USD Index (USDIDX) slides 0.5%, resuming downtrend following announced opening of the Strait of Hormuz.

Despite limited volatility at the start of the session, the FX market grew turbulent at the very end of the week in response to a report published by Axios regarding a negotiated 3-page peace plan between Iran and the USA. The announcement by the Iranian Foreign Minister of the full opening of the Strait of Hormuz sealed the deal, deepening the dollar's decline and triggering euphoria across equity markets.

The collapse in oil contracts pulled the dollar down with it, as the greenback surrendered gains accumulated due to geopolitical uncertainty. USDIDX is trading at its lowest level in over 1.5 months, and bearish momentum is confirmed by the EMA10 crossing below the EMA30 and EMA100. The RSI has not yet dropped below the overbought threshold, although the price has stalled at the 61.8% Fibonacci retracement level of the recent upward wave. Source: xStation5

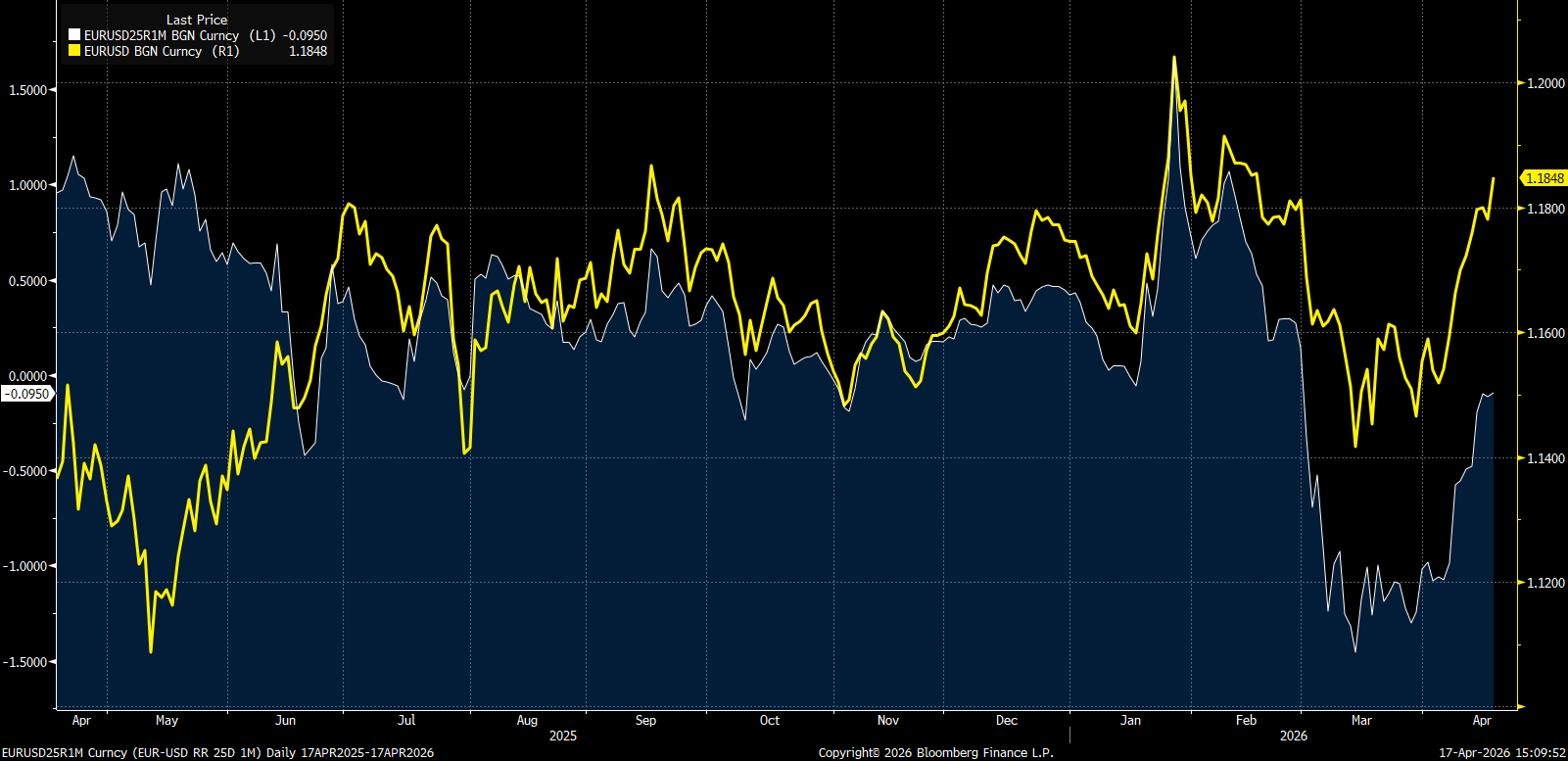

EURUSD at 2-month highs

With the outbreak of the war in Iran, discussions returned regarding potential euro-dollar parity in the event of a sustained stall in the European economic recovery. However, the market quickly priced in a return to normalcy, and EURUSD returned to the offensive shortly after breaking out of a local bottom near 1.1400. Currently, the pair is above 1.18, trading at levels seen before the Middle East conflict when the primary narrative was the market-anticipated return of U.S. interest rate cuts.

