- Brent crude prices have fallen to around $70 per barrel, successfully erasing the geopolitical risk premium that arose following U.S.-Iran tensions earlier this year.

- Declining prices are driven by strong supply from non-OPEC+ producers—notably the U.S.—combined with stagnating global demand, especially from China.

- The current market stability is fragile, as strategic energy reserves are at historic lows and the ongoing de-escalation agreement is only temporary, creating potential for volatility in the second half of 2026.

- Brent crude prices have fallen to around $70 per barrel, successfully erasing the geopolitical risk premium that arose following U.S.-Iran tensions earlier this year.

- Declining prices are driven by strong supply from non-OPEC+ producers—notably the U.S.—combined with stagnating global demand, especially from China.

- The current market stability is fragile, as strategic energy reserves are at historic lows and the ongoing de-escalation agreement is only temporary, creating potential for volatility in the second half of 2026.

Geopolitical Decompression and Return to Pre-War Equilibrium Levels

The sharp sell-off in oil futures at the turn of the second and third quarters of 2026 has led to the elimination of the full war premium that arose immediately after the start of U.S. attacks on Iran at the end of February. Of course, oil prices remain at an elevated level compared to the beginning of the year, when concerns about a possible conflict began to emerge, particularly after the brief U.S. attack on Venezuela.

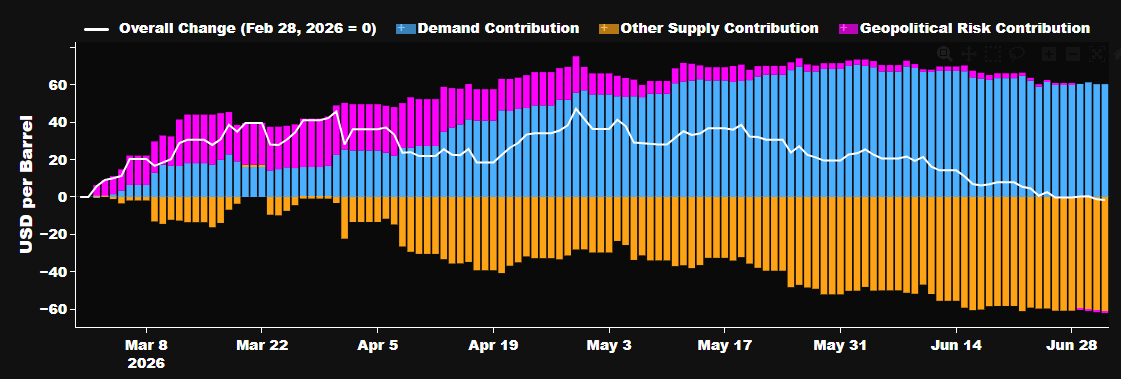

Looking from the beginning of February, essentially the full geopolitical premium has been erased in the oil market. Source: Bloomberg Finance LP

Looking from the beginning of February, essentially the full geopolitical premium has been erased in the oil market. Source: Bloomberg Finance LP

