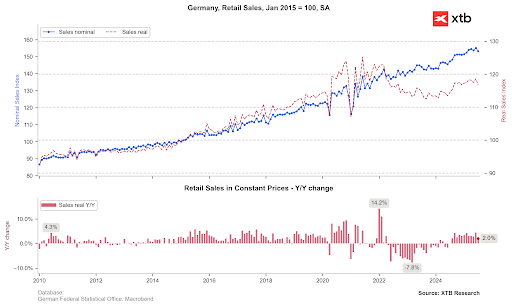

EURUSD began today's session with a degree of weakness, following the release of poor German retail sales data and lower producer inflation (or rather, deflation). German retail sales fell by 1.5% month-on-month and rose by only 2.0% year-on-year, a significant slowdown from the nearly 5% growth seen in June. Such weak data undermines the narrative of a robust European consumer.

Additionally, data from France and Spain was released. French inflation remains extremely low at 0.9% year-on-year, although it did see a monthly increase of 0.4%. In Spain, CPI inflation remains elevated at 2.7% year-on-year but failed to rise as expected to 2.8%.

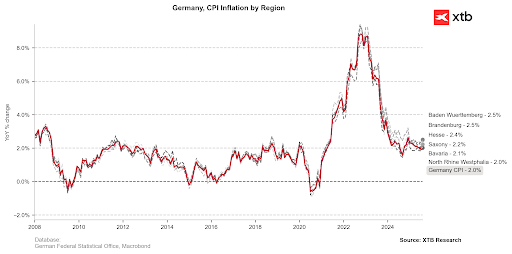

However, we have seen a significant surprise from individual German states, where data has come in notably above expectations, suggesting a considerable rebound in August's CPI inflation. These figures will be released in the early afternoon. For instance, inflation in Brandenburg rose to 2.5% year-on-year from a previous reading of 2.2%. Almost all states saw inflation come in higher than previous levels, though there were virtually no month-on-month changes after the last strong rebound.

Expectations for German inflation point to a rebound to 2.1% year-on-year from 2.0%, with a month-on-month reading of 0.0%. However, there is room for an upside surprise, which should reinforce the ECB's stance to hold interest rates at its upcoming meetings.

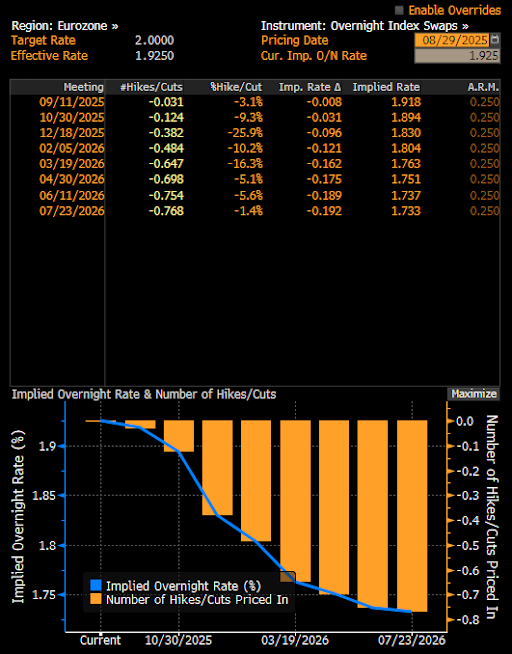

Expectations indicate an almost zero probability of a rate change at the September meeting. For December, the market is pricing in just under a 40% probability. Source: Bloomberg Finance LP, XTB

EURUSD has recovered almost all of its morning weakness thanks to the higher data from the German states. It is worth noting that the pair has reacted to the 1.1600 level four times in recent weeks. Nonetheless, at 1:30 PM BST today, we will see the US PCE inflation data, which could set a new tone for the pair. If inflation proves to be higher than expected, it could temper the strong market expectations (85%) for a Fed rate cut in September. Conversely, if it turns out that tariffs do not have as much of an impact on consumer prices as some Fed members have suggested, confidence in a September move could increase. This might encourage the pair to re-test the 1.17 level, which marks the upper boundary of the descending trend channel.

Wheat climbs to the highest level since May 2024 🚜 Black Sea export risks fuel rally

Oil rises over 3% 🛢️

Economic Calendar: Big Tech, Tensions Over Iran, and the ECB’s Decision ⏰

Morning Wrap: A New Threat of Conflict in the Middle East 🚨 (23.07.2026)