Accenture shares are down around 15% in pre-market trading following the publication of its Q2 2026 results. Although the company beat market expectations on earnings per share and delivered a full-year outlook better than consensus, the stock is falling.

The negative investor reaction was mainly triggered by a series of large acquisitions in the cybersecurity sector. The market is currently bearish on cybersecurity, assuming that further AI development will make the industry lose its relevance.

Earnings

- Revenue came in at $18.7bn, below the consensus of about $18.8bn, but still 6% higher y/y.

- EPS was $3.80 versus $3.72 expected.

- New bookings totaled $19.3bn, compared with $19.7bn a year earlier.

- Operating margin increased by 20 basis points to 17.0%.

Guidance

- The company now expects full-year EPS of $13.78-$13.90, versus market expectations of $13.80.

- Accenture also expects FY 2026 revenue growth of 3-4%.

- Free cash flow guidance was maintained at $10.8-$11.5bn.

Controversial purchases

The transactions announced alongside the results drew the most market attention. Accenture announced plans to acquire a majority stake in Dragos and to acquire runZero and NetRise in full.

The combined enterprise value of these transactions is about $4.17bn. Closing is expected in August or September 2026, subject to regulatory approvals.

Accenture’s management presents these deals as a strategic strengthening of its position in operational technology security (OT Security). CEO Julie Sweet said the acquisitions are intended to increase the company’s market share and create a new growth platform.

The market, however, sees the purchases mainly as short-term pressure on results and large spending on a sector viewed as lacking strong prospects. Integration of the new businesses into the company’s operations is also being questioned.

Context

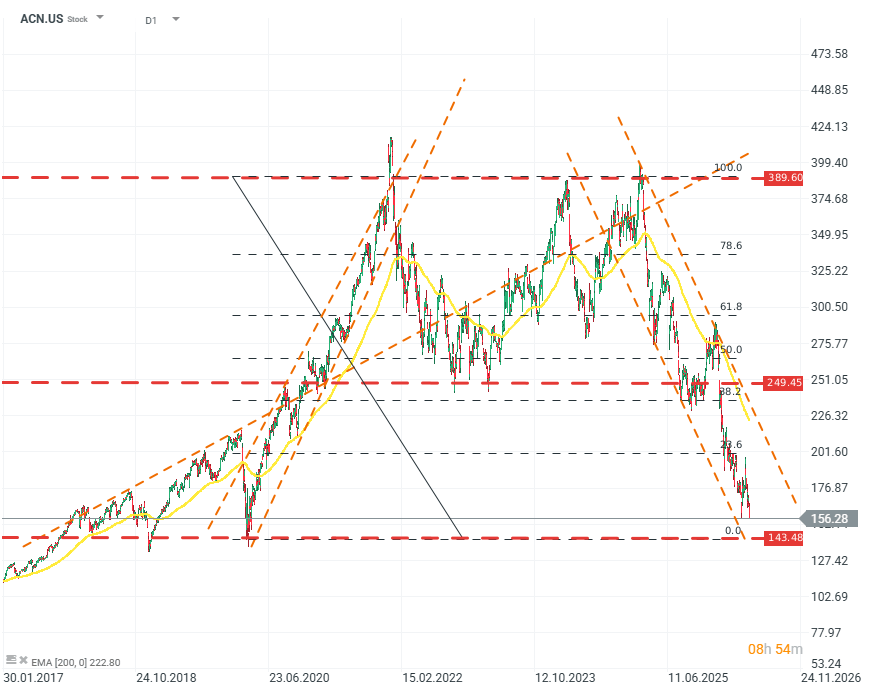

ACN.US (D1)

From a valuation perspective, the company has not had a good period. It is now trading close to the valuation levels seen at the bottom of the sell-off during the market’s reaction to the COVID-19 pandemic. From its peak, the company has lost more than 70% in valuation, and 40% in valuation this year alone. Importantly, profits and profitability do not indicate a decline or a significant loss of growth momentum. The company has reached a P/E of 13 and a price-to-sales ratio of 1.4. Source: xStation5.

Daily Summary - The market starts to doubt rate hikes after Warsh, but Trump destroys the rebound

US OPEN: Wall Street Holds Its Breath Ahead of Fed Decision and Tech Giant Earnings

SK Hynix earnings: Did market over-sold?

France Challenges Palantir, Market Reacts.