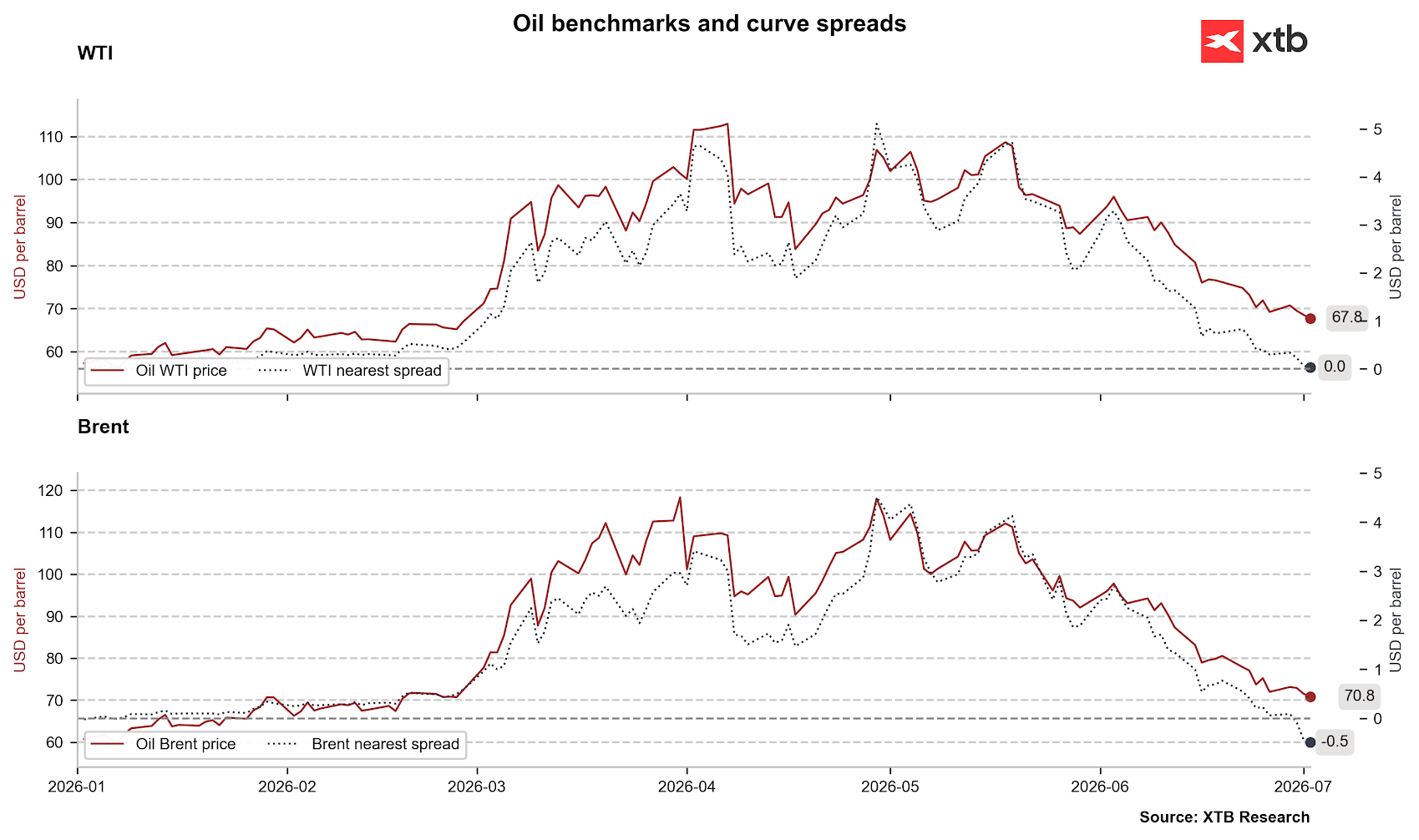

The Brent oil price is currently testing the level of 70 dollars per barrel and is at levels below the close of the last Friday of February, just before the U.S. attack on Iran. Of course, it is worth remembering that over these few months we observed rollovers of futures contracts in extreme backwardation. This means that the spectacular nominal decline is not as large if we look at it through a real prism.

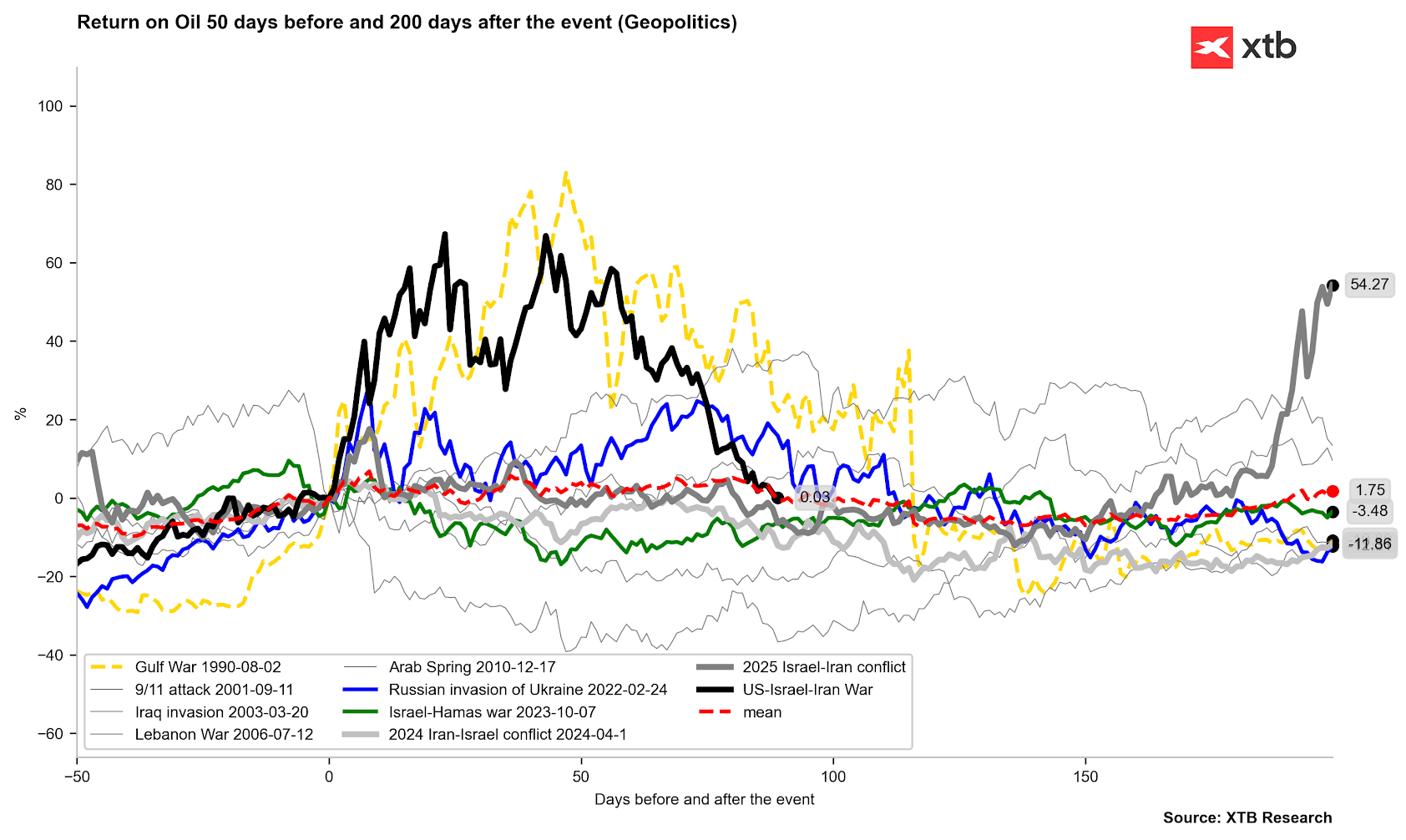

Brent oil fully erases the war premium from the last few months. Importantly, this premium was removed faster than in 2022 or 1990. As the behavior of oil prices from those periods shows, we should expect continued volatility, but at the same time a downward direction. Source: Bloomberg Finance LP, XTB

