Apple, once the undisputed leader in consumer technology products, now lags behind competitors in the race for artificial intelligence dominance. While Google and Microsoft are presenting groundbreaking generative AI features – from advanced coding assistants to real-time music and video generation – Apple at WWDC 2025 is focusing more on incremental changes rather than revolutions, as was the case in the past, primarily during Steve Jobs' era.

The most important new feature to be unveiled is the release of its own AI models to third-party developers, but their scale (3 billion parameters) remains far behind the latest achievements of the competition. On the other hand, it's important to remember that the ultimate recipient of Apple products is the consumer, not a large corporation. Nevertheless, the breakthrough conversational Siri, based on large language models, has been postponed again, and other anticipated AI features, such as a new Health app, will appear no earlier than 2026.

Design and Ecosystem: Apple Leans on its Strengths

In the face of delays in artificial intelligence, Apple is emphasizing its traditional strengths: product design and ecosystem consistency. This year, the company is presenting a new "Solarium" interface – a refreshed look with transparency and light effects will cover iOS 26, iPadOS 26, and macOS 26. For the first time since 2007, the Phone app will be thoroughly rebuilt, and a new, central Games app is intended to strengthen Apple's position in the gaming segment. On the other hand, it's important to remember that competition from Nintendo and Sony remains very strong.

Is Apple's Financial Situation Still Strong?

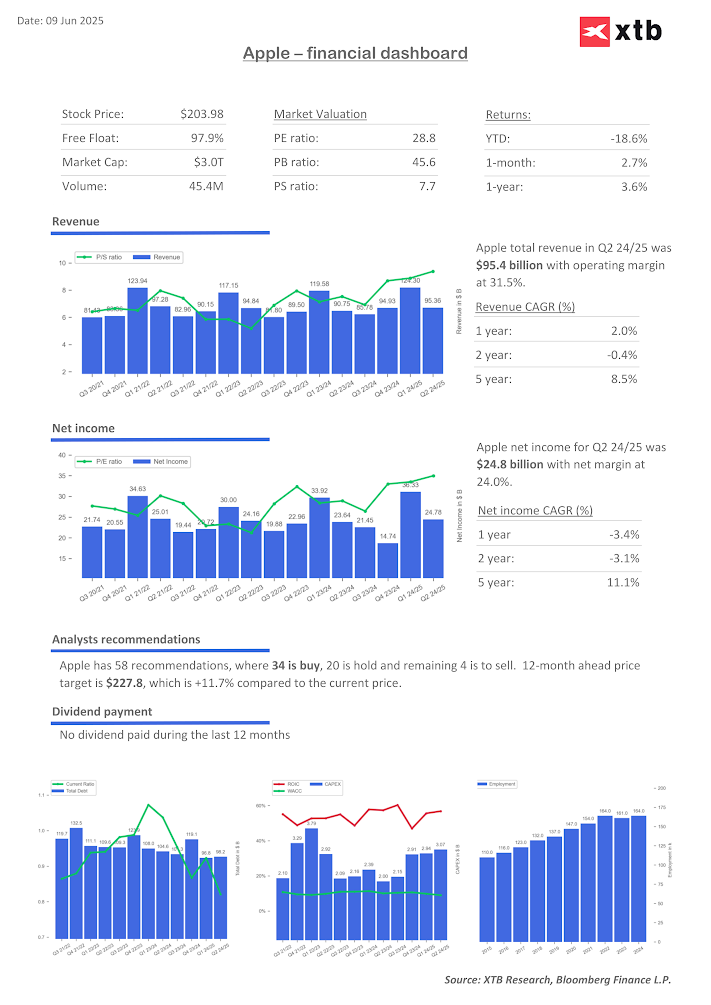

In recent months, the company hasn't boasted spectacular results:

- Stock price: A decline of 18% since the beginning of the year makes the company one of the weakest in the Mag7 group. It's second only to Tesla, which suffered significantly from the turmoil between Musk and Trump.

- Revenue and net profit: The company's revenue amounted to $95.3 billion, with an operating margin of 31.5%. However, the company is experiencing a clear slowdown in revenue growth (CAGR) to 2.0% for the last year and 8.5% over the last 5 years. In terms of profit, the result was $23.8 billion, with a net margin of 24%. The CAGR for the last year was negative at -3.4%, with a 5-year net growth dynamic of 11.1%.

- Analyst recommendations: Among 58 analysts, only 34 recommend "buy" – a very low percentage compared to other tech companies. The company also has several "sell" recommendations. The average 12-month price target is $227.8, implying an almost 12% increase.

Strategic Risks: Tariffs, China, and Hardware Competition

Apple's problems don't end with AI. The company is facing rising tariff costs (estimated at $900 million this quarter) and must quickly rebuild its supply chain, which has been heavily reliant on China. iPhone shipments in China have fallen by over 20%, pushing Apple to fifth position in that market. Hardware competitors, such as Meta and OpenAI (collaborating with former Apple designer Jony Ive), are increasingly demonstrating that they will be able to compete with Apple in the premium hardware market.

Investors and Consumers Remain Loyal

Despite the challenges, Apple can still count on a loyal user base, high-margin services, and solid cash flow. These strengths help maintain a relatively high valuation, although growth remains far behind the competition. Increasingly, Apple is perceived as a "safe haven" in the stock market, rather than a growth engine.

The company has been lagging behind the broader Nasdaq 100 technology index in recent weeks. Source: xStation5

Daily Summary: Equities Diverge as Tech Lags, Europe Rallies on Earnings & PMIs (24.07.2026)

US OPEN: Nasdaq hits 1-month low! Geopolitics bring AI trade down!

Market Wrap: European Stocks Are Trying to Rebound as the Week Comes to an End💡

Alphabet shares are down 22% from their all-time high 🚩 Is Google ready to resume its bull run?