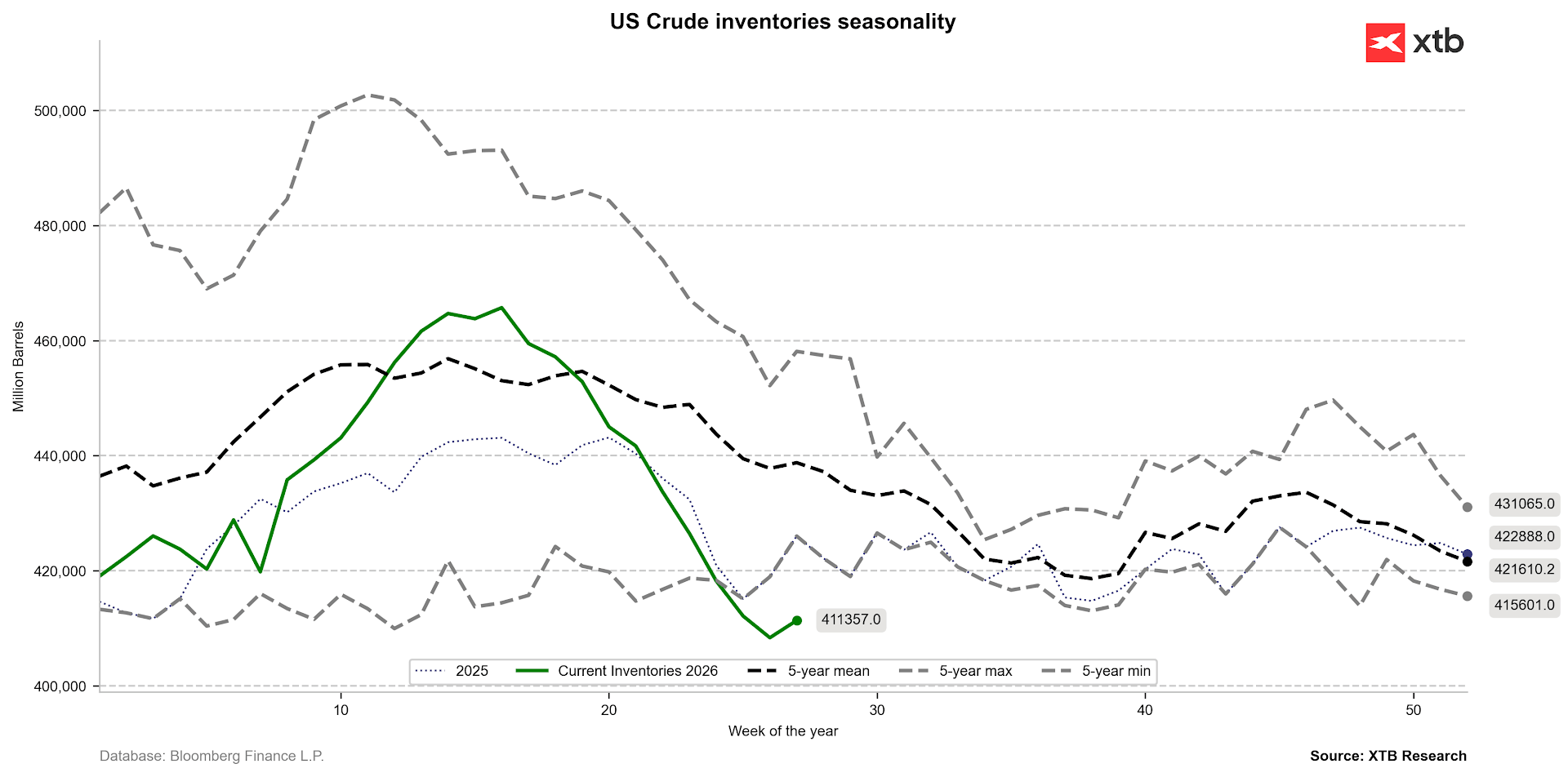

Key inventory changes (weekly)

- Crude oil inventories: +3.00 million barrels (a decline of about 1.1 to 1.6 million barrels was expected).

