US index futures continue to advance as investors await the trading debut of SpaceX (SPCX.US), while oil prices have fallen to multi-month lows below $90 per barrel amid growing expectations that the United States and Iran are nearing a provisional agreement to end the conflict. Current indications suggest SpaceX could open around $165 per share, implying a market capitalization above $2 trillion on its first day of trading.

Nasdaq 100 futures are up nearly 0.9% after the index gained more than 3% in the previous session. European and Asian equity markets have also extended the risk-on move into the end of the week. Brent crude is down 4% and is on track for its first close below $88 per barrel since the opening week of the conflict. The decline reflects a rapid unwinding of geopolitical risk premiums as investors increasingly price in a diplomatic solution and the reopening of the Strait of Hormuz. Reports suggest a framework agreement could be signed as early as Sunday, with Iranian officials indicating that negotiations are nearing completion. The draft reportedly includes 14 provisions, including the reopening of Hormuz and a 60-day negotiation period on nuclear issues.

On Wall Street, the latest rally has once again been led by semiconductor stocks. Meanwhile, bond markets remain stable following Thursday's flight-to-safety move triggered by Middle East tensions. European bond yields are moving lower as easing energy prices reduce inflation concerns. The US dollar is stabilizing after four consecutive sessions of declines, gold remains close to recent levels, and Bitcoin is posting modest gains.

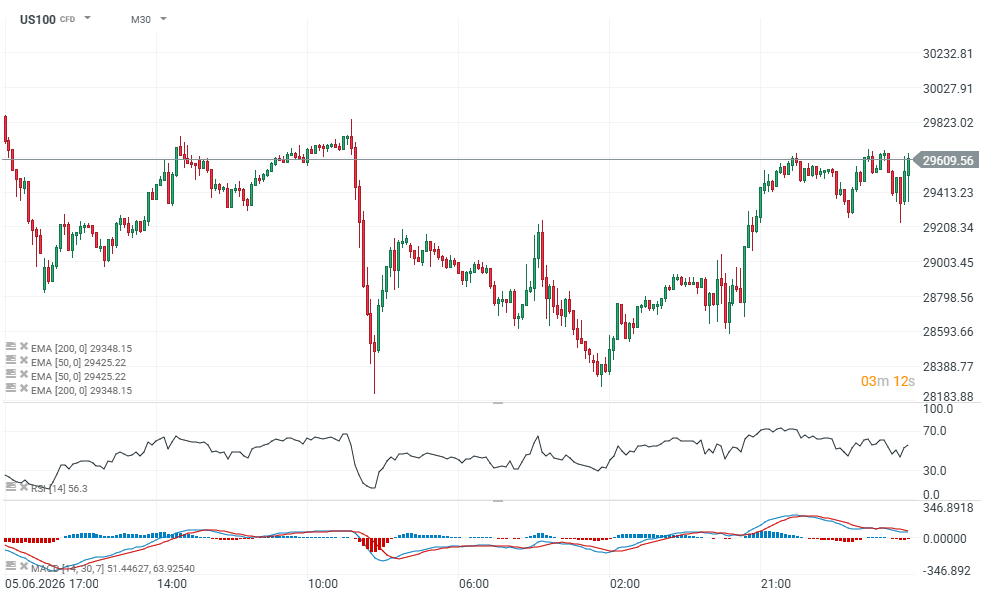

US100 (M30)

The chart suggests that Nasdaq 100 futures have almost completely erased yesterday's decline, which was initially driven by former President Trump's warning about a potential attack on Iran. Trump later softened those comments, although he recently acknowledged that negotiations between US and Iranian officials continue to face certain "frictions."

