The memory manufacturer released its long-awaited results and, despite high expectations, managed to beat them very clearly. The stock is up more than 10% in the post-earnings session.

Financial data

- The pace and scale of growth have taken analysts’ and investors’ breath away.

- The company raised its quarterly revenue from USD 25 billion to over USD 41 billion, which represents 170% growth - quarter-on-quarter, not year-on-year.

- EPS increased from USD 12 to over USD 25, which is a 200% rise.

- Gross margin remains above 80% in nearly all segments of the company; only the automotive segment posts 79%.

- Growth across all business segments is around 100%, with the fastest growth in the data center segment, followed by memory.

- After investments of USD 7.1 billion, free cash flow stands at USD 18.3 billion.

Guidance

- The company announced an even better Q3, with guidance above expectations.

- Projected revenue next quarter is expected to rise to USD 50 billion, with margins around 86% and EPS of USD 31.

Market reaction

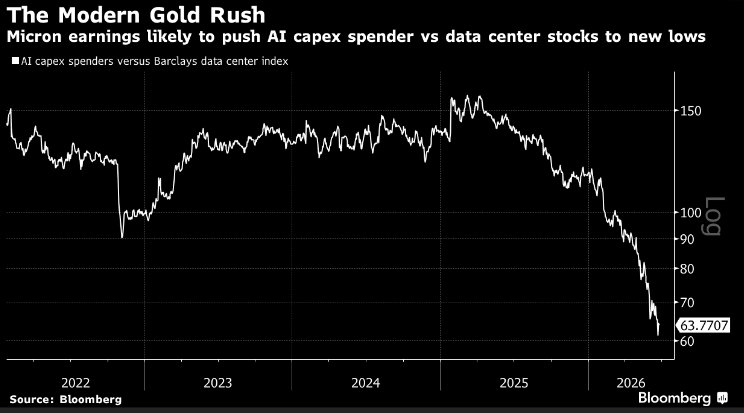

- Contrary to what many investors expected, Micron’s strong results turned out to be pressure on the tech sector - not support.

Souce: Bloomberg Finance

- Micron’s huge profits and optimistic forecasts mean capital expenditure remains stable, but they also imply an increasingly heavy burden on the budgets of companies that already have to take on record amounts of debt.

