The market remains dominated by the ongoing sell-off in technology stocks and renewed pressure on precious metals, with overall tension expected to rise ahead of today’s high-impact macroeconomic releases.

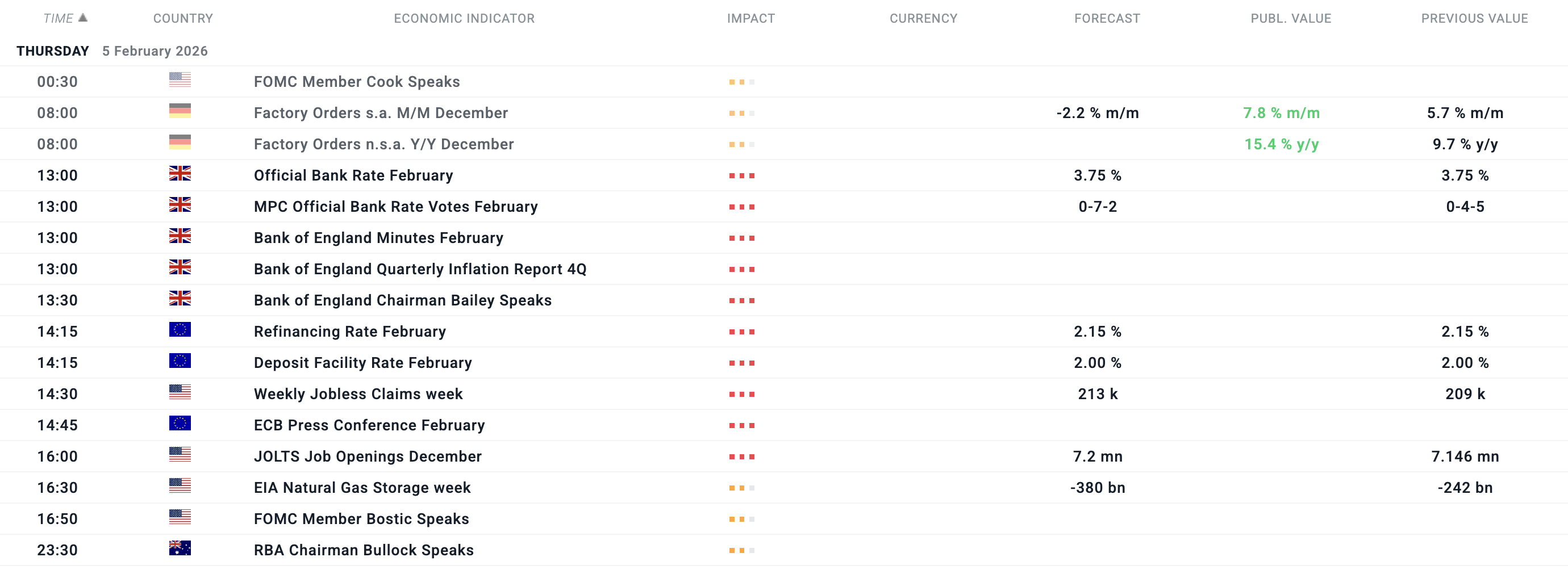

Thursday will be primarily shaped by central bank decisions in Europe. The Bank of England (BoE) will publish its interest rate decision at 12:00 PM GMT, followed by the European Central Bank (ECB) at 1:15 GMT.

While both institutions are expected to keep rates unchanged, the focus will be on the accompanying rhetoric. The BoE may signal a readiness for further cuts in the coming months, whereas the ECB is likely to reaffirm a favorable balance of risks, characterized by inflation reaching its target and gradual, albeit uneven, economic recovery in the Eurozone.

In the U.S., investors await another series of labor market data. Alongside weekly jobless claims, the JOLTS report on job openings will be released. Yesterday’s weaker-than-expected ADP employment report (showing only 22,000 new jobs) set a relatively pessimistic tone; therefore, any further signs of labor market weakness could stall the current gains seen in the U.S. dollar.

Financial results will be presented by companies including: Amazon, Shell, UniCredit, BNP Paribas, Philip Morris.

All times CET (GMT+1). Filtered by US, UK, Eurozone, Germany, France, Japan, Australia, New Zealand, medium and high importance. Source: xStation5

Chart of the Day: USDJPY Rises Again. Intervention Is Not Enough — Markets Await BoJ Action

Economic Calendar: RBA Holds Rates, Markets Await US Housing Data

Morning Wrap: Trump Sets Conditions for Iran. Oil Rises as Hopes for a Quick Reopening of the Strait of Hormuz Fade

Daily Summary: Failure of negotiations in the gulf, oil and gas prices soar