European indices open June on a positive note, with Nvidia and Microsoft driving the tech sector. Markets are starting the new month with an appetite for risk, but geopolitical tensions in the Strait of Hormuz are keeping investors on edge.

📊 Launch in Europe

European indices are opening cautiously in positive territory. The biggest gains are being posted by EU50 (+0.43%) and ITA40 (+0.24%) and NED25 (+0.22%). Germany (DE40 +0.18%) and France (FRA40 +0.21%) are up solidly. Slightly in the red are VSTOXX (-0.25%)—the European volatility index—and the Swiss SUI20 (-0.05%) remain slightly in the red, suggesting that the overall mood is moderately bullish, without panic.

🌐 Global Sentiment

A broad view of the markets shows green dominating. Energy commodities are leading the gains: NATGAS +2.56%, OIL.WTI +2.43%, OIL +2.15% – driven by escalating US-Iran tensions and disruptions in the Strait of Hormuz, where the US Navy is escorting only a fraction of normal commercial traffic. Also rising sharply are JP225 (+1.43%) and CHN.cash (+1.16%). US100 +0.61% and US500 +0.33% are signaling that Wall Street is gearing up for new records following a strong May (+8% Nasdaq, +5.2% S&P 500).

📅 Today's Calendar

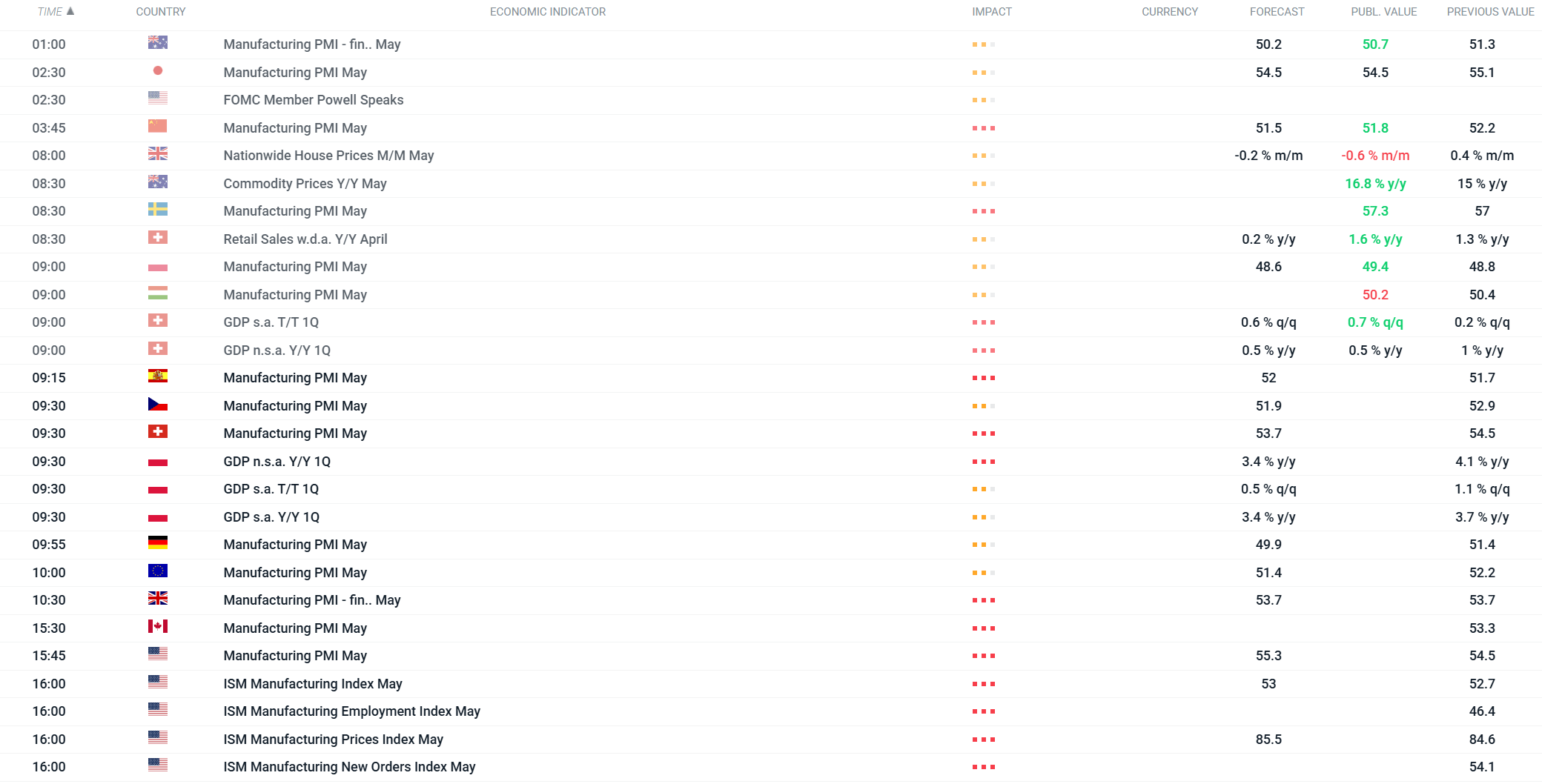

The day will be dominated by a series of Manufacturing PMI readings for May from around the world:

-

China (Caixin) already released: 51.8 (above the forecast of 51.5, previously 52.2) – a slight slowdown, but still in expansionary territory

-

Poland Q1 GDP: at 9:30 a.m. – forecast +3.4% y/y, previous +4.1% y/y – potentially weaker reading

-

Germany Manufacturing PMI at 9:55 a.m. – forecast: 49.9 (below the 50 mark!)

-

Eurozone Manufacturing PMI at 10:00 a.m. – forecast: 51.4

-

U.S. ISM Manufacturing at 4:00 p.m. – forecast 53 vs. previous 52.7 – the key reading of the day

Note: Swiss Q1 GDP, released at 9:00 a.m., came in at +0.7% q/q—above the forecast of 0.6%.

🔑 What drives the market?

-

U.S.–Iran Geopolitics – The Strait of Hormuz remains in "crisis management" mode; oil prices react sharply to every report of attacks

-

COMPUTEX Taipei + Microsoft Build – Jensen Huang (Nvidia) unveils the N1X chip and the RTX Spark superchip; the first ARM-based Windows PCs are coming next week

-

ISM Manufacturing at 4:00 p.m. – the first hard macroeconomic data of the week ahead of Friday’s NFP (forecast: 85,000 jobs)

-

Oil and gas as a geopolitical barometer – WTI nearing $90; any news from the Persian Gulf could trigger a strong reaction

Daily Summary: Wall Street Regains Ground; Another Intervention in the Yen Market❓

Three Markets to Watch Next Week (July 31, 2026)

Market Wrap: European equities at 3-week highs! Apple dips in US premarket!

Euro Area core inflation above estiamtes! EURUSD under key resistance!