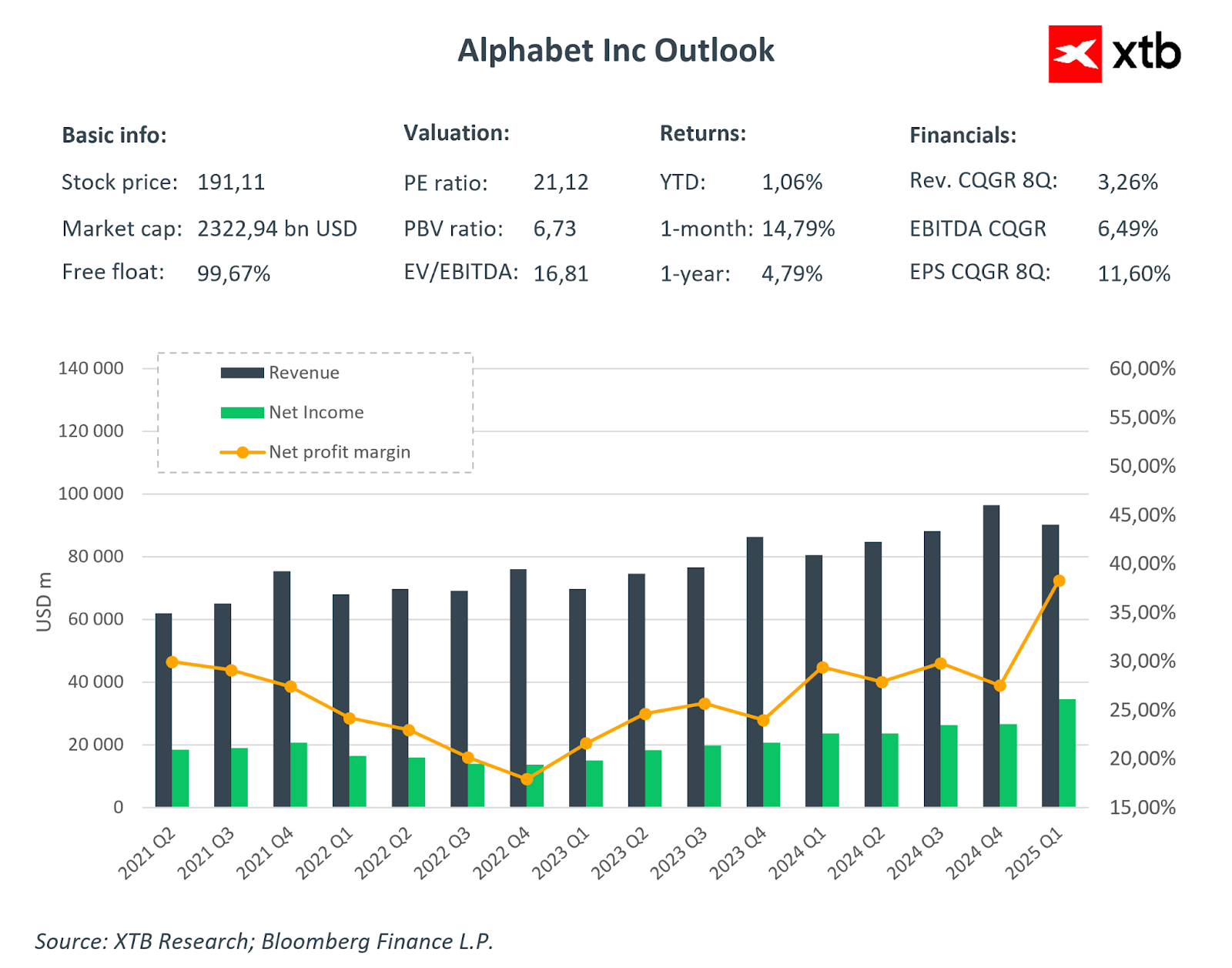

Today, after market close, Alphabet (GOOGL.US), along with Tesla, will kick off the earnings season for the "Magnificent Seven" companies. This earnings season, the key focus will remain on the revenue growth rate in the most dynamically developing cloud segment, and investors will also be closely watching how the crucial advertising segment

