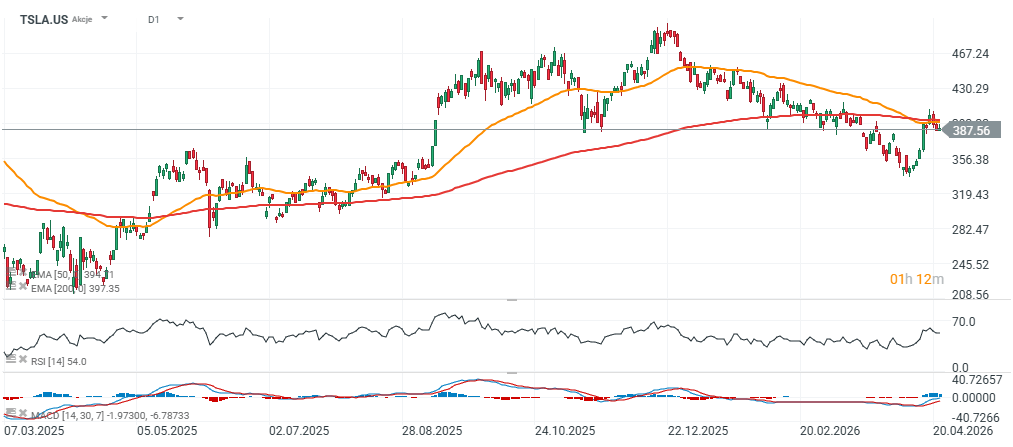

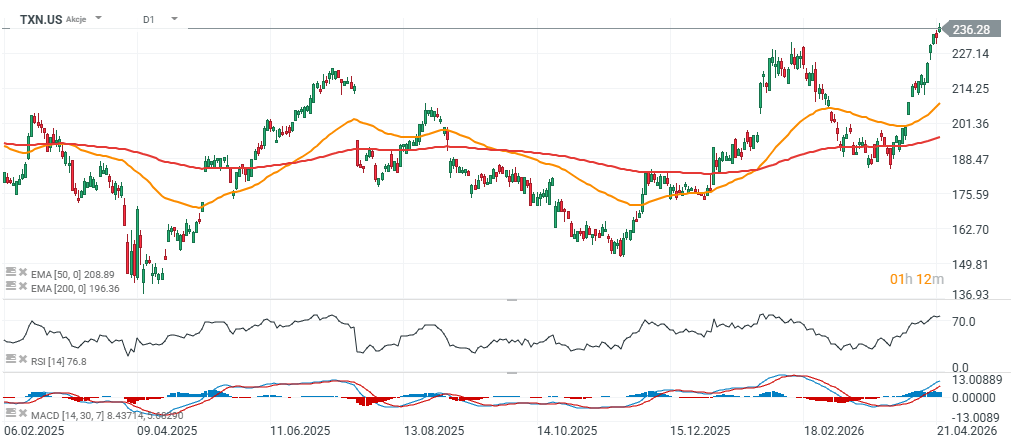

Today’s U.S. earnings calendar was clearly dominated by Tesla (TSLA.US), which beat market expectations on both earnings per share and revenue. On the other hand, IBM pulled back following relatively conservative guidance, while Texas Instruments surged nearly 9% after delivering a strong report pointing to a broader recovery in the semiconductor cycle.

Tesla: strong beat across key metrics - especially margins and cash flow; shares rise nearly 4% after hours

Tesla delivered a first-quarter report that surprised to the upside, particularly in the areas investors have been most focused on: profitability and cash generation.

- Adjusted EPS came in at $0.41, well above expectations of $0.34. Revenue reached $22.39 billion, also slightly ahead of consensus at $22.19 billion. Reported EPS stood at $0.13 versus $0.12 a year ago.

- The standout element of the report, however, was gross margin, which came in at 21.1%, significantly above market expectations of just 17.7%. This is a critical point, as margin compression has been one of the dominant concerns around Tesla in recent quarters.

Operating performance was equally solid. Operating income totaled $941 million, comfortably above the $787.7 million expected. Even more striking was free cash flow, which reached $1.44 billion, compared to expectations for a negative $1.86 billion. This magnitude of outperformance suggests that the quarter was not only strong on paper but also in terms of underlying cash generation quality.

Strong headline beat, but the AI pivot is getting more expensive

Tesla delivered a first-quarter report that clearly beat expectations at the headline level, particularly in profitability and cash generation. However, beneath the surface, the numbers suggest a company entering a more capital-intensive phase — one driven less by automotive efficiency and more by long-term bets on AI, robotics, and autonomy.

Margins and cash flow beat, but the cost base is rising fast

While the strength in margins and free cash flow surprised the market to the upside, a closer look at the cost structure points to a more complex picture. Operating expenses surged 37% year over year to $3.78 billion, reflecting Tesla’s accelerating investment cycle. As a result, operating margin fell to 4.2%, marking the second consecutive quarter of sequential compression — a sign that current profitability is increasingly being traded for future positioning.

Tesla is reallocating capital toward AI, robotics, and autonomy

This shift is not incidental. Elon Musk has been explicit about redirecting Tesla’s strategic focus toward artificial intelligence, including humanoid robots (Optimus), autonomous vehicles, and proprietary AI chips. These initiatives are no longer peripheral; they are becoming central to the company’s capital allocation decisions.

The decision to discontinue legacy models such as the Model S and Model X, and the possibility that the Model Y could gradually be sidelined in favor of the upcoming Cybercab, shows how aggressively Tesla is reshaping its product roadmap around autonomy and AI-driven mobility.

