Lululemon Athletica (NASDAQ: LULU) shares fell around 12% after the company released its fiscal first-quarter 2026 results. While revenue and earnings per share came in broadly in line with market expectations, investors were concerned by the retailer’s lowered full-year guidance and further signs of weakening demand in North America.

The market is increasingly questioning whether the company’s challenges — particularly its struggle to reignite growth in the U.S. market — are temporary in nature or reflect a deeper deterioration in the positioning of one of the world’s most recognizable premium athletic apparel brands. The stock has fallen to its lowest level since May 2018, and its weakness is weighing on sentiment across the broader athletic apparel sector, including rival Nike, whose shares are trading near their lowest levels in 15 years.

Key Takeaways

-

Revenue increased 4% year-over-year to $2.47 billion

-

Net income fell from $314.5 million to $195 million (-38% YoY)

-

EPS declined from $2.60 to $1.69

-

Gross margin contracted by 410 basis points to 54.2%

-

Operating margin declined by 730 basis points to 11.2%

-

Comparable sales increased 1%

-

Comparable sales in the Americas fell 5%

-

International comparable sales rose 13%

-

Revenue in Mainland China increased 30%

-

The company lowered its FY2026 EPS guidance to $10.95–$11.15 from $12.10–$12.30

-

Revenue guidance was cut to $11.0–$11.15 billion from $11.35–$11.50 billion

Results Met Expectations, but Profitability Continues to Deteriorate

From a top-line perspective, Lululemon delivered results that were broadly in line with Wall Street expectations. The company generated $2.47 billion in revenue versus analyst estimates of $2.44 billion, while earnings per share came in exactly at the consensus forecast of $1.69.

However, the underlying earnings picture was considerably weaker. Operating income declined 37% year-over-year, while net income dropped 38%. At the same time, gross margin narrowed to 54.2%, highlighting rising cost pressures and weakening pricing power.

This trend is particularly important for investors because Lululemon has historically commanded a premium valuation thanks to its ability to maintain industry-leading margins and strong brand equity.

China Remains a Growth Engine, but North America Continues to Weigh on Performance

The strongest aspect of the quarter remained the company’s international business. Revenue outside North America increased 22%, while international comparable sales rose 13%.

China stood out as the key growth driver. Revenue in Mainland China climbed 30%, while comparable sales advanced 20%, reinforcing the market’s importance within Lululemon’s long-term growth strategy.

In contrast, North America remains under pressure. Revenue in the region declined 3%, while comparable sales fell 5%. This segment continues to be the primary source of concern for investors and analysts alike.

Lowered Guidance Triggered the Sharp Sell-Off

The biggest disappointment came from management’s outlook for the coming quarters.

For the second quarter, Lululemon expects revenue between $2.45 billion and $2.47 billion and EPS of $1.76–$1.81, both below Wall Street expectations.

More importantly, the company significantly reduced its full-year guidance. Management now expects fiscal 2026 EPS of $10.95–$11.15, nearly 10% below its previous forecast.

The guidance cut suggests a more challenging consumer environment and a slower recovery trajectory than management had anticipated only a few months ago.

According to the company, macroeconomic uncertainty and cautious discretionary spending continue to pressure demand across key markets.

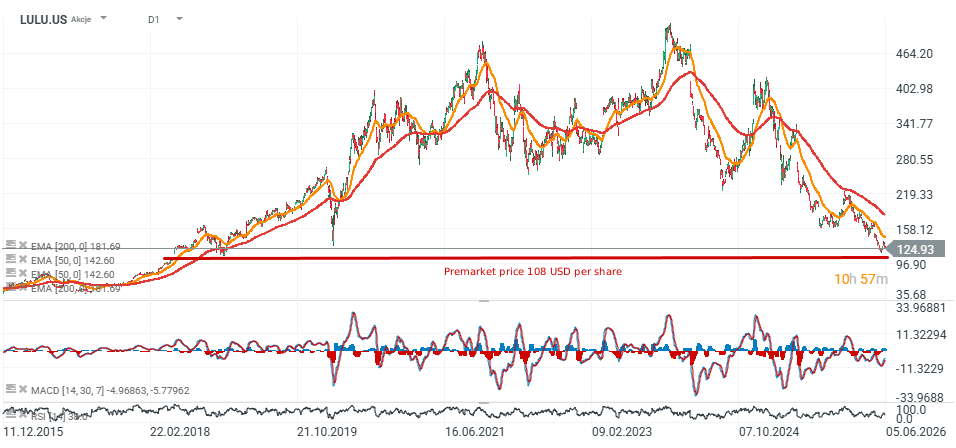

Analysts Cut Price Targets as the Chart Signals Persistent Weakness

Following the earnings release, several major brokerages lowered their price targets on Lululemon shares. Stifel reduced its target price from $176 to $134 while maintaining a Hold rating. The firm noted that the company’s core North American business deteriorated further during April and May and now expects comparable sales to remain negative through the first half of fiscal 2027.

Other analysts have expressed similar concerns. Wells Fargo cut its target price to $110, Jefferies lowered its target to $115, and BofA Securities reduced its valuation to $140.

The common theme across these revisions is weakening North American demand, ongoing margin pressure, and concerns about market share erosion. Some analysts are also beginning to question whether the company is facing a broader brand issue rather than merely a temporary product-cycle challenge.

From a technical perspective, the stock’s decline to eight-year lows reinforces the negative narrative surrounding the name. The breakdown reflects not only weaker earnings expectations but also growing uncertainty regarding the sustainability of Lululemon’s premium positioning.

Despite these challenges, the company continues to post strong international growth and has expanded its global store base to 816 locations. In addition, former Nike executive Heidi O’Neill is set to take over as CEO in the coming months, a leadership change that investors hope will help restore growth momentum. The next several quarters will likely determine whether Lululemon is experiencing a temporary operational slowdown or facing a more structural challenge to its brand and long-term growth story.

Source: xStation5

Morning Wrap: Equities under pressure after Wall Street took profits, FX frozen (06.08.2026)

Daily Summary: Dow Jones hits record highs, while gold and silver rally on hopes for a US–Iran deal

Gold surges higher, as US stock rally slows down

US Open: AMD and SpaceX failed to impress, but the broader market remains resilient

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.