Q2 2025 Outlook

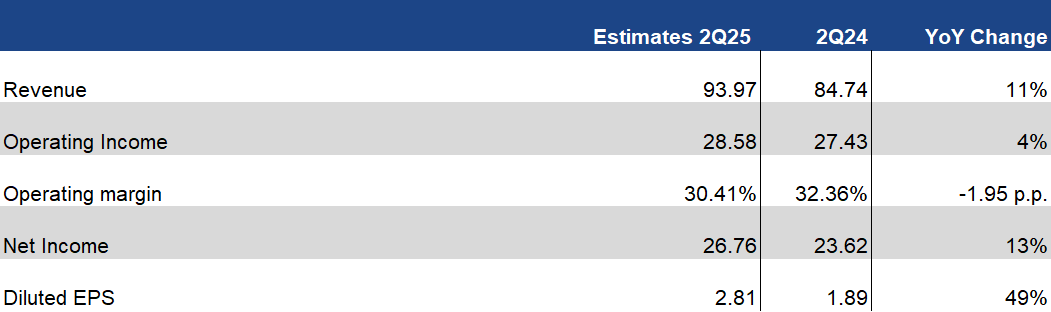

Expectations for Alphabet's results remain high. Market consensus predicts the company will report its second-highest quarterly revenue in history (after Q4 2024). Strong revenue growth (+11% y/y) is expected to slightly outpace the operating profit growth, which will result in an anticipated decline in operating margin to 30.4% (from 32.4%). It's worth noting that in recent quarters, the operating profit margin remained elevated, so a nearly 2 percentage point decrease should be interpreted more as a normalization of elevated values rather than a weakening of the company itself.

On the other hand, net profit growth is expected to improve, increasing by 13% to $26.76 billion. As a result, adjusted earnings per share (EPS) are projected to reach $2.81, translating to nearly 50% year-over-year growth.

Selected financial estimates for Q2 2025. Source: XTB Research, Bloomberg Finance L.P.