The core automotive business still looks mixed

At the same time, execution in Tesla’s core automotive business remains uneven. Vehicle deliveries — still the closest proxy for underlying demand came in at 358,023 units, missing market expectations and described by some analysts as an underwhelming start to the year. This suggests that while Tesla is advancing technologically, its traditional EV business is no longer the only engine of growth, and perhaps no longer the most important one strategically.

The long-term ambition is becoming much bigger than cars

Looking ahead, the scale of Tesla’s ambition is notable. The company expects volume production of the Cybercab and the electric Semi in 2026, while also signaling a major push into semiconductor infrastructure through a partnership with SpaceX to build what Tesla described as “the largest chip fab ever.” The logic behind that move is straightforward: Tesla expects future demand for AI-related compute capacity to exceed current and planned industry supply.

The investment case is becoming more ambitious — and more demanding

From a market perspective, this makes Tesla a more complex story to evaluate. The company is no longer just an automaker, or even just an EV manufacturer — it is increasingly evolving into a hybrid between an industrial company and an AI platform builder. That transition creates meaningful upside if execution holds, but it also brings higher execution risk, greater capital intensity, and less visibility on near-term returns. In short, the quarter confirms that Tesla can still produce strong financial results. At the same time, it makes clear that the company is deliberately moving into a phase where short-term efficiency may give way to larger, longer-duration strategic bets.

Source: xStation5

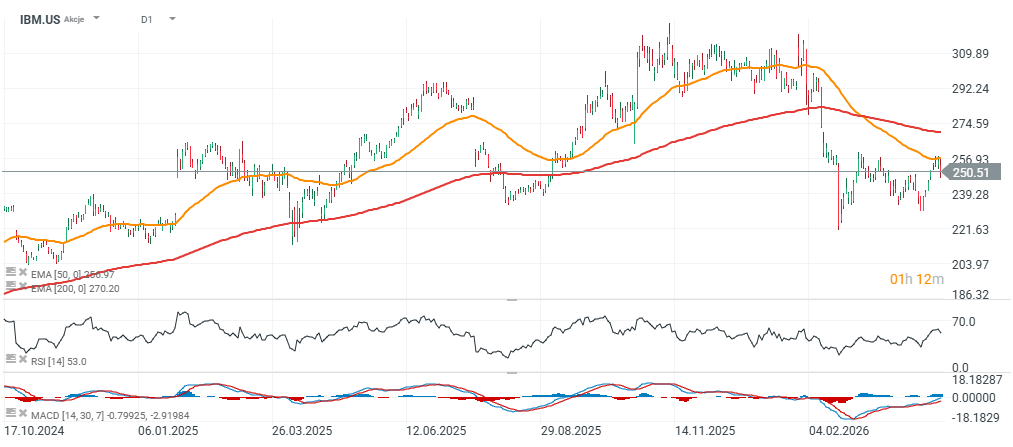

IBM: solid quarter above expectations, but conservative outlook weighs on the stock - shares down nearly 7% after hours

IBM delivered a broadly solid first-quarter report, beating expectations across most key metrics. Operating EPS came in at $1.91 versus a consensus of $1.81, while revenue reached $15.92 billion, exceeding forecasts of $15.67 billion.

- At the segment level, the software business remained stable, with revenue of $7.05 billion, essentially in line with expectations. The consulting segment came in slightly below forecasts at $5.27 billion versus $5.29 billion expected, though this does not materially alter the overall strength of the quarter.

- Cash flow was also a positive. Free cash flow reached $2.22 billion, slightly ahead of expectations. However, one notable omission was the lack of updated metrics related to IBM’s AI business, which may leave some investors wanting more clarity on this key growth narrative.

From a full-year perspective, management maintained its guidance. IBM still expects revenue growth of over 5% in constant currency terms, broadly in line with the market consensus of 5.1%. The company also reiterated its expectation for free cash flow to increase by approximately $1 billion year over year.

Source: xStation5

Texas Instruments: very strong quarter and constructive Q2 outlook — shares jump nearly 9% after hours

Texas Instruments delivered one of the strongest reports among semiconductor companies this earnings cycle, beating expectations on both revenue and operating profitability.

- EPS came in at $1.68 versus a consensus of $1.38, while revenue reached $4.83 billion, clearly above the expected $4.53 billion. This suggests that demand conditions in key end markets were stronger than anticipated.

- Operating profit also exceeded expectations, coming in at $1.81 billion compared to $1.54 billion forecast. Free cash flow reached $1.40 billion, above the $1.2 billion consensus, while capital expenditures were slightly below expectations at $676 million versus $689.9 million.

- Particularly important is the analog segment — the core of Texas Instruments’ business model. Revenue in this segment reached $3.92 billion, well above expectations of $3.68 billion. This is a key signal, as analog demand is often viewed as a proxy for broader industrial and electronics activity.

Looking ahead, the company provided constructive guidance for the second quarter. Texas Instruments expects EPS in the range of $1.77 to $2.05 and revenue between $5.00 billion and $5.40 billion. This suggests improving demand conditions and indicates that the company is entering the next quarter with stronger momentum.

Source: xStation5

Earnings bonanza for US banks

US Open: Nasdaq 100 gains 1% 🔼 Software stocks decline, JP Morgan rises after earnings

US CPI review

Software stocks slide on enterprise spending concerns 🚩 Microsoft drops 3%

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.