Brent oil fully erases the war premium from the last few months. Importantly, this premium was removed faster than in 2022 or 1990. As the behavior of oil prices from those periods shows, we should expect continued volatility, but at the same time a downward direction. Source: Bloomberg Finance LP, XTB

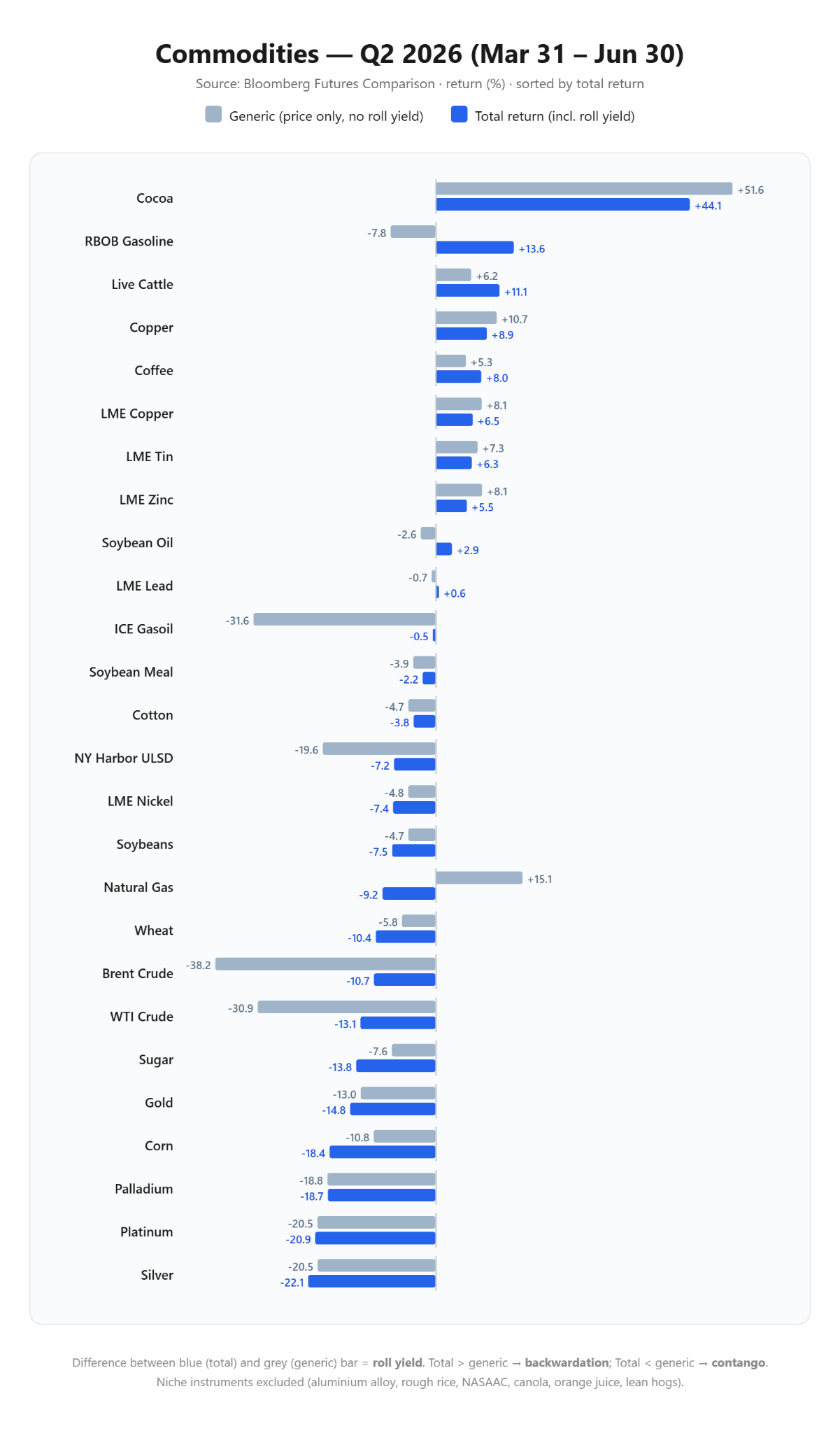

Looking at the summary of commodity price behavior in the second quarter, we see that taking into account futures rollovers, the declines were significantly smaller than would follow from the nominal price behavior. This is a normal situation, considering the shape of backwardation. Source: Bloomberg Finance LP, XTB

Looking at the summary of commodity price behavior in the second quarter, we see that taking into account futures rollovers, the declines were significantly smaller than would follow from the nominal price behavior. This is a normal situation, considering the shape of backwardation. Source: Bloomberg Finance LP, XTB

Of course, it should be emphasized that the direct catalyst for market relaxation was the signing on June 17, 2026, of a temporary, 60-day memorandum of understanding (MOU) between Washington and Tehran. This agreement opened the way for de-escalation and enabled the rapid reconstruction of logistical flows in the Strait of Hormuz. The volume of sea transport through this key bottleneck of global energy reached a record level of 78 units per day at the end of June (unofficially). However, it is worth remembering that for now the memorandum is temporary, and JD Vance himself suggested that the current time is primarily intended for replenishing stocks, and further de-escalation will depend on progress in negotiations.

