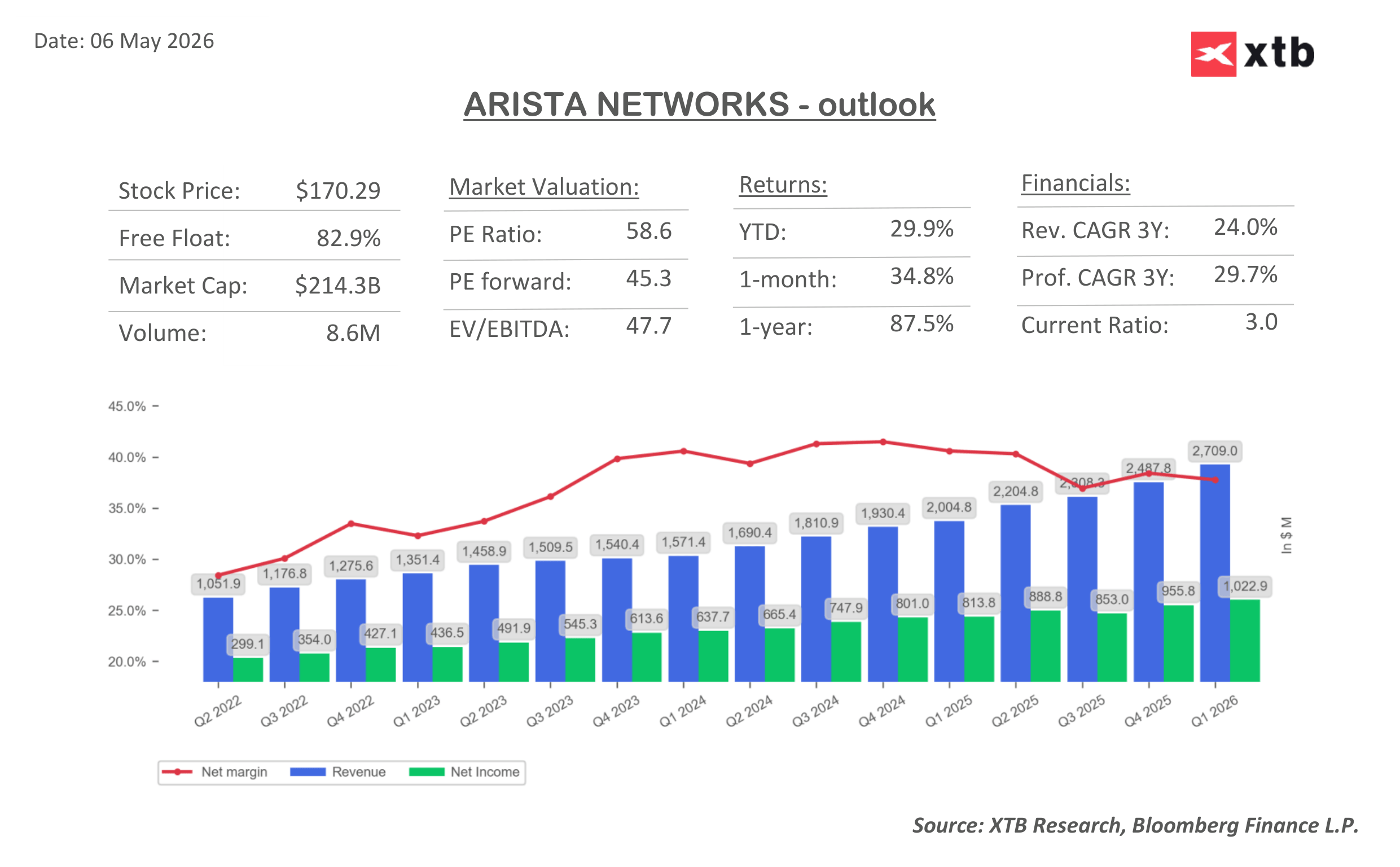

