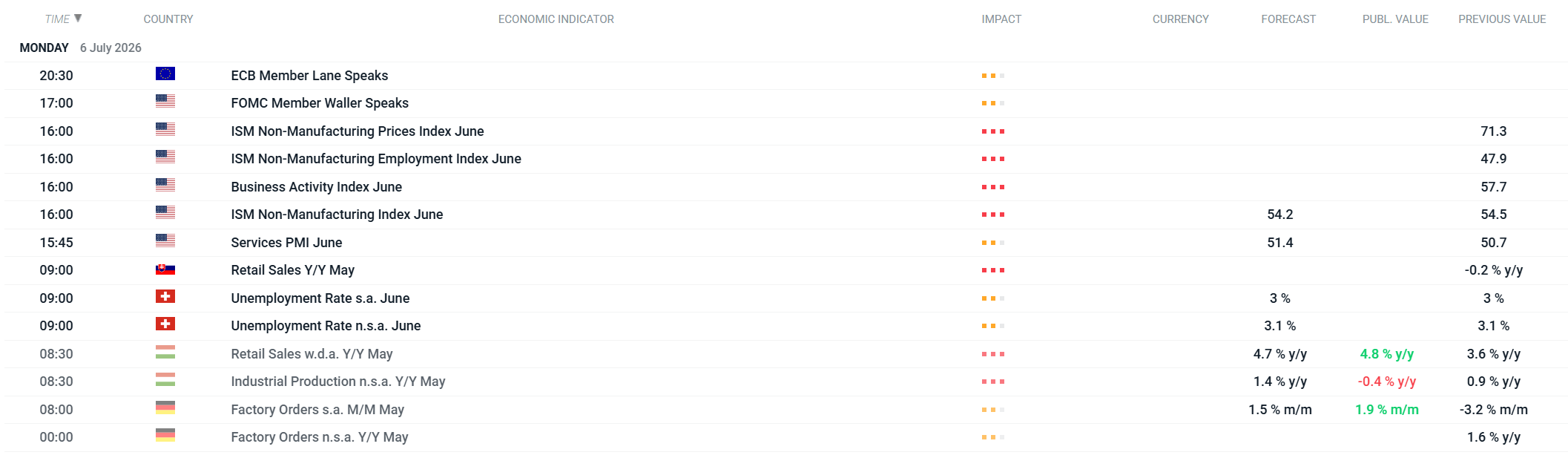

We’re kicking off a new week on the financial markets. This morning’s macroeconomic data has had a limited impact so far: Hungarian retail sales came in better than expected (4.8% y/y vs. 4.7% expected), but Hungarian industrial production came in below expectations (-0.4% y/y vs. 1.4% expected), while German factory orders exceeded forecasts (1.9% m/m vs. 1.5% expected).

This afternoon, market attention will shift to the U.S., where the PMI and ISM PMI data for the services sector for June will be released. The Services PMI (forecast: 51.4) will be released at 3:45 p.m., followed by the key ISM Non-Manufacturing Index (forecast: 54.2, previously 54.5) at 4:00 p.m., along with its components: Business Activity, Employment, and the Prices Index. In the evening, comments from central bank officials—Waller of the Fed (5:00 p.m.) and Lane of the ECB (8:30 p.m.)—are expected, which may influence expectations regarding the future path of interest rates.

Opening of European stock indices

At the start of the trading session, European stock markets are posting slight gains.

-

VSTOXX (volatility index) – +0.60%, signaling a slight increase in market nervousness

-

UK100 +0.23%, NED25 +0.13%, FRA40 +0.10%, SUI20 +0.09%, SPA35 +0.05%, ITA40 +0.04% – modest gains

-

The EU50 (-0.07%) and DE40 (-0.15%) are the only indices in negative territory, though the declines are marginal

Daily Summary: Chip War Weighs on Wall Street as Oil Plunges After US–Iran Ceasefire ⭐

Nasdaq-100 under pressure after chip sell-off

China Is Building Its Own Chip-Making Machines. ASML Under Pressure as the Technology War Enters a New Phase

US Open: Wall Street Rebounds After US Iran Ceasefire