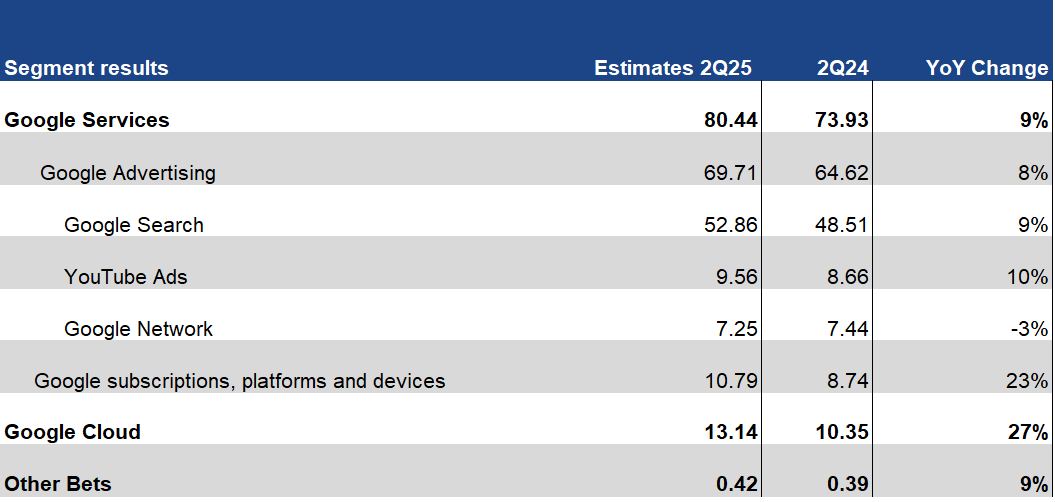

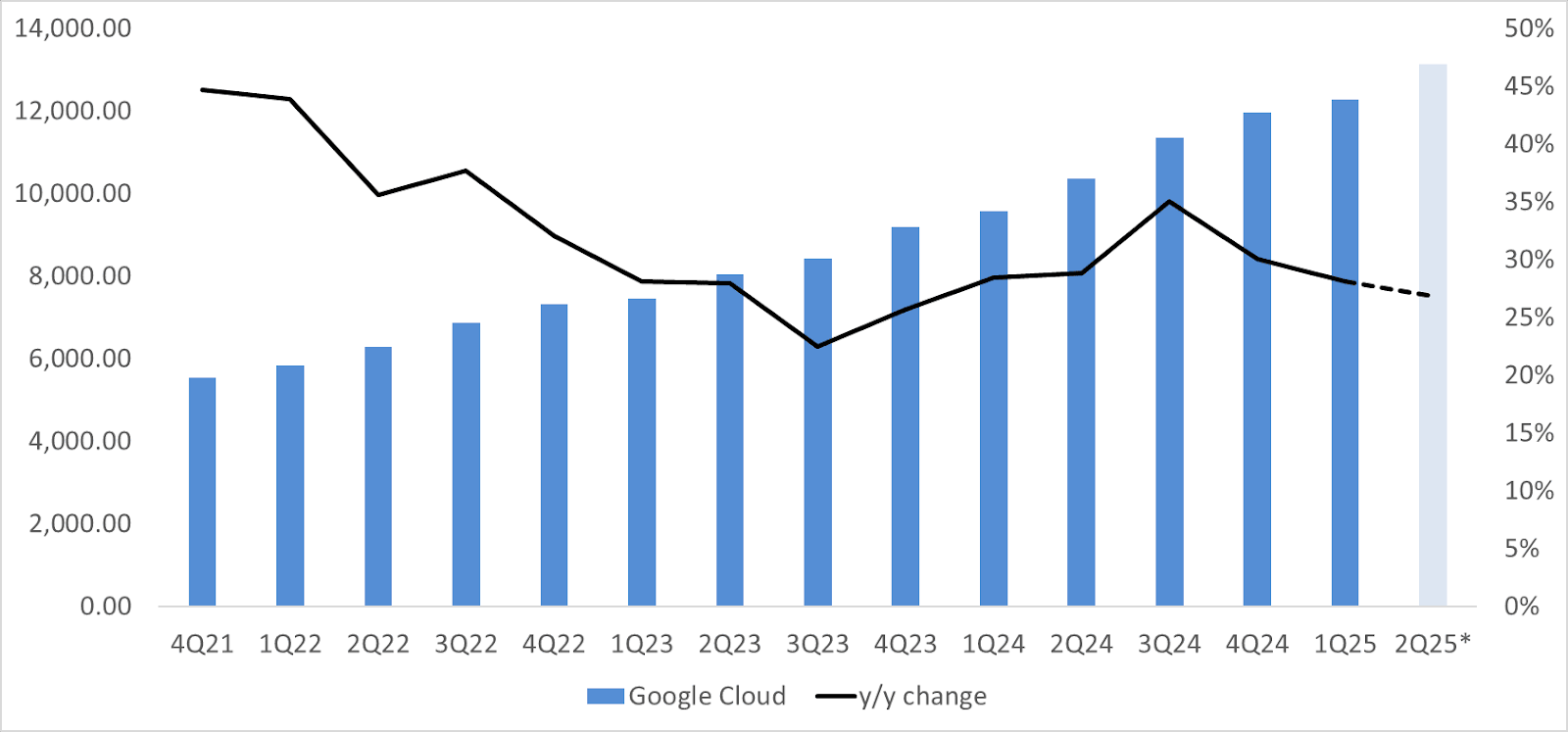

Looking deeper into the company's business segments, we can see that the Google Cloud segment continues to show the highest projected growth. Consensus forecasts a 27% year-over-year increase, which would translate to $13.14 billion and simultaneously mark the highest cloud revenue in the company's history. The Google Advertising segment is also expected to demonstrate healthy growth, driven by solid dynamics in Google Search (+9% y/y) and a 10% increase in revenues generated by the YouTube platform.

Selected financial estimates for Q2 2025. Source: XTB Research, Bloomberg Finance L.P.

Aside from EPS (whose forecasts were lowered by 5%), analysts have maintained a neutral stance on Alphabet in recent months, without significantly changing their predictions.