Alongside the gains in EURUSD (yellow), we are observing a very strong rebound in the Risk Reversal indicator in the options market (white). In other words, investors have abruptly stopped hedging against EURUSD declines (in this case, for a 1-month period). Source: Bloomberg Finance LP

Central banks return to center stage

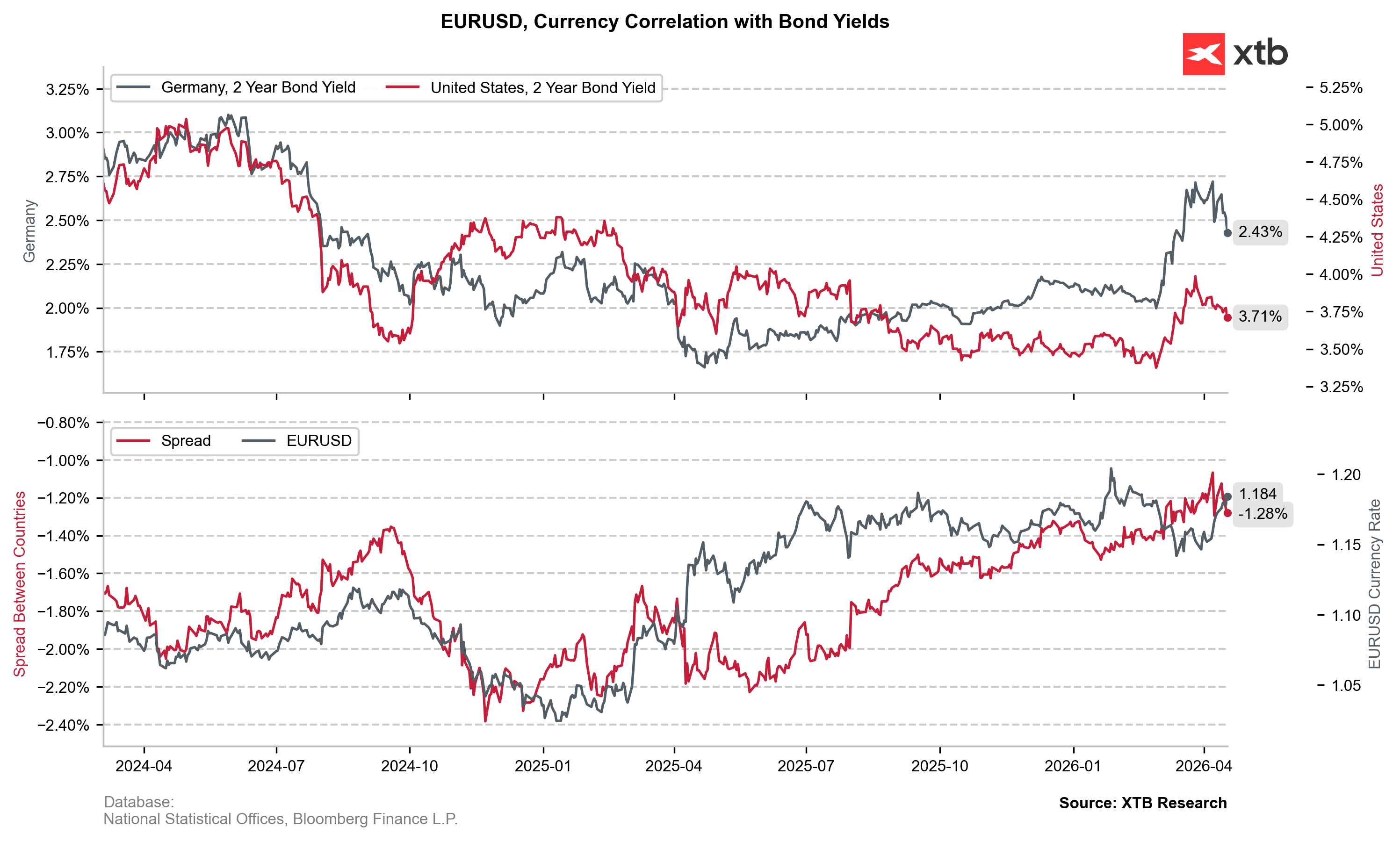

With the gradual de-escalation of the Middle East conflict, monetary policy will once again become the primary driver of volatility in the FX market. For two weeks, we have observed a clear decline in bond yields on both sides of the Atlantic, suggesting that investors have been discounting a decrease in the risk of a long-term surge in energy prices—and thus a global return to rate hikes—for some time. The swap market has already abandoned pricing in U.S. rate hikes, while for the ECB, a 98% chance of a hawkish +25 bps move in July remains. Investor positioning was also bolstered by today’s statements from the ECB's Madis Muller, who "would not rule out a move in April." However, these words were spoken before the opening of the Strait of Hormuz, which should nonetheless explain the pressure on the bond spread between Germany and the US.

The EURUSD rate has effectively caught up with the spread between German and U.S. 2-year yields, which rose consistently despite the geopolitical chaos. While the potential end of the war and the opening of the Strait of Hormuz reduce the risk of rate hikes on both sides of the Atlantic, the ECB should remain relatively more hawkish than the Fed, for which the pre-war scenario involved further rate cuts—and consequently, downward pressure on the dollar. Source: XTB Research

Aleksander Jablonski

Quant Analyst, XTB

Nasdaq Gains 0.6% and Reclaims 29,000 🔼 Strong Results from ON Semiconductor and Palantir

Cocoa Pauses Its Sharp Rally 🚩 Production Concerns in West Africa Return

Chart of the Day: USDJPY After Japan’s Intervention. The Exchange Rate Falls Below 160, but Pressure on the Yen Remains

Economic Calendar: JOLTS Report and Key U.S. Data Take Center Stage