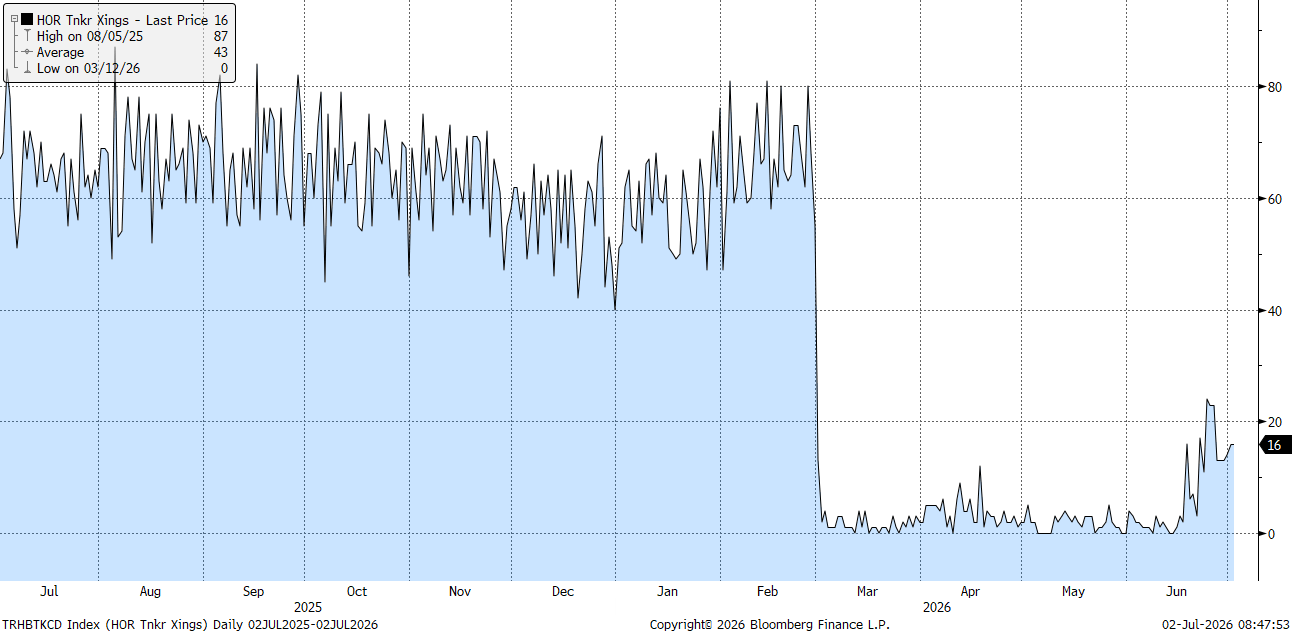

The number of tankers officially passing through the Strait of Hormuz is far from the declared numbers, but many units may still decide to pass through without officially switched-on transponders. Source: Bloomberg Finance LP

The number of tankers officially passing through the Strait of Hormuz is far from the declared numbers, but many units may still decide to pass through without officially switched-on transponders. Source: Bloomberg Finance LP