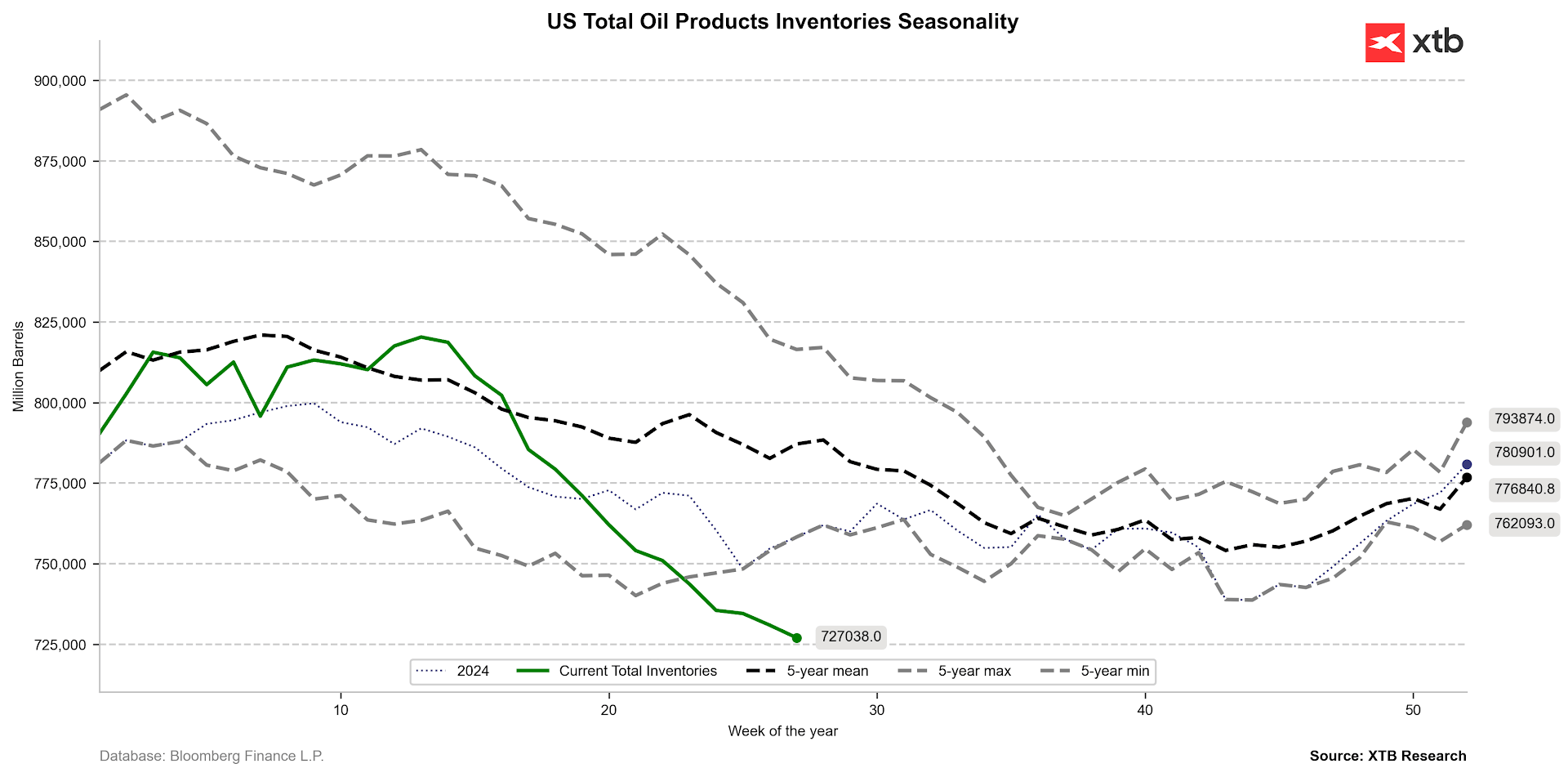

- Distillate inventories: -4.98 million barrels (a rise of +1.05 million barrels was expected).

- Gasoline inventories: -1.90 million barrels (a decline of -1.5 million barrels was expected).

- Cushing inventories: -0.052 million barrels (a slight decline).

- Refinery capacity utilization: -0.8 percentage points (a smaller decline of -0.2 percentage points was expected).

- Oil imports: +350 thousand barrels per day (bpd).

- Domestic oil production: +50 thousand barrels per day (bpd).

Market commentary

The latest EIA report brings a strongly mixed, though ultimately quite balanced, set of data. On one hand, there is a big surprise regarding crude oil inventories themselves, which rose by a full 3 million barrels instead of the decline expected by the market. This is the first inventory increase since the second half of April. This was contributed to by, among other things, a clear increase in imports (+350 thousand bpd) and a slight decline in raw material processing by refineries, whose utilization fell more than forecast (by 0.8 percentage points).

