What should we watch for during today's session?

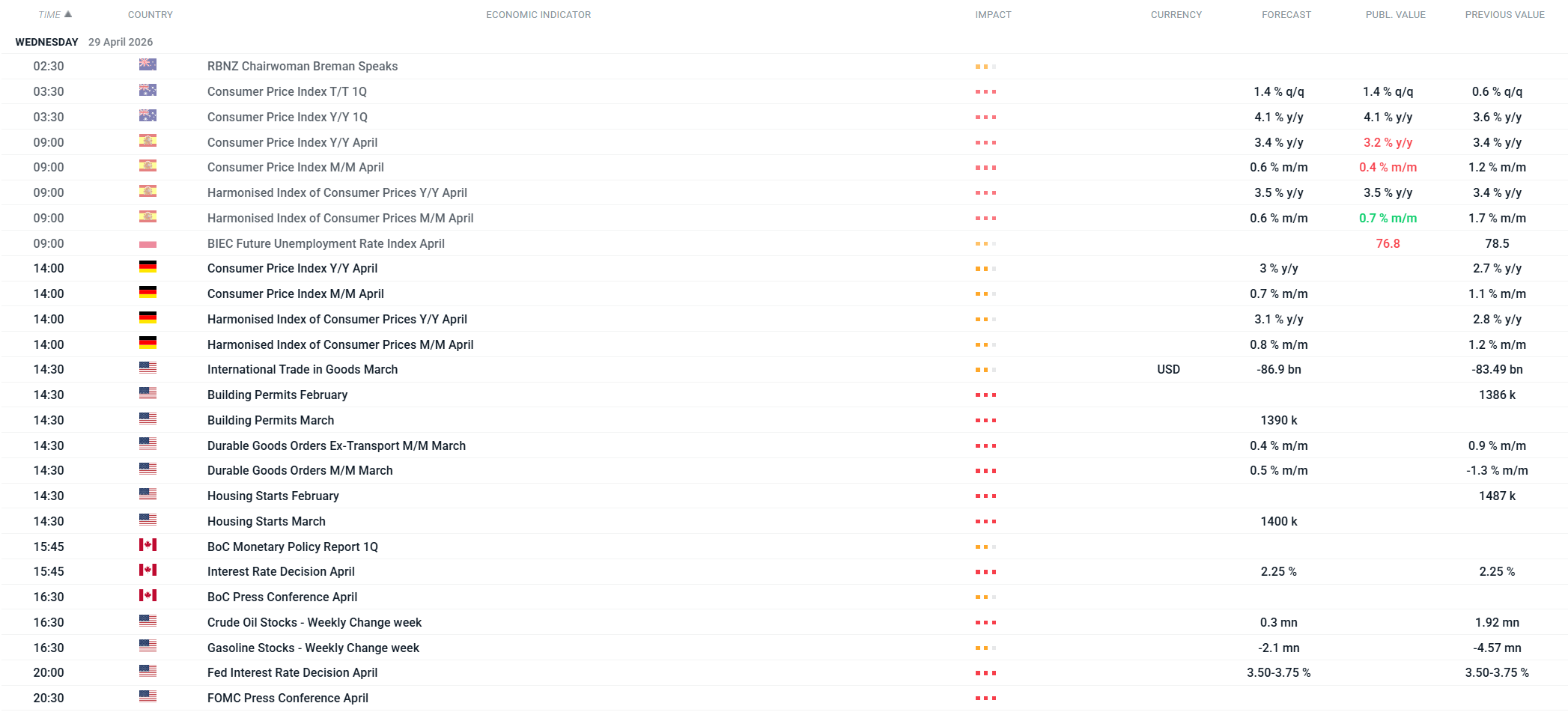

• The key events of the day are the interest rate decisions by the Fed (8:00 p.m.) and the Bank of Canada (3:45 p.m.) – in both cases, rates are expected to remain unchanged, but the press conferences (Powell at 8:30 p.m., BoC at 4:30 p.m.) may provide clues regarding the future path of policy amid elevated energy inflation.

• Data on durable goods orders, building permits, and housing starts in the U.S. (2:30 p.m.) will provide insight into the state of the U.S. real economy. Official EIA data on crude oil inventories will either confirm or refute yesterday’s API report.

• In Europe, attention will focus on inflation data—Germany’s CPI and the HICP—which will show the extent to which the energy crisis is affecting consumer prices in the eurozone. The data may limit the ECB’s room to send any dovish signals.

• Tonight marks the absolute climax of earnings season—as many as four megacaps are set to report after the market closes: Microsoft, Meta Platforms, Alphabet, and Amazon. These are companies with massive weightings in the S&P 500 and Nasdaq indices, whose results could determine the market’s direction for the coming weeks. Investors expect not only earnings to beat forecasts, but also concrete evidence of AI monetization, cloud growth, and sustained profitability amid rising costs. Markets are buying every dip, hoping for further geopolitical concessions, but nothing has changed materially—the lack of new catalysts, with oil above $100 and the Strait of Hormuz closed, poses a real threat to the rally’s continuation.

Today's schedule is shown above. Source: xStation

Daily Summary: Failure of negotiations in the gulf, oil and gas prices soar

FX Weekly: Yen Returns to Losses, Dollar Under Pressure (10.08.2026)

US OPEN: Debt and the Strait of Hormuz fuel growing concerns.

⬆️TTF gas rises over 6% near 58 EUR