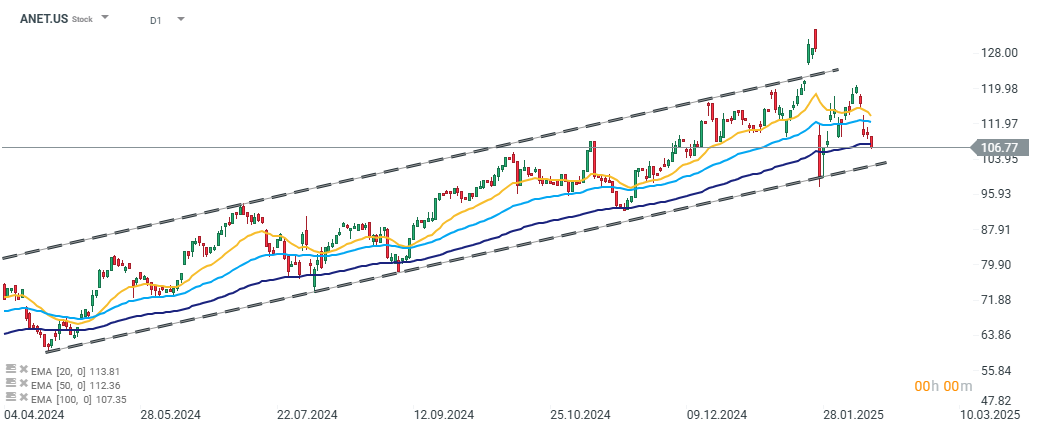

Arista Networks (ANET.US) will report its 4Q earnings after today's session. The company has remained in a stable and strong upward trend since the beginning of 2024. Over the past year, it has increased in value by nearly 130% at its peak and is currently trading about 81% higher than at the start of 2024.

Following a sharp market reaction at the end of January to news about DeepSeek technology development, Arista Networks experienced a significant sell-off, dropping 25% from its peak. Despite recovering some ground in the following weeks, the stock currently appears to lack clear direction in the short term. A strong Q4 earnings report could provide the momentum needed to break out of this stagnation. Source: xStation

At the same time, the company continues to show strong earnings growth, and its high valuation multiples (e.g., P/E of 51.3x) do not deter investors. This is due to Arista maintaining an average annual growth rate of 32% over the past three years, with EPS growing nearly 50% annually.

Q4 Earnings Estimates. Source: Bloomberg Finance L.P.

Q4 2024 Forecast

Arista operates in a rapidly growing market. The widespread adoption of database-related solutions is a key driver of its revenue growth. While the beginning of this year has cast some doubts among investors regarding sustained high AI-related capital expenditures, it is still unlikely that companies will step away from using these solutions. This suggests continued strong demand for Arista’s products, creating room for further earnings acceleration.

Market consensus expects $1.9 billion in revenue for Q4, representing 23% year-over-year growth. While this is lower than the company's three-year CAGR, it's important to note that Arista is grappling with a rising revenue base effect. Additionally, a 23% revenue increase would mark the highest growth rate in five quarters.

There is also optimism regarding operating profit, with analysts forecasting a 45% operating margin, the highest in the company’s history.

Despite a weak earnings season in the US and a general tendency among analysts to lower estimates, Arista has seen an increase in average forecasts over the past four weeks, reinforcing confidence in the company’s potential.

However, despite expectations for strong Q4 results, the company is likely to maintain its previous guidance for 2025. There are still no details on key future contracts. While planned capital expenditures by companies like Microsoft and Meta for 2025 are encouraging, investors should prepare for the possibility that Arista will not raise its forecast.

It’s also worth noting that Arista Networks has beaten earnings expectations for the past eight consecutive quarters. Given the negative sentiment surrounding this earnings season, investors’ heightened reaction to companies that fail to surpass expectations, and Arista’s elevated valuation multiples, the stock could face a significant decline if it disappoints.

Estimated Q4 2024 Results:

- Estimated revenue: $1.9 billion

- Estimated product revenue: $1.6 billion

- Estimated service revenue: $294.3 million

- Estimated cost of revenue: $688.3 million

- Estimated product cost of revenue: $633.7 million

- Estimated service costs: $58.5 million

- Estimated operating margin: 45%

Economic calendar: Wednesday brings big Q2 earnings and PPI inflation (15.07.2026)

Morning Wrap: What’s next with the Strait of Hormuz, inflation and US interest rates? (15.07.2026)

US Open: Nasdaq 100 gains 1% 🔼 Software stocks decline, JP Morgan rises after earnings

Software stocks slide on enterprise spending concerns 🚩 Microsoft drops 3%