The most important market assumption regarding the conflict in Iran is that the conflict must, in the near future and in one way or another, end. This assumption is so widespread that most market participants do not even notice that they are making it. But what if this is an optimistic assumption?

The conflict in Iran has temporarily moved out of its hot phase and is now in a period of prolonged peace negotiations, interrupted by individual exchanges of fire between the US coalition and Iran and its proxies. Such a situation already has a precedent, for example the war in Ukraine.

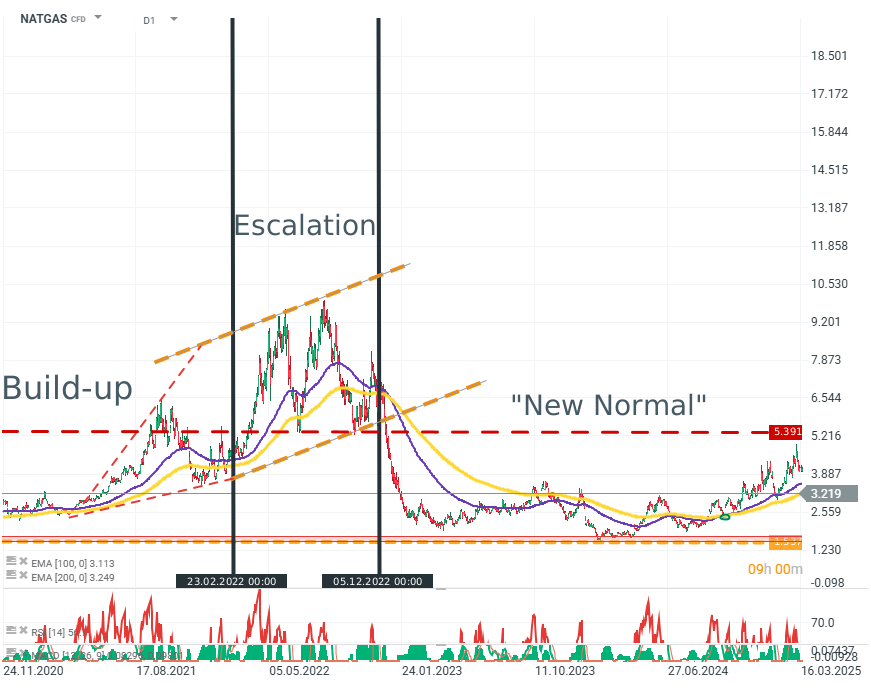

NATGAS (D1)

Although natural gas, especially when viewed through the lens of US contracts, is not an ideal medium for measuring sentiment, it remains an important indicator in the context of gas supplies to Europe during the first quarters of the war. Source: xStation5

During roughly the first half year of the conflict, a large part of the market expected the conflict to end in one way or another, if only because of the economic pressure it generated. This conflict has now lasted more than four years, and the catastrophic scenarios have not materialized for either side.

Could the same thing happen in the Persian Gulf?

Everything indicates that it could. This is not because the conflict is profitable, because it is economically devastating for both sides, but because both sides are prevented from making peace by impassable boundaries imposed on them by the realities of their political systems.

USA

- The US willingness to compromise is determined to a large extent by domestic pressures of a political and economic nature. Rising inflation expectations and falling indices are disastrous for the results of the political party currently in power. This is crucial in the context of the upcoming midterm elections.

- At the same time, as a military hegemon, the US still has various capabilities to overthrow the Iranian government and or partially occupy the country. It is not doing so because of political, economic and social pressure.

Iran

Iran’s situation is almost a mirror image of the American position.

- Iran does not have the military capability to threaten US forces in the region or to project power.

- Iran’s military capabilities are strictly limited to pacifying its own population and conducting missile and drone attacks, mainly against infrastructure.

- Despite lacking the capability to decide the conflict, Iran’s demands remain maximalist and include:

- Preserving its nuclear program

- Recognition of its control, or rather the transfer of control to it, over the Strait of Hormuz

- The removal of sanctions from the country.

