Investor sentiment on Wall Street is gradually stabilizing following comments from Donald Trump, who indicated that the US is speaking with “the right people in Iran” and that Tehran is willing to reach a deal. He also stated that the US has won the war, which he hopes is now nearing its end. Trump added that a different group is now in power in Iran, suggesting that the main objective of the conflict has been achieved. He also mentioned that Iran did something positive yesterday regarding the Strait of Hormuz, although he did not specify what he meant. According to sources, direct US-Iran negotiations could take place as early as this Thursday.

- The S&P 500 is trading flat and has managed to erase earlier session losses, while the Nasdaq 100 is slightly weaker, down over 0.4%. The semiconductor sector is clearly outperforming in the US equity market today, with gains also continuing among oil and gas companies—shares of Chevron and Exxon Mobil are rising. Cheniere, a US LNG exporter, is also gaining, with its stock up more than 50% from December lows.

- Yields on US 10-year Treasuries are rising by nearly 5 basis points to around 4.4%, indicating continued strong demand for safe-haven assets. Higher yields are putting pressure on precious metals, with gold attempting to stabilize after a recent sell-off, but still trading below $4,400 per troy ounce.

- The crypto sector is also under pressure. Despite ETF inflows and stronger spot demand, Bitcoin has fallen below $70,000. Analysts at Bernstein project a potential rise to $150,000 by the end of 2026, driven by increasing demand from institutional investors and corporations.

The release of preliminary US PMI data for March came in weaker than expected, with the overall business sentiment indicator falling to its lowest level in 11 months, following softer data from Europe. While the manufacturing index surprised to the upside, the services sector declined notably.

US Composite PMI (March): 51.4 (Forecast: 51.9; Previous: 51.9)

- Manufacturing PMI: 52.4 (Forecast: 51.5; Previous: 51.6)

- Services PMI: 51.1 (Forecast: 52.0; Previous: 51.7)

March PMI data from the largest euro area economies painted a mixed picture of economic conditions. Germany delivered a positive surprise in manufacturing, but services underperformed, leading to a decline in the composite index. France, meanwhile, saw manufacturing remain just above the neutral threshold, but services and the composite index stayed below 50, signaling ongoing weakness in economic activity.

Eurozone Composite PMI: 50.5 (Forecast: 50.4; Previous: 51.9)

- Manufacturing PMI (S&P Global, March): 51.4 (Forecast: 49.8; Previous: 50.8)

- Services PMI: 50.1 (Forecast: 50.5; Previous: 51.9)

Germany Composite PMI: 51.9 (Forecast: 52.2; Previous: 53.5)

- Manufacturing PMI (March): 51.7 (Forecast: 49.5; Previous: 50.9)

- Services PMI: 51.2 (Forecast: 52.5; Previous: 43.5)

France Composite PMI: 48.3 (Forecast: 49.3; Previous: 49.9)

- Manufacturing PMI (March): 50.2 (Forecast: 49.5; Previous: 50.1)

- Services PMI: 48.3 (Forecast: 49.0; Previous: 49.6)

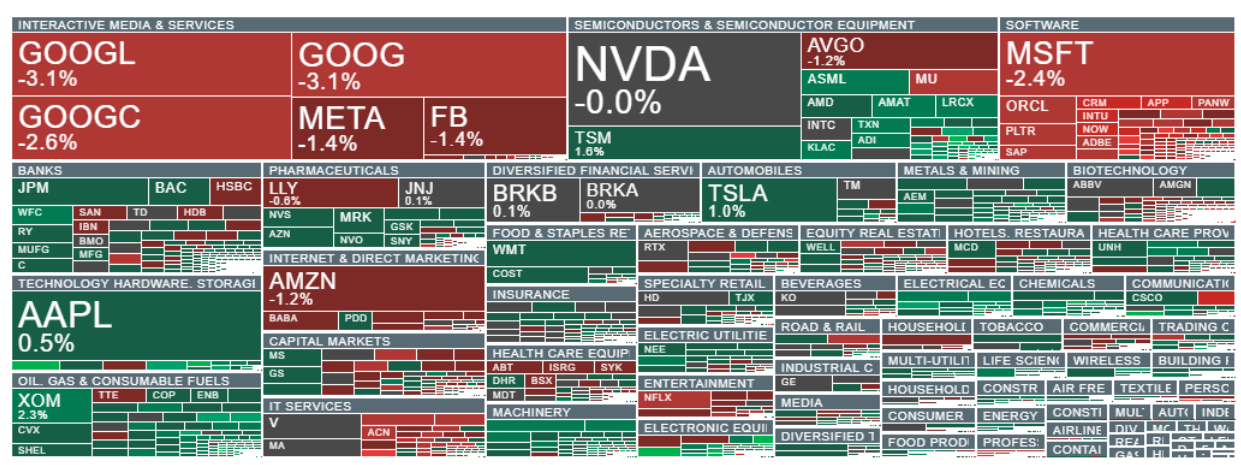

Sentiment is improving today in the semiconductor, electronics, banking, and oil & gas sectors. In contrast, the IT sector is underperforming, with shares of Alphabet (GOOGL.US) and Microsoft (MSFT.US) both down करीब 3%. Source: xStation5

(summary in progress)

Source: xStation5

When will the rise in oil prices reach us?

Daily Summary: Equities Diverge as Tech Lags, Europe Rallies on Earnings & PMIs (24.07.2026)

Three markets to watch next week (24.07.2026)

Oil Slides Ahead of the Weekend!