European equity markets opened Wednesday’s session with modest gains, extending the recent improvement in sentiment following the easing of geopolitical tensions surrounding Iran. However, the advance remains measured as investors increasingly shift their attention toward the Federal Reserve’s policy decision and the first communication from newly appointed Fed Chair Kevin Warsh.

According to Hugh Gimber, Global Market Strategist at JPMorgan Asset Management, European equities may offer selective opportunities following the recent decline in oil prices. In his view, consumer-facing companies and energy-sensitive cyclical sectors appear particularly attractive. Gimber noted that the interim peace agreement between the United States and Iran, which is expected to be signed on Friday, has helped cool energy prices and created opportunities beyond the largest constituents of major equity indices. Oil prices are edging slightly higher today, gaining around 0.1% and remaining above $80 per barrel. Meanwhile, the US dollar is posting modest gains, while Bitcoin has slipped back below $65,000 after failing to break sustainably above the $68,000 level.

Key market drivers today include:

-

Lower inflationary pressure across the Eurozone

-

Improving sentiment toward European consumer and cyclical stocks

-

Anticipation ahead of the Federal Reserve decision

-

Weakness in Germany’s automotive sector weighing on the DAX

-

Pressure on the UK’s FTSE 100 from energy stocks

European indices remain near record highs

The pan-European STOXX 600 index was up around 0.4%, remaining close to all-time highs. Over the previous four sessions, the benchmark gained approximately 3% as investors embraced risk assets amid fading concerns about an energy-driven inflation shock.

Major European markets traded mostly higher. France’s CAC 40 rose around 0.2%, Italy’s FTSE MIB remained modestly positive, and Spain’s IBEX 35 gained roughly 0.5%.

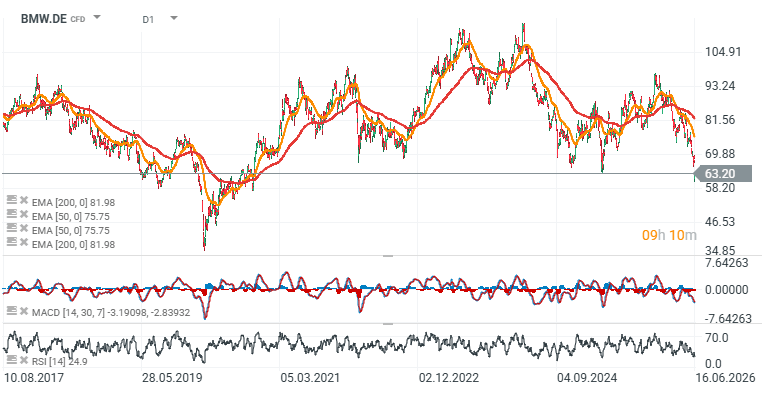

Germany’s DAX underperformed, continuing to feel the impact of a sharp sell-off in automotive stocks following BMW’s decision to lower its annual profit outlook.

Shares of the Bavarian automaker fell more than 7%, dragging down peers including Volkswagen and Mercedes-Benz. The market reaction highlights investors’ sensitivity to any signs of weakening margins and slowing demand in cyclical industries.

The automotive sector remains exposed to several challenges simultaneously, including the high costs of technological transformation, increasing competitive pressure, and fluctuating consumer demand. As a result, a single earnings revision from a major manufacturer can quickly trigger broader weakness across the industry.

Eurozone inflation offers relief to investors

Broader market sentiment was supported by inflation data from the Eurozone. May CPI figures pointed to a moderation in price pressures on a month-over-month basis, easing concerns that earlier increases in energy prices could force the European Central Bank into a more hawkish stance.

Short-dated Eurozone government bond yields continued to decline, reflecting reduced expectations for tighter monetary policy. For equity markets, this is generally supportive, as lower interest rate expectations tend to improve valuations for risk assets.

Oil prices ease following developments involving Iran

The oil market remains a key piece of the puzzle. Crude prices have retreated in recent sessions after reports that Washington is preparing to formally waive certain sanctions on Iranian oil exports.

Such a development reduces the geopolitical premium embedded in energy prices and lowers the risk of another inflationary shock in Europe. This is particularly important for a region that remains sensitive to energy costs and their impact on both consumers and businesses.

FTSE 100 lags behind continental peers

Not all European markets have benefited equally from the current backdrop. The UK’s FTSE 100 has remained under pressure due to its heavy weighting toward energy companies.

Lower oil prices weighed on shares of BP and Shell, limiting the index’s upside potential. Investors also digested the latest UK inflation data, which showed annual CPI unchanged at 2.8%. The figures will serve as an important reference point ahead of the Bank of England’s upcoming interest rate decision.

Individual stocks outperform despite cautious sentiment

At the company level, Straumann and Auto1 stood out among the strongest performers.

Straumann shares surged around 9% after the company upgraded its full-year profitability outlook. Auto1 gained more than 8% following the release of robust long-term financial guidance.

These moves suggest investors remain willing to reward companies that demonstrate improving earnings visibility and resilient business fundamentals despite a still uncertain macroeconomic environment.

The Fed remains the key event of the week

In the near term, the Federal Reserve remains the dominant market catalyst. While interest rates are widely expected to remain unchanged, investors will closely monitor the tone of the accompanying statement and Kevin Warsh’s first press conference as Fed Chair.

The Fed’s communication will be important not only for Wall Street but also for European risk assets, given its influence on global liquidity conditions, the US dollar, and equity valuations worldwide.

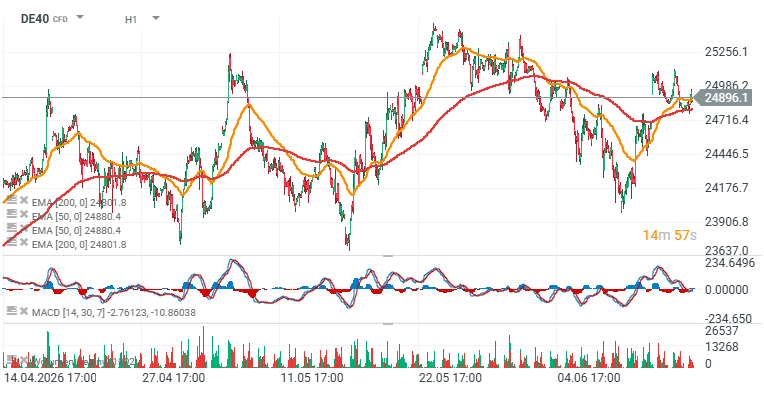

The market remains constructive but fragile: DE40 and EU50 charts (D1)

The broader backdrop for European equities remains constructive, though more nuanced than headline index levels might suggest. Markets continue to benefit from lower oil prices, easing inflation pressures, and a reduction in geopolitical risks.

At the same time, valuations remain close to record highs, meaning the next leg of the market move could depend heavily on whether central banks validate expectations for a more accommodative policy path. In such an environment, investors are likely to become increasingly selective, focusing on earnings quality, margin resilience, and the credibility of corporate guidance.

Source: xStation5

Source: xStation5

Three Markets to Watch Next Week (July 31, 2026)

What July can tell us about where stocks go next

Market Wrap: European equities at 3-week highs! Apple dips in US premarket!

Euro Area core inflation above estiamtes! EURUSD under key resistance!

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.