Fundamental Asymmetry: Record Production and Demand Stagnation

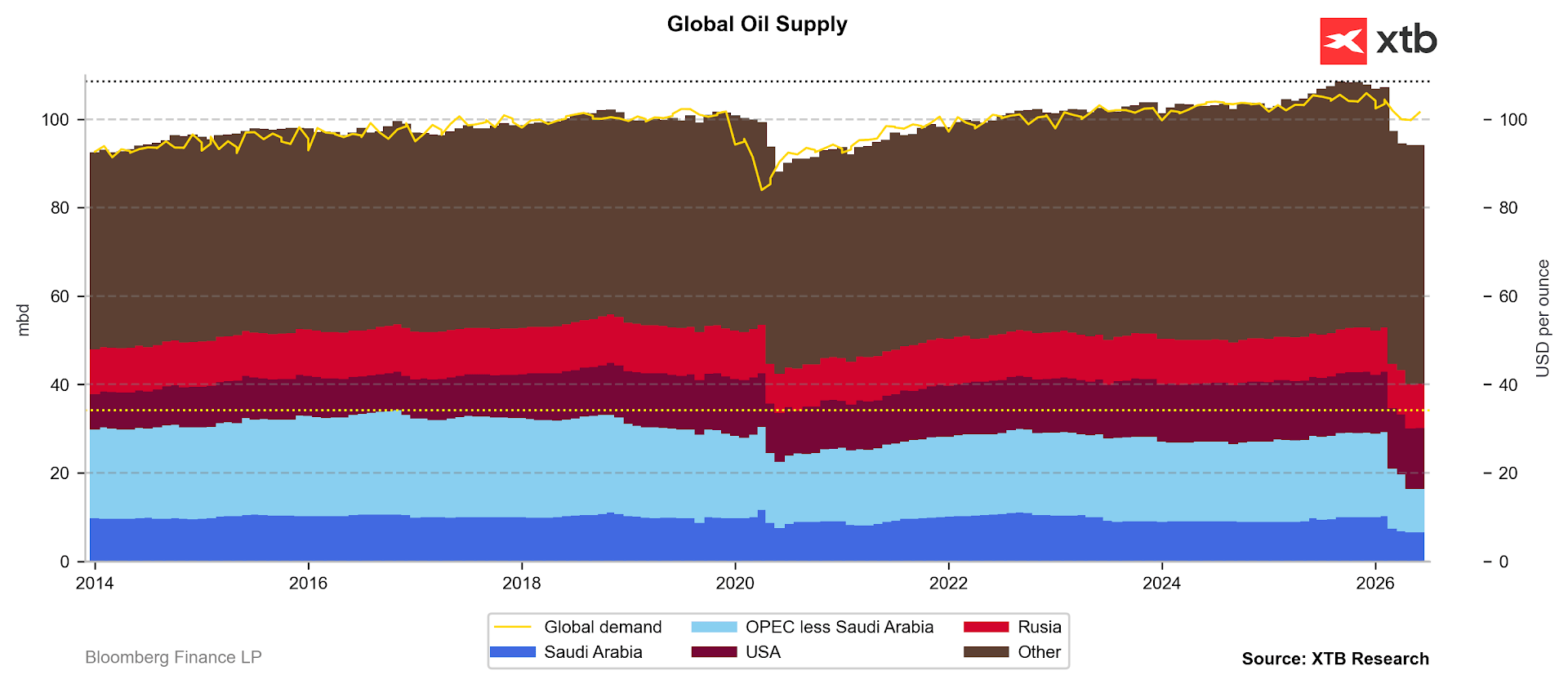

As the war premium falls, market participants' attention has returned to a rigorous analysis of physical fundamentals, which indicate a deep and growing structural asymmetry. On the supply side, the pressure for price declines is compounded by the unprecedented flexibility and extraction volume of producers outside the OPEC+ cartel, led by the United States, where production is approaching another milestone at 14 million barrels per day. At the same time, OPEC+ continues the process of gradually restoring production capacity, approving another increase in production quotas by approximately 188,000 barrels per day for August, which raises (on paper for now) the group's cumulative supply increase since April to nearly 600,000 barrels per day. In June, however, we have a minimal increase in global supply, along with an acceleration of exports from some Persian Gulf nations.

Although we still have a deficit in the market, in July we should already see a stronger increase in supply. This largely depends on flexible producers like Saudi Arabia or the United Arab Emirates. Source: Bloomberg Finance LP

Although we still have a deficit in the market, in July we should already see a stronger increase in supply. This largely depends on flexible producers like Saudi Arabia or the United Arab Emirates. Source: Bloomberg Finance LP

Demand in June moved slightly upward, but the prospect of a recovery this year remains doubtful, mainly due to the slowdown in macroeconomic activity in China. The International Energy Agency (IEA) made a drastic revision of its forecasts, lowering global demand growth estimates for 2026 by 700,000 barrels per day and forecasting an absolute decrease of 1.1 million barrels per day for the entire year.

Structural Risks Hidden Under the Bearish Consensus

Although the market consensus has become extremely bearish, a deeper analysis of the inventory structure and political conditions suggests that the complete erasure of the geopolitical premium may rest on fragile premises. Firstly, the legal framework and sovereignty over the Strait of Hormuz remain a key point of contention in future conflicts. Iranian negotiator Mohammad Bagher Ghalibaf clearly stated that Tehran and Muscat maintain full jurisdiction over this waterway, and the current 60-day memorandum in no way limits Iran's sovereign rights to control navigation after its expiration. Incidental attacks on commercial vessels that took place at the end of June show how easily a fragile truce can be broken.

The forward structure no longer shows any tension on the immediate calendar spreads. At the same time, such a situation may appear to be short-term, given the depletion of inventories and still a lot of uncertainty. Source: Bloomberg Finance LP, XTB

The forward structure no longer shows any tension on the immediate calendar spreads. At the same time, such a situation may appear to be short-term, given the depletion of inventories and still a lot of uncertainty. Source: Bloomberg Finance LP, XTB