Source: xStation 5

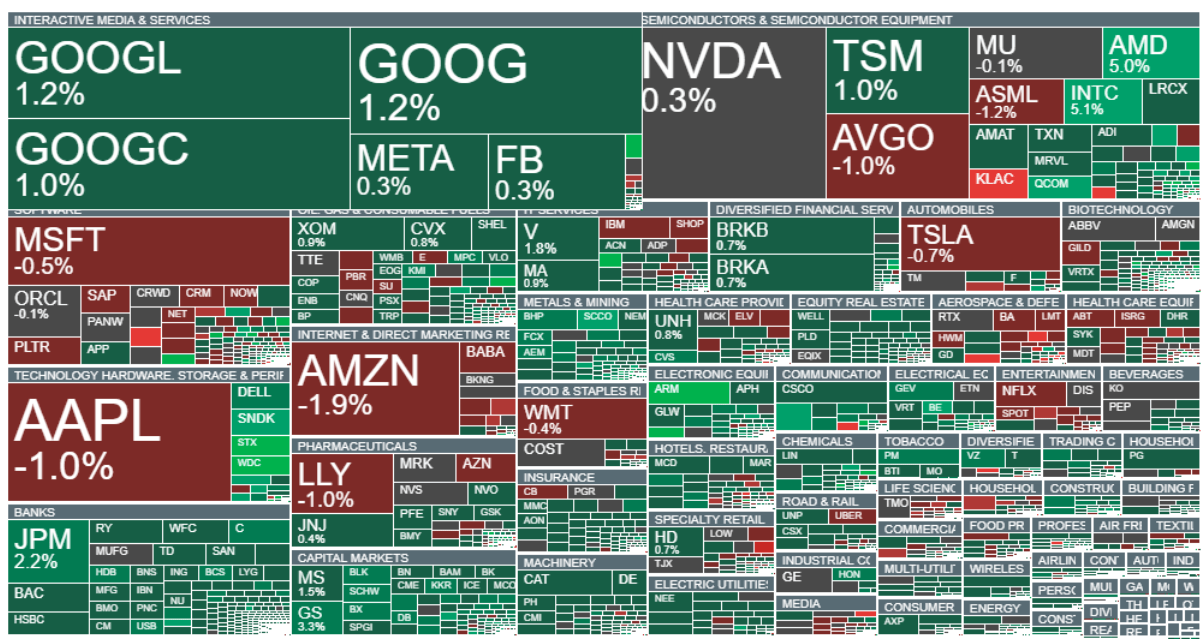

Despite weakness in KLA Corp, the semiconductor sector remains one of the strongest performers today. Memory-related companies such as SanDisk, along with Arm Holdings, are posting notable gains. Financial stocks and banks are also outperforming, while defense-related companies are among the weakest performers.

