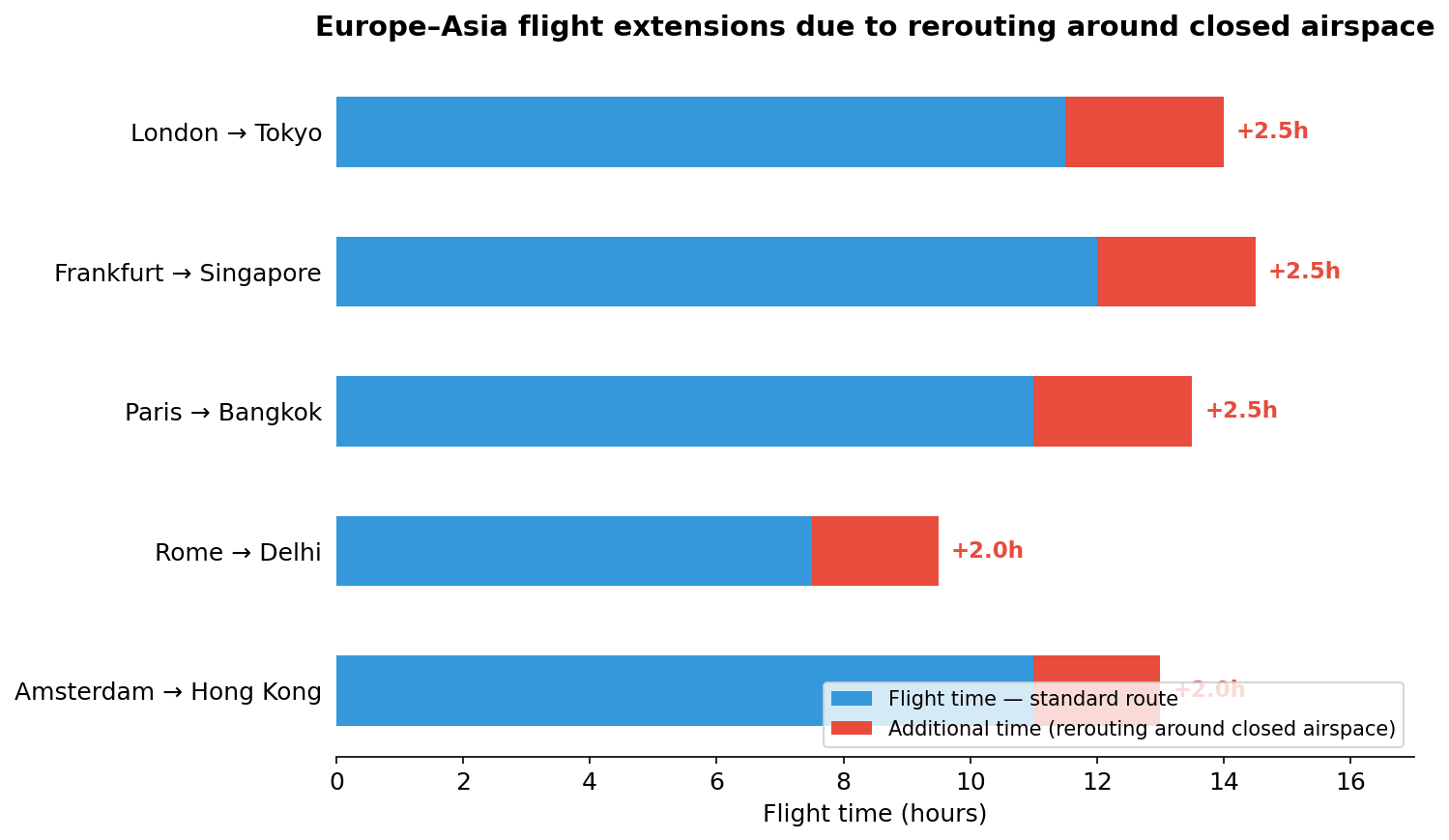

The domino effect on Europe–Asia routes

An additional challenge is the need to reroute around closed airspace, which adds one to three hours to Europe–Asia flights. This is not just more fuel per flight amid already constrained supplies — it triggers a cascade of consequences: fewer daily rotations per aircraft, crew duty-time regulation issues, and the need to maintain additional reserve crews. In practice, the effective capacity of the sector on affected routes drops by 10–15 percent, even when fuel is available. EasyJet has already warned investors that volatile fuel prices will weigh on results in the coming months and are negatively impacting customer bookings.

Europe–Asia flight extensions due to rerouting around closed airspace Rerouting around closed airspace adds 1.5 to 2.5 hours to key routes. Every additional hour means more fuel consumed, fewer daily rotations, and higher crew costs — the effect compounds across the entire network.Source: CNBC, XTB based on Morningstar data

Wizz Air as a canary in a coal mine

With a 55% hedging level for the fiscal year ending in March 2027—as confirmed by both Morningstar data and a direct statement from the company’s CEO, József Váradi—Wizz Air is in the most vulnerable position among European carriers in terms of protection against rising fuel prices. However, it is worth taking a closer look at the bigger picture.

As Váradi himself emphasized during the CAPA Airline Leader Summit — Airlines in Transition (April 23, 2026), Wizz Air has hedged 70% of its fuel needs for the next six months at a price of $700 per ton, while the current market price stands at $1,500 per ton. This means that in the short term, the company has a significant price buffer.

The company is focusing on preserving cash. Váradi stated clearly: “Airlines don’t go bankrupt because they’re unprofitable—they go bankrupt because they run out of cash. That’s why we’re focusing on maintaining liquidity. We’re starting with €2 billion.” A cash reserve of €2 billion in free cash gives Wizz Air room to maneuver that should not be underestimated.

The carrier is also taking active operational steps — Váradi announced that in fiscal year 2026, Wizz Air intends to focus its route network on “stable operating environments” in key markets in Central and Eastern Europe, and plans to suspend operations in the Middle East starting September 1, 2025. This is a pragmatic adaptation of the model to the realities of the crisis.

The ultra-low-cost model on which Wizz Air is based has for years allowed the airline to offer some of the lowest ticket prices in Europe, making air travel accessible to millions of passengers. The current situation, however, poses a particular challenge for the company—a model based on low margins is inherently more sensitive to sharp spikes in fuel costs than the models of traditional carriers, which have greater pricing flexibility.

Wizz Air’s situation may also serve as a barometer for the entire sector. As other carriers’ hedging contracts expire in the coming months, similar challenges may arise even for airlines that currently appear to be better protected. Wizz Air is the first to face this problem, but—as Váradi’s words show—it is doing so with a deliberate strategy to protect liquidity and ensure operational flexibility

What it means for passengers

For travellers planning summer holidays, the consequences go beyond ticket prices alone. Expect fuel surcharges introduced at short notice, a real risk of flight cancellations even close to departure, and a deterioration in service quality as airlines cut costs elsewhere to offset fuel expenses. Higher fares and a genuine risk of network reductions at the peak of summer season are now the base case, not the pessimistic scenario.

The key question for the coming weeks is whether the situation in the Strait of Hormuz stabilises before July. If it does not, European aviation faces its toughest summer since the pandemic — with the crucial difference that this time the problem is not a lack of demand, but the physical inability to serve it.

Mateusz Czyżkowski

Financial Markets Analyst

XTB HQ Poland

What July can tell us about where stocks go next

Market Wrap: European equities at 3-week highs! Apple dips in US premarket!

Morning Wrap: AI Fuels the Rebound. Technology Makes a Strong Comeback

Apple is still impressive, but the market is no longer impressed

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.