On the other hand, this same decline in refinery activity, combined with sustained demand, has led to a very deep depletion of finished fuel inventories. The decline in distillate inventories by nearly 5 million barrels (versus an expected increase!) and a stronger-than-forecast decline in gasoline inventories are acting strongly bullish on oil product prices and are effectively neutralizing the "bearish" tone of the crude oil itself.

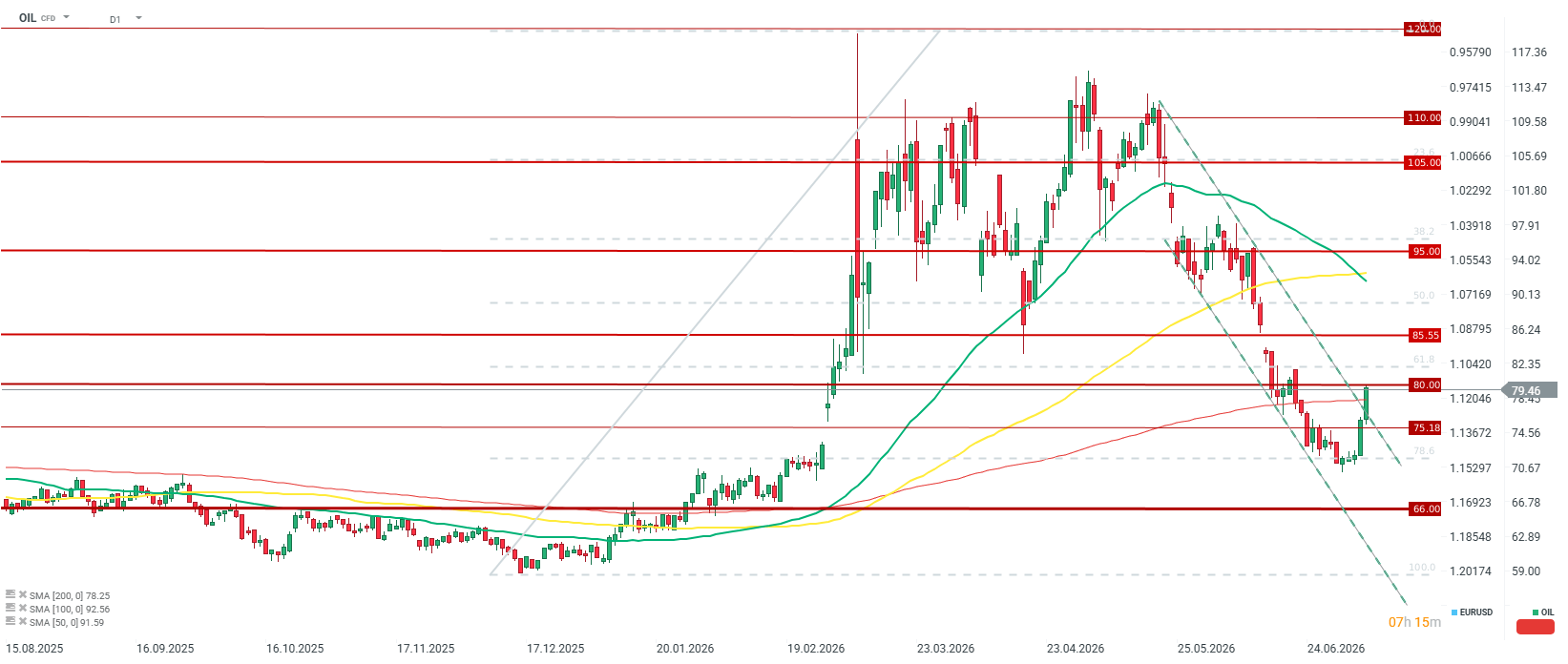

Despite these interesting shifts in US storage data, the price reaction of the commodity (Brent around 79.50 USD) reminds us of the broader context. The reaction to weekly EIA reports may currently be limited or short-lived because to a large extent, everything now depends on the geopolitical situation in the Middle East. The tensions there, the risk of conflict escalation, and the potential threat to supply continuity are now dictating the main direction for oil prices in global markets, pushing typical fundamental data from the US slightly into the background. After earlier uncertainty, Donald Trump has again announced readiness to attack Iran, which is driving price increases to nearly 80 USD per barrel.

Daily Summary: Markets limit the pullback while awaiting the Fed

The semiconductors sell-off continues 📉

US OPEN: Deeper sell-off and a SaaS rebound

The coffee market in the grip of weather and empty warehouses: The paradox of record Brazil harvests