Despite Iran’s military and economic weakness, it is simultaneously insensitive to political, social or economic pressure. It must be remembered that:

- Iran is a fundamentalist and totalitarian state. The factional nature of the Iranian center of power does not change this state of affairs.

- The Islamic Republic is a state unwilling, if not unable, to compromise, both internally and externally. This is clearly shown not only by the conflict itself, but by Iran’s reaction to the protests at the turn of 2025 and 2026.

What is also important, however:

- A peace agreement remains extremely unlikely, but not impossible

- Escalation of the conflict from the current level remains likely, but it is not currently the base case scenario.

Will the market get stuck in the strait?

Analysts and investors, in extreme situations, often rely on precedents. As I mentioned, precedents exist, but one must be careful not to confuse them.

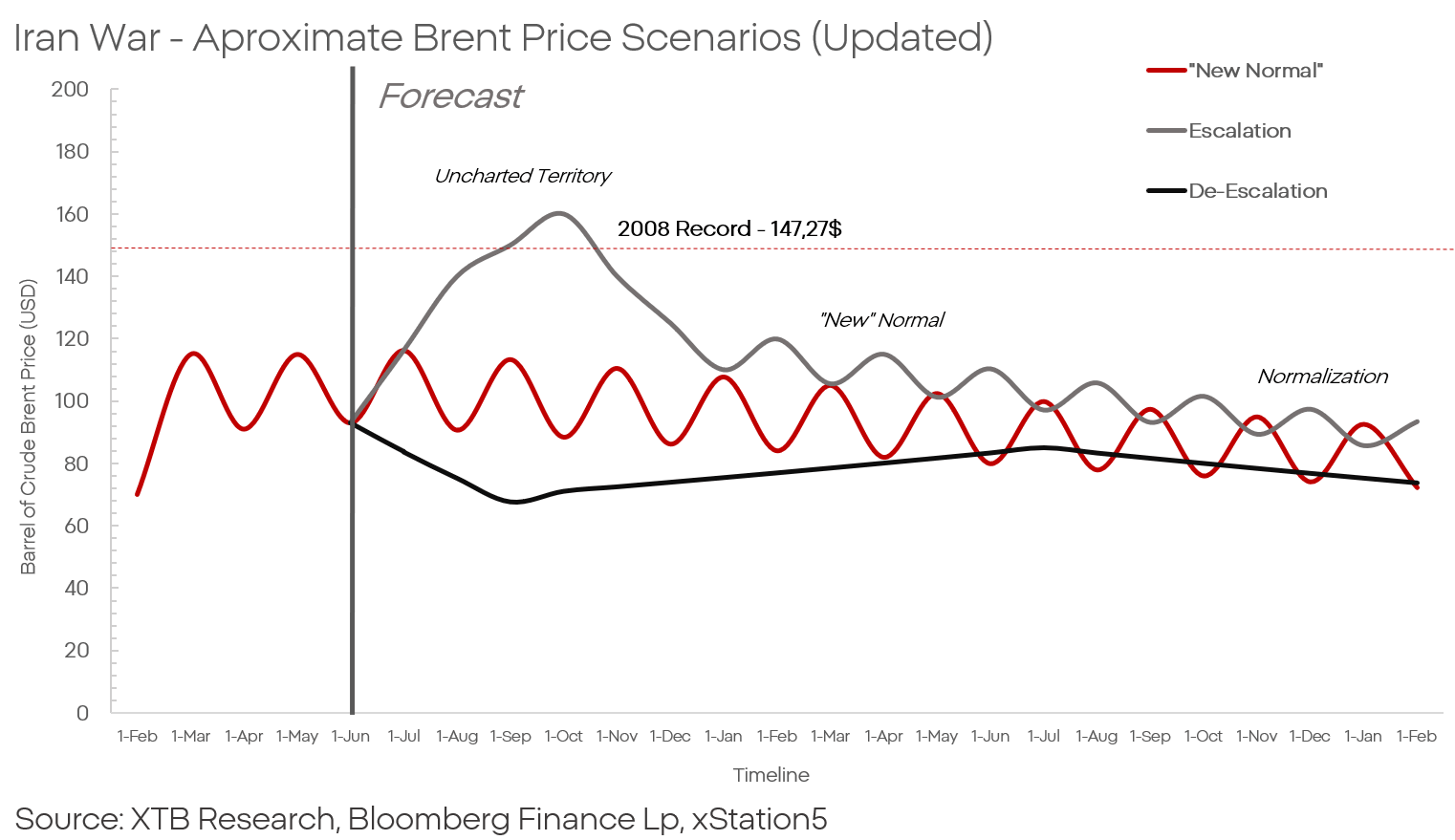

The year 2025 is not 2008 or the 1970s.

- The US is now a net exporter and the world’s largest producer

- Europe has a diversified network of energy supplies and energy sources

- Both economies are many times less sensitive to oil than they were a few decades ago.

- The oil market is additionally being cooled by weak consumer sentiment and the labor market, although in the context of recent data it is possible that the turning point is already behind us.

Oil will not be at 200 dollars because no one needs oil so badly anymore that they would pay that much for it.

The situation looks worse in Asia, where oil from the Middle East is still a foundation of the economy. Here, however, we have a two speed market, China and Japan on one side, and everyone else on the other.

It is Asian countries that are most likely to suffer from the conflict and from its long term nature the most.

China and Japan have enormous oil reserves and powerful financial systems capable of financing substitutes and emergency supplies. China is particularly important here. By burning through its oil reserves, China increases exports and floods the market with an ever larger volume of products. This is a key issue in the fight against inflation in developed markets.

Countries such as India, Vietnam and Indonesia are in a terrible situation. A lack of reserves or sufficient domestic production, combined with pressure on cheap labor from AI, places these countries among the biggest losers of the Gulf conflict.

Is that really the case?