Source: xStation 5

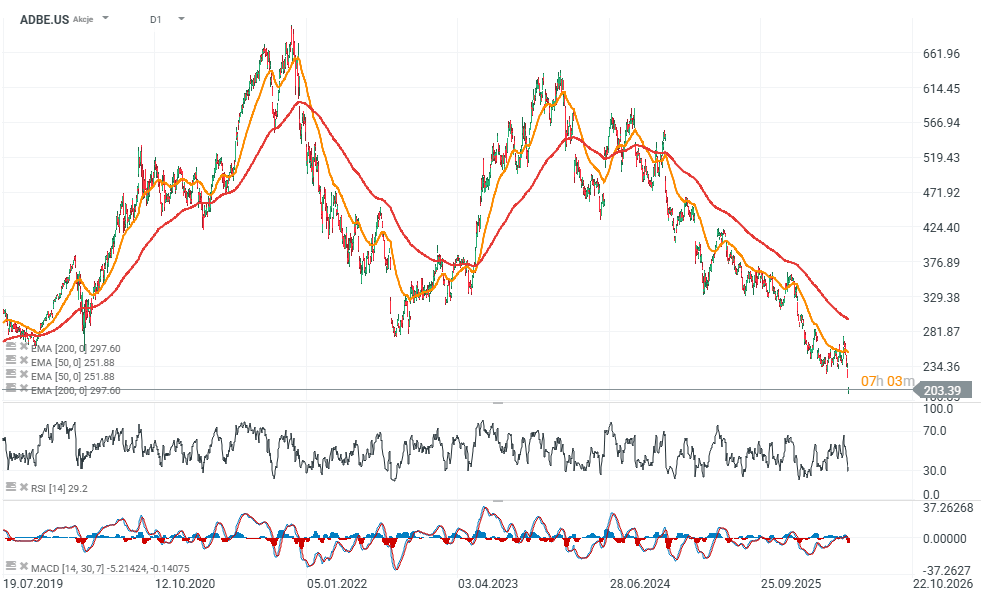

Adobe under pressure despite strong results as investors focus on slowing ARR growth

Adobe (NASDAQ: ADBE) shares remain under pressure following the company's fiscal Q2 2026 earnings release. Although Adobe delivered record revenue, stronger-than-expected growth, and raised its full-year guidance, investors focused on two negative developments: weaker expectations for organic ARR growth and continued leadership changes at the company. As a result, Adobe shares fell roughly 7%, while several major Wall Street firms downgraded the stock or lowered their price targets.

- At first glance, Adobe's financial results were difficult to criticize. Revenue reached a record $6.62 billion, representing approximately 13% year-over-year growth. Non-GAAP EPS came in at $5.96, while operating cash flow totaled $2.17 billion. Total ARR reached approximately $27.1 billion, and management raised its full-year outlook. However, investors concluded that the most important developments were hidden beneath the headline figures.

- The market's primary concern is the quality and sustainability of future growth. Adobe reduced its organic ARR growth outlook by approximately $480–500 million. Roughly half of the revision was attributed to delayed pricing initiatives, while the other half reflected the company's growing emphasis on a freemium strategy. Net new ARR excluding the Semrush acquisition reached $560 million, down 3% year-over-year. Analysts at Wolfe Research described the quarter as potentially "thesis changing," arguing that AI-related growth is not yet large enough to offset slowing momentum in Adobe's core subscription business.

- Another key issue is Adobe's strategic shift toward freemium offerings. Management is increasingly prioritizing user acquisition and engagement over near-term monetization. Several planned pricing initiatives have been postponed, raising concerns that future revenue growth could become more dependent on converting free users into paying customers. Analysts at Piper Sandler and BMO acknowledged that the strategy could expand Adobe's user base, but questioned whether the company will be able to monetize those users effectively in an increasingly competitive environment.

- Artificial intelligence remains one of Adobe's strongest growth areas. AI-first ARR more than tripled year-over-year to exceed $500 million, Firefly ARR increased 50% quarter-over-quarter, and monthly active users across Acrobat and Express grew from 700 million to 850 million. Nevertheless, investors remain skeptical because AI-related ARR still represents less than 2% of Adobe's total recurring revenue base. While the growth rate is impressive, the segment remains relatively small compared to the broader business.

Leadership changes have further amplified investor concerns. CFO Dan Durn will leave Adobe on June 15 to join Marvell Technology, while the company is simultaneously searching for a successor to CEO Shantanu Narayen, who is expected to transition to the role of Chairman of the Board. For many investors, the timing is problematic because Adobe is attempting to execute a major strategic transition centered around AI and freemium products. Evercore analysts noted that sentiment may struggle to improve until a new CEO and CFO are appointed and demonstrate credible execution of the company's long-term strategy.

Ultimately, the current selloff is not a reflection of deteriorating financial performance. Instead, investors appear concerned that Adobe may be sacrificing near-term profitability and ARR growth to build a larger free user base, while AI monetization remains too small to fully compensate for slowing growth in the company's traditional subscription business. As a result, Wall Street is increasingly focused on execution risk rather than the company's current operating performance.

Source: xStation 5

Oil rises over 3% 🛢️

Economic Calendar: Big Tech, Tensions Over Iran, and the ECB’s Decision ⏰

Morning Wrap: A New Threat of Conflict in the Middle East 🚨 (23.07.2026)

Tesla and Alphabet results round up

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.