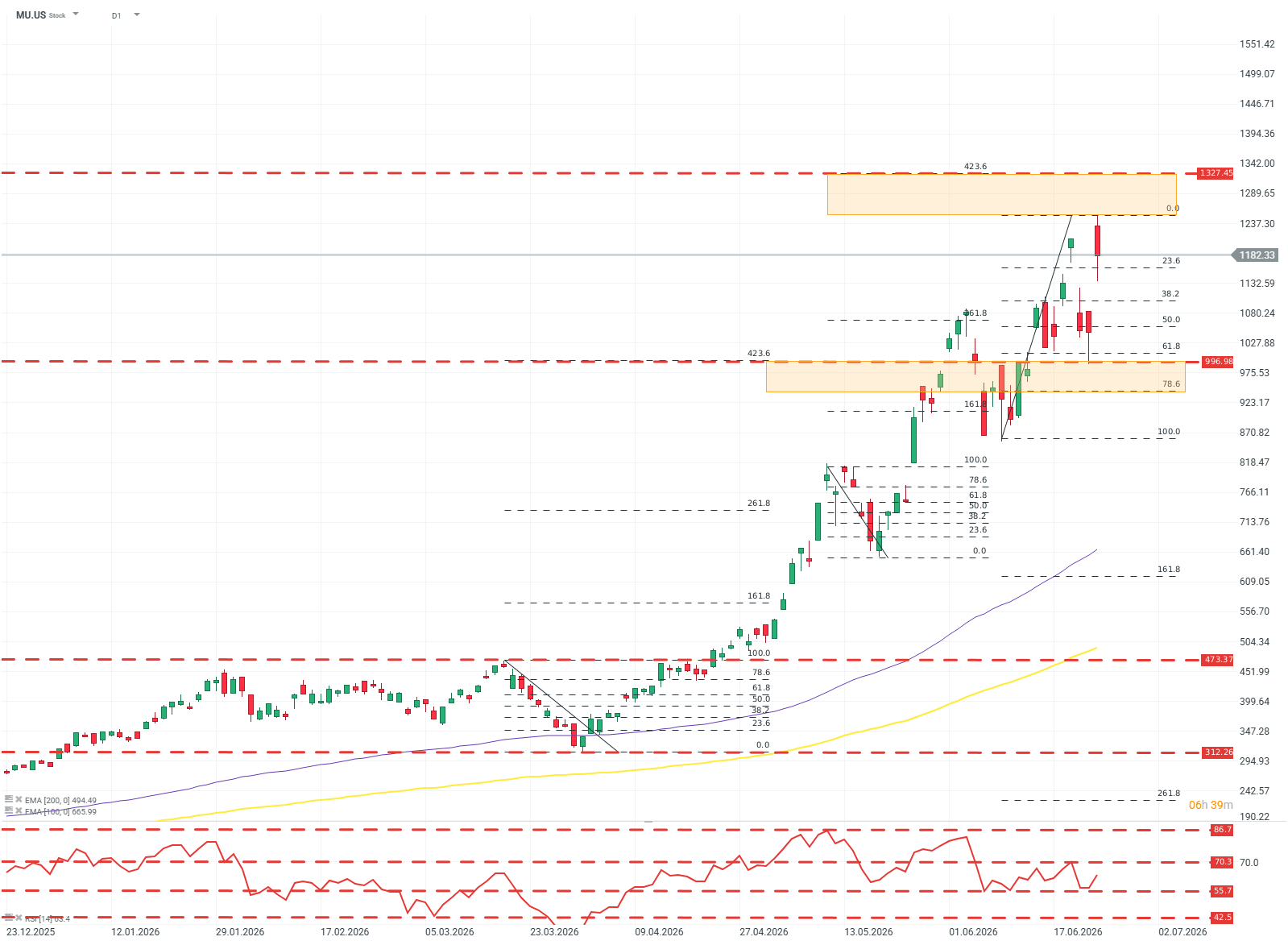

MU.US (D1)

The company’s uptrend is very sharp and steep, but Fibonacci levels help identify potential resistance and support zones. If, for some reason, supply were to take the инициативive, strong resistance would most likely be the (also psychological) level of USD 1000. For buyers, the next target is a wide resistance zone around USD 1300.

Not everything that glitters is gold

While the pace and scale of the company’s growth are unmatched and phenomenal, no company is free of risk and weaknesses - and that is also the case for Micron (and other memory companies).

At present, the company is benefiting from unprecedented investments by the tech sector in data centers. Revenue growth is enormous, but it is driven by a sudden and concentrated jump in demand, not by innovation on the companies’ side.

Companies involved in the specialized, previously niche business of producing DRAM and NAND memory are cyclical - not without reason. In cycles of strong economic conditions and periods of (smaller or larger) speculative bubbles in the tech sector, demand for memory rises drastically and rapidly. The current increases mean that: we are observing another period of costly and wide-ranging investments — which may not pay off - on a scale greater than ever before… or a paradigm shift is taking place, and AI-driven demand is the new “base” and starting point for the company’s revenues. Both scenarios are difficult and risky to value.

Valuation difficulty is compounded by the fact that memory producers do not differ much in their offerings - creating a dangerous combination of concentrated demand and fairly strong competition, even though the production process itself is quite specialized.

In the past, this has repeatedly led to the formation of cartels and price-fixing among RAM manufacturers. The U.S. Department of Justice proved anti-consumer behavior and price collusion by RAM producers during the Dot-com bubble (1998–2002); Micron was one of them.

Such behavior in the current market would be extremely risky, not because of legal or regulatory consequences, but because the CAPEX budgets required to purchase memory alone are already hard to imagine. SemiAnalysis and CLSA estimate that out of the hundreds of billions in CAPEX by tech companies, currently about 30–40% is spending on memory alone — and that share is expected to grow.

Companies like Micron are fully dependent on that spending, and if they themselves start standing in the way of the “AI revolution,” they could stop it - and lose their position as quickly as they gained it.

Outlook going forward

A “wild card” for the sector in the coming quarters is China. Chinese memory manufacturers, thanks to deep integration with a centrally planned economy and direct access to financial support, can very quickly “dump” enough memory on the market to push sector margins down - even if revenues continue to grow.

Regardless of whether valuations and profits of memory companies, including Micron, are “rational,” the fact is that the gigantic investment budgets of hyperscale companies are not going anywhere in the near term, and that, in a simple mechanical way, means these companies should continue to wow the market with great results.

Is there a chance that these companies will break out of the cyclical nature of their business? Partly. Even if the AI industry eventually disappoints investors and some investments become worthless, one should not expect hundreds of massive data centers to disappear overnight. They will require maintenance and modernization.

Kamil Szczepański

Financial Markets Analyst, XTB

Daily Summary: Nasdaq 100 Up 3.2% – Is the Bull Market Back? (04.08.2026)

Palantir Earnings: High Expectations and Even Bigger Gains

Daily Summary - The market starts to doubt rate hikes after Warsh, but Trump destroys the rebound

US OPEN: Wall Street Holds Its Breath Ahead of Fed Decision and Tech Giant Earnings

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.