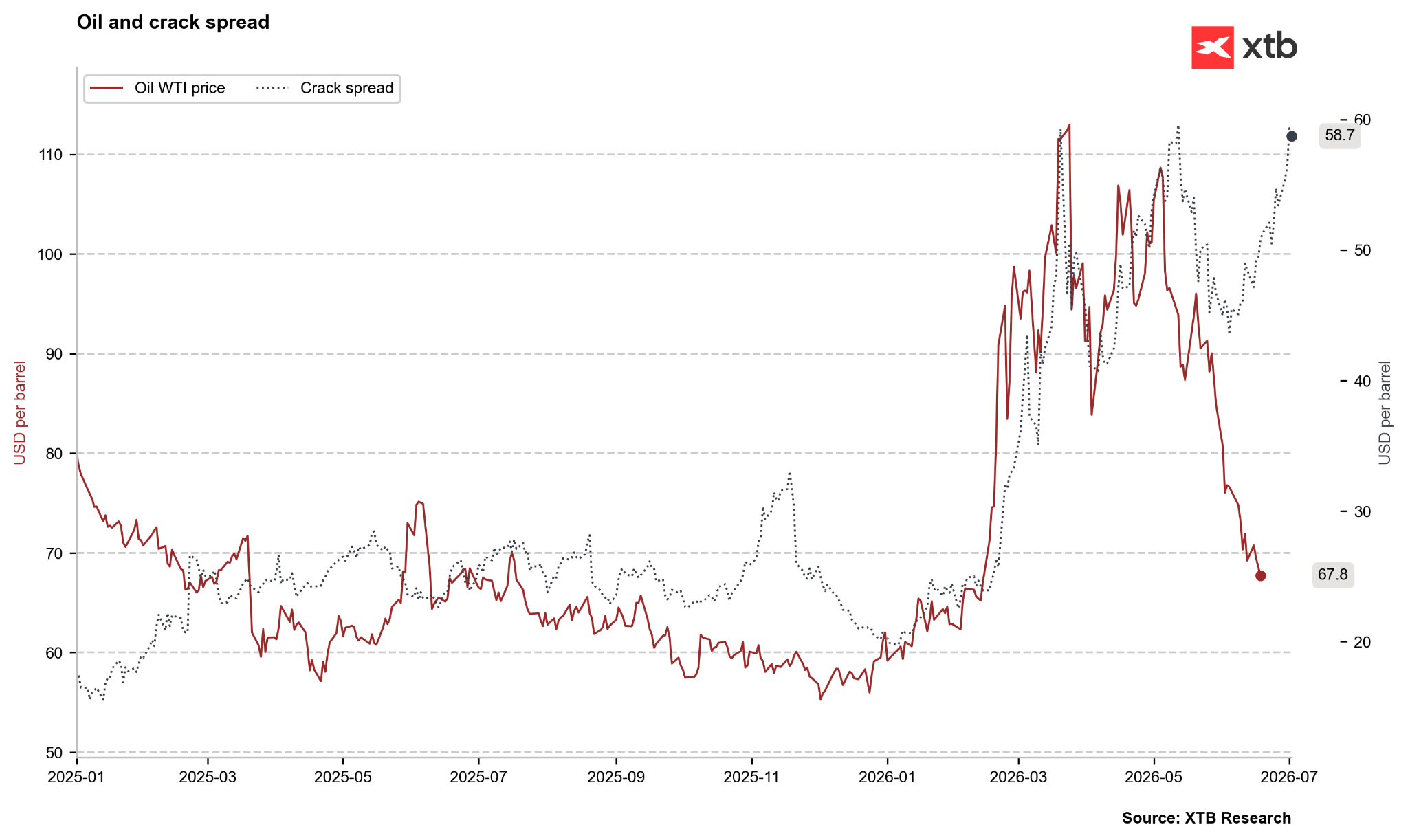

The crack spread, illustrating the difference between the prices of finished fuels and oil, shows a powerful disproportion. The price of oil is falling, while fuel prices remain at high levels or are even rising. This may be a temporary situation related to increased demand or show that the situation on the fuel market is far from normal. Source: Bloomberg Finance LP, XTB

The crack spread, illustrating the difference between the prices of finished fuels and oil, shows a powerful disproportion. The price of oil is falling, while fuel prices remain at high levels or are even rising. This may be a temporary situation related to increased demand or show that the situation on the fuel market is far from normal. Source: Bloomberg Finance LP, XTB

