The company lost over a dozen percent of its market value during Monday’s session, and at the peak of the correction as much as 20%. One of the most promising IPOs in the industry in recent years is starting to look increasingly less attractive - what are investors worried about, and are those concerns justified?

Even before the latest episode, Czechoslovak Group had been performing below market expectations. This was, however, more a matter of unrealistic investor expectations than poor management on the company’s side. CSG produces mainly small arms and light vehicles; a company of this type has little chance of catching up with market leaders in terms of growth pace and, above all, margins.

It was also reflected in the valuation: as recently as Friday, the stock was trading more than 40% below the IPO price.

The situation has deteriorated from bad to disastrous - driven by the short-selling fund “Hunterbrook Media.”

In its publication, Hunterbrook pointed to a number of alleged irregularities. These mainly include:

An unclear status of certain investors and counterparties

- Hunterbrook raises a series of uncomfortable yet important questions:

- The Spanish company FMG was suspended by NATO’s procurement agency. CSG maintains that FMG’s operations remain beyond reproach and that the decision does not affect shareholders’ interests, as FMG was excluded only from the NSPA procurement process. That may be the case; however, the company did not address NATO’s allegations and did not disclose this in the IPO prospectus.

- A complex network of links and transactions involving minority shareholders as well as various politicians and businessmen (often openly connected to Russia) this is a very serious and dangerous accusation.

- The materials provided by Hunterbrook do not conclusively prove conscious wrongdoing to the detriment of shareholders, but they do provide serious grounds to suspect the company of harmful or even illegal practices.

Inflated declared production capacity

- Hunterbrook also points to far-reaching overinterpretation regarding the company’s declared ammunition production capacity - ammunition that accounts for over 60% of the company’s current revenues. Hunterbrook’s investigation suggests the company’s actual production capacity is only about 100–300 thousand 155 mm shells versus more than 600 thousand declared by CSG.

- The problem is not the lack of production capacity itself, but rather the nature of the company’s business model. If the allegations against CSG were confirmed, it would mean the company relied on resale/refurbishment of ammunition rather than its production. This would not be such a major issue were it not for the fact that globally available ammunition stocks that can be purchased on a semi-open market are close to depletion.

- If these allegations were true - and one can partly lean toward them based solely on the company’s historical context, as it has in fact repeatedly operated under such a model in the past - it could imply a collapse in margins and/or sales.

CSG responded to the allegation by calling it baseless, while refusing to provide detailed explanations. Still, it is hard to blame the company for this: CSG is part of NATO’s security ecosystem, and any facility or logistics hub is a constant target for entities acting on Russia’s behalf.

Contrary to the typical standard of short-seller publications, the Hunterbrook report is not a groundless accusation. Moreover, the fund’s analysts’ claims, while not unassailable, are coherent enough to seriously question how the company operates.

However, it should be remembered that such a fund is not a neutral party, and the publication has a clear goal of pushing the company’s valuation down. Before drawing further-reaching conclusions, it is important to wait for more detailed explanations from CSG, which the company has committed to provide.

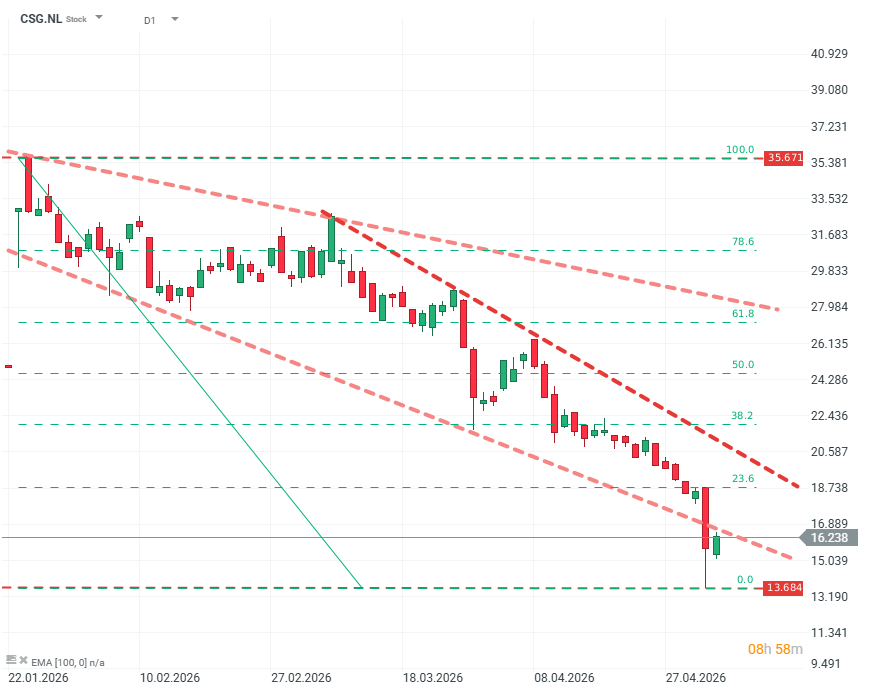

CSG.NL (D1)

Weak sentiment toward the company’s valuation appears to be worsening further, setting an increasingly steep downward trend. Source: xStation5.

BREAKING: Iran and US are back at the negotiation table?! Oil takes a step back, stocks tick up!

Daily Summary - Escalation in the Middle East. FOMC fears inflation

FOMC Minutes: Hawkish tone confirmed. EURUSD rebounds nonetheless

Trump in Ankara does not signal total escalation. Oil limits gains, and Nasdaq parries losses