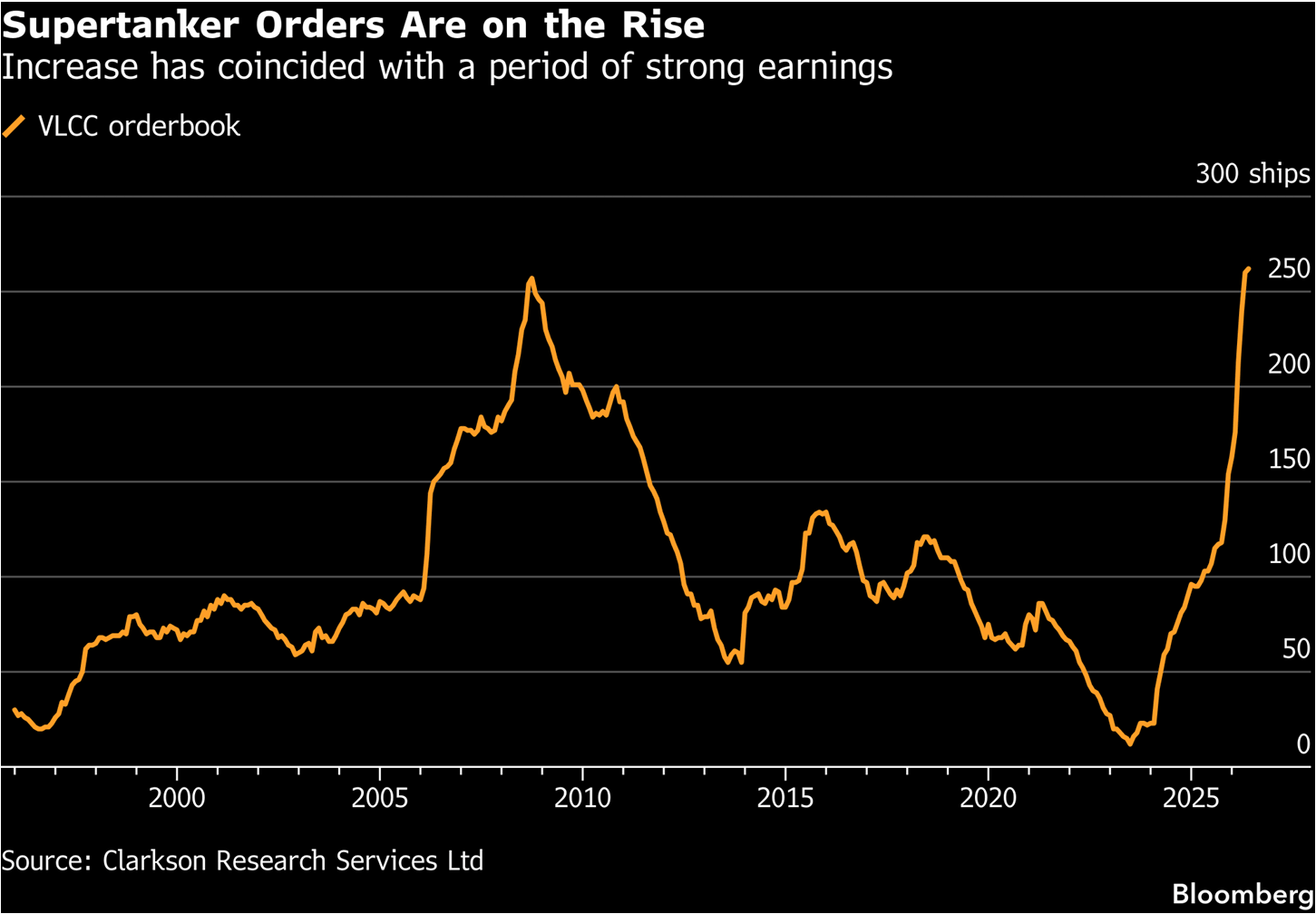

A narrow segment of investors who, because of proximity and expertise, have a much better quality of oil market forecasts are investors specialized in maritime logistics. Enormous cargo ships are the bloodstream of the global economy, and tankers are an important part of that bloodstream.

If companies and investors were discounting further bottlenecks in the Strait of Hormuz, why are tanker orders growing at the fastest pace in history? Because the market is most likely not pricing in the opening of the strait, but a fundamental change in the oil trade regime.

Source: Bloomberg Finance LP

In theoretical terms, price is a function of demand and supply. The demand side must compensate the supply side for risk, if such risk exists. If demand is able to cover a sufficiently high profit margin, then ultimately the commodity will reach the recipient. Nothing suggests that the oil and freight market should operate differently.

It can also be theorized that, given the relatively primitive way in which Iran conducts attacks on ships, it is possible that shipyards and shipowners will adapt vessels to operate in threatened regions. It is not a far reaching speculation that installing moderate armor and reinforcements, anti drone nets and commercial jamming systems on tankers would degrade Iran’s capabilities to an economically acceptable minimum...

...at the same time, demand for tankers is clearly cyclical, which is also visible on the chart. Ships built in the 1990s and 2000s are already at the end of their operating life and urgently need replacement. At the same time, sanctions on Russia, Iran and Venezuela have removed a significant amount of transport volume from the market, and that volume must be replaced.

On the other hand, however, the cyclicality of orders may also indicate a turning point and signal a peak in oil prices, after which a deep and prolonged selloff would follow. Such a scenario would become the base case if the US and Iran were, despite everything, able to reach an agreement.

Kamil Szczepański

Financial Market Analyst at XTB

🛢️Brent Crude Oil Tests $95 per Barrel

Morning Wrap: AI companies and gold back in favour? (22.07.2026)

Red Sea, but not the indices : The effects of the Bab al-Mandab blockade.

Daily Summary: A sell-off with a spin-off

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.