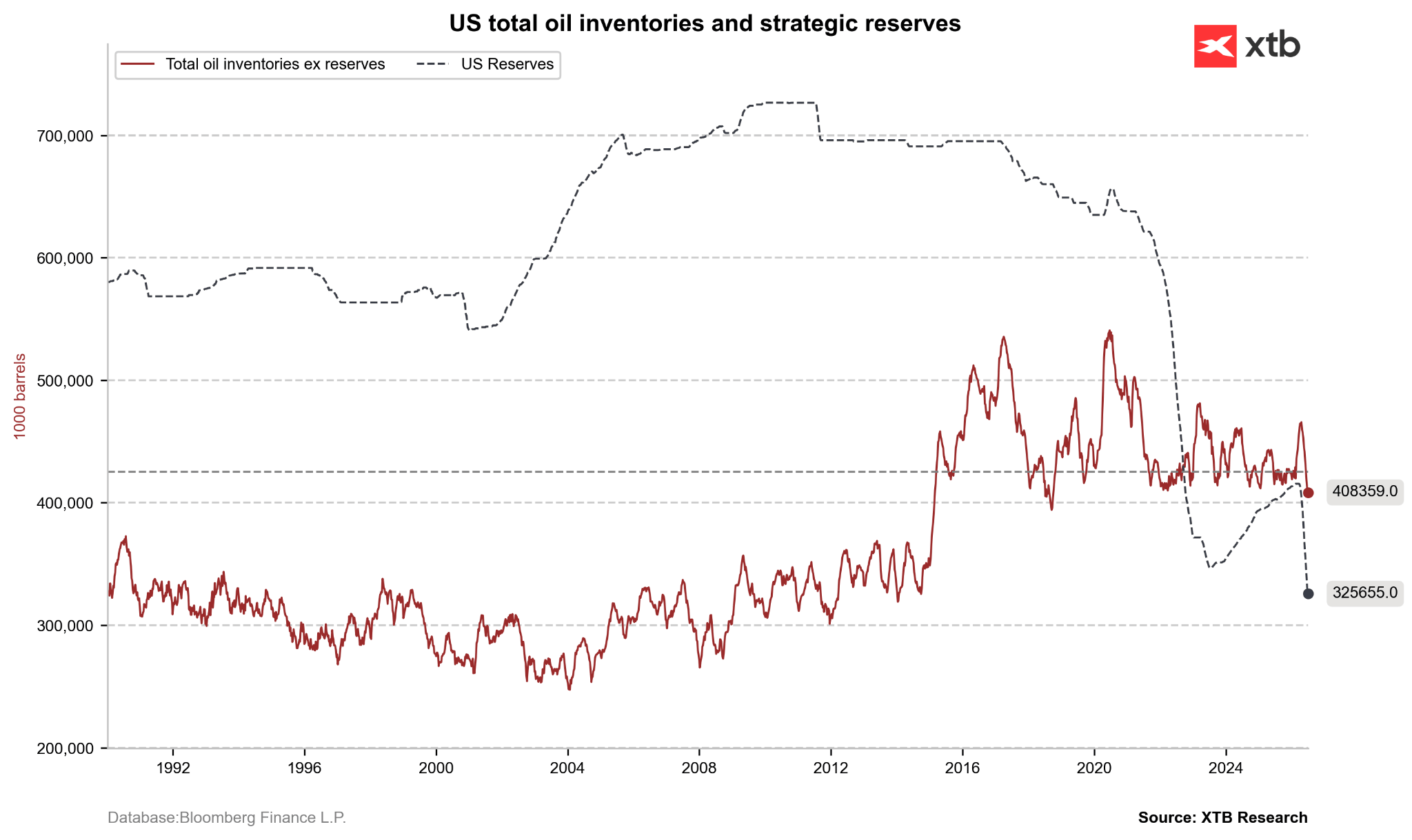

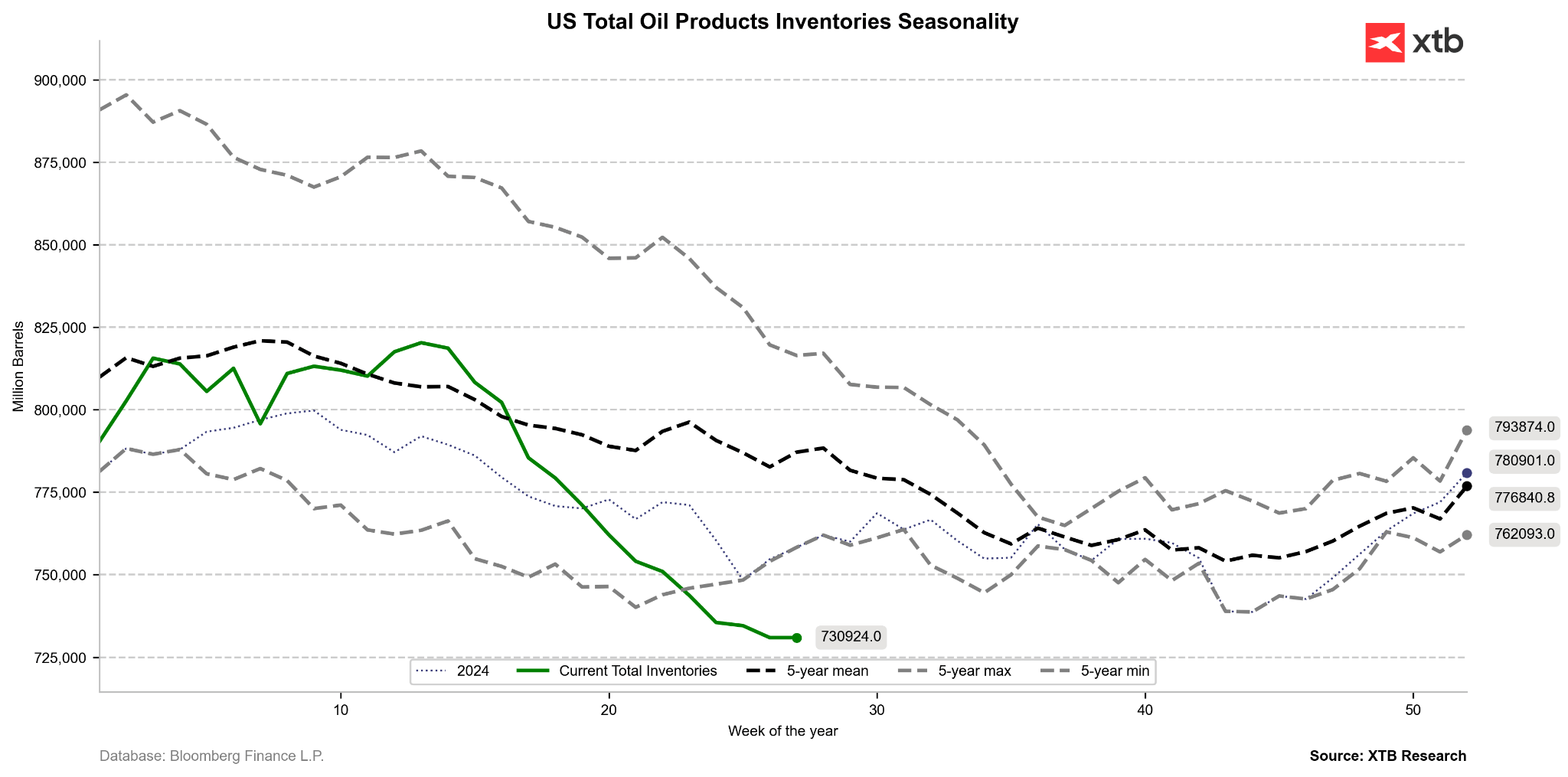

Four months of supply disruptions have led to a critical depletion of energy security buffers in OECD countries. To counteract the crisis, the IEA coordinated an unprecedented release of 400 million barrels from strategic reserves. As a result, the U.S. Strategic Petroleum Reserve (SPR) has shrunk to 325 million barrels, the lowest level since 1983. At the same time, commercial crude oil inventories in the U.S. remain 7% below the five-year average, and distillate stocks are depleted by 10%. This configuration leaves global refineries without a margin for error in the event of another supply shock. A potential failure of peace talks in Doha could trigger an immediate tightening of refining margins and a secondary inflationary impulse, which would drastically complicate the monetary policy pursued by the new Federal Reserve Chairman, Kevin Warsh.