Key Segments

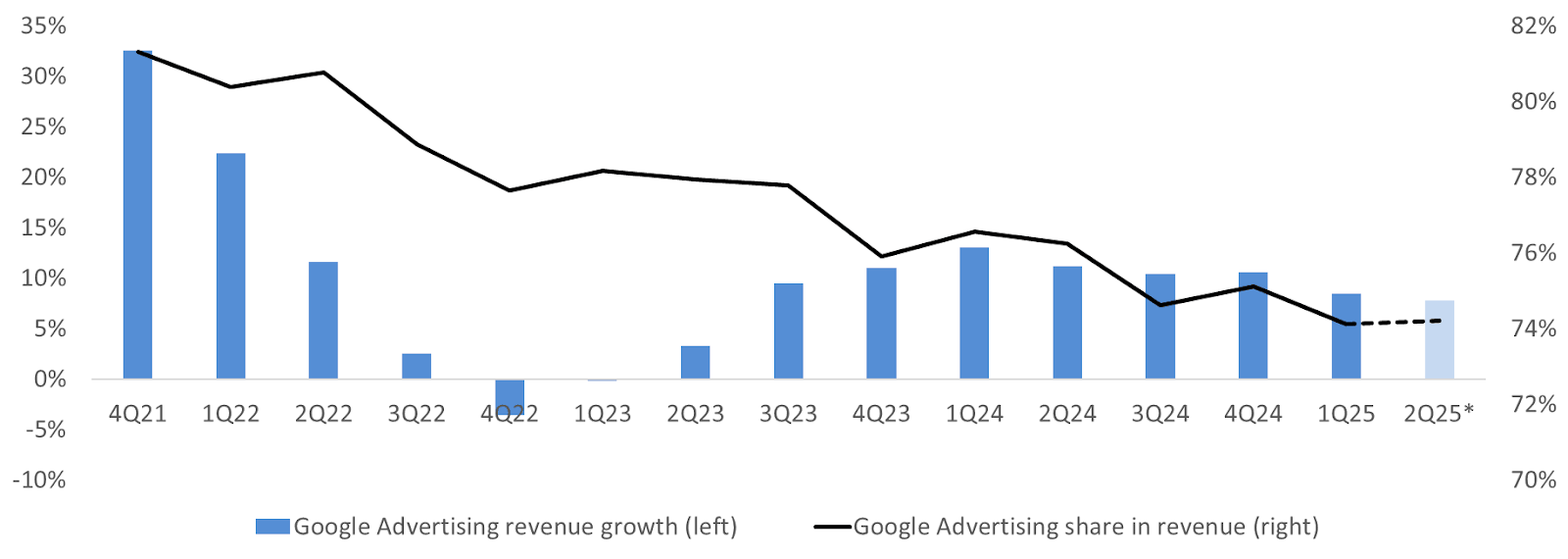

Revenue from Google's advertising segment remains fundamental to maintaining Alphabet's strong sales performance. Hence, investors treat this topic with high attention and scrutiny. A weakening of this segment could have a significant impact on the company's overall finances, as despite a decrease in its revenue share, it still accounts for nearly 74% of the company's total revenue. It's worth noting in this context that the declining share of advertising revenue in total company sales is not due to a decrease in the segment's revenue, but rather its slower dynamics relative to other segments (especially cloud). Nevertheless, it continues to show solid levels, oscillating around 8-10% since Q4 2023.

Source: XTB Research, Bloomberg Finance L.P.

If Alphabet reports strong results in the advertising segment, investor attention will shift to the cloud segment, which has been the company's fastest-growing segment for over 14 consecutive quarters. Amidst the development of AI, market consensus expects a slowdown in revenue growth to 27% year-over-year, mainly due to a high base effect. The revenues themselves, at $13.14 billion, are projected to be the highest quarterly revenues in the cloud segment in the company's history.

Source: XTB Research, Bloomberg Finance L.P.

Valuation before earnings

Alphabet, unlike other Big Tech companies, can boast a slightly larger margin for error in terms of valuation. The company is currently trading at levels approximately 20-30% lower than its averages over the last year (which have increased compared to previous years due to higher valuations of the "Magnificent Seven" relative to the rest of the market). At the same time, Alphabet remains the lowest valued (in terms of fundamental indicators) among all seven Big Tech companies. This somewhat places less pressure on the company relative to other "Magnificent Seven" members, for whom maintaining elevated valuations may pose a particular challenge this earnings season.

Source: Bloomberg Finance L.P.

Daily Summary: Equities Diverge as Tech Lags, Europe Rallies on Earnings & PMIs (24.07.2026)

US OPEN: Nasdaq hits 1-month low! Geopolitics bring AI trade down!

Market Wrap: European Stocks Are Trying to Rebound as the Week Comes to an End💡

Alphabet shares are down 22% from their all-time high 🚩 Is Google ready to resume its bull run?