Although it is still too early to see a recovery in inventories, the state of reserves and commercial stocks remains extremely low. Source: Bloomberg Finance LP, XTB

Although it is still too early to see a recovery in inventories, the state of reserves and commercial stocks remains extremely low. Source: Bloomberg Finance LP, XTB

Oil and product inventories have dived deep below 5-year minimum levels, although at the same time there is hope in the form of a slowdown in the downward trend. Source: Bloomberg Finance LP, XTB

Oil and product inventories have dived deep below 5-year minimum levels, although at the same time there is hope in the form of a slowdown in the downward trend. Source: Bloomberg Finance LP, XTB

Conclusions and Future Outlook

The spectacular fall in oil prices to around 70 USD per barrel proves that, with incredible speed, financial markets can dismantle the geopolitical risk premium in the face of diplomatic progress. However, in the longer term, the normalization of flows through the Strait of Hormuz reveals the problems that the oil market struggled with before the conflict, related to structural oversupply and simultaneously drained global oil and fuel inventories. Although from a technical and fundamental analysis perspective, the short-term downward trend may push WTI prices toward the demand zone at 62-65, ignoring the temporary nature of the agreement with Iran poses a significant risk to market participants. The lack of a lasting peace treaty, combined with historically low levels of strategic and commercial reserves, makes the current stabilization highly fragile, which could lead to a sharp return of volatility in the second half of 2026.

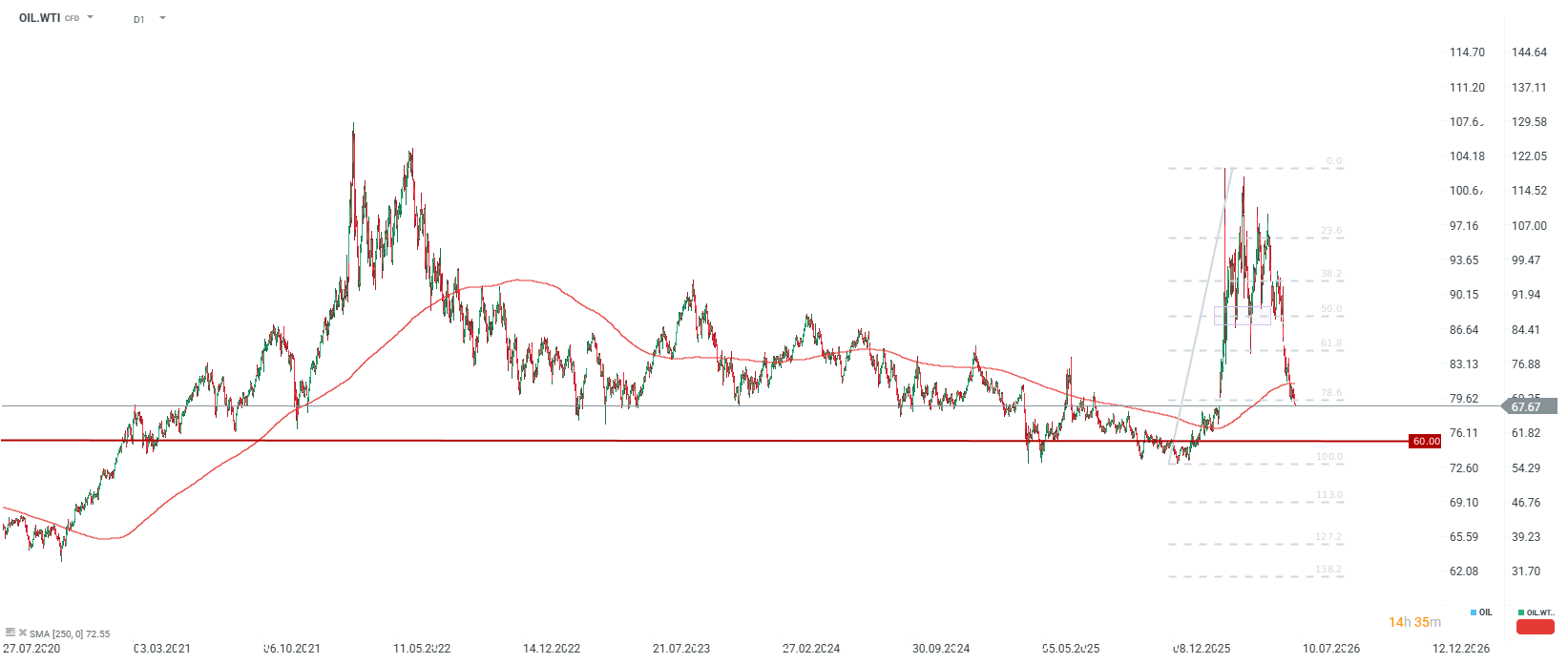

Nominally, we are dealing with a 43% price decline from the March peaks. In 2022, the peak-to-trough decline was a maximum of 50%, which would currently imply a level of 60 USD per barrel. However, it is worth noting that we are currently at levels similar to the 2022 lows, which are also close to the 5-year nominal average. Although technical momentum is clearly bearish, fundamentally, in the short term, it may seem that the declines are too steep, while at the same time, the outlook for next year remains clearly bearish, given the potential oversupply. Source: xStation5

Nominally, we are dealing with a 43% price decline from the March peaks. In 2022, the peak-to-trough decline was a maximum of 50%, which would currently imply a level of 60 USD per barrel. However, it is worth noting that we are currently at levels similar to the 2022 lows, which are also close to the 5-year nominal average. Although technical momentum is clearly bearish, fundamentally, in the short term, it may seem that the declines are too steep, while at the same time, the outlook for next year remains clearly bearish, given the potential oversupply. Source: xStation5

Defense sector ahead of earnings: Summary

🛢️Brent Crude Oil Tests $95 per Barrel

Morning Wrap: AI companies and gold back in favour? (22.07.2026)

Red Sea, but not the indices : The effects of the Bab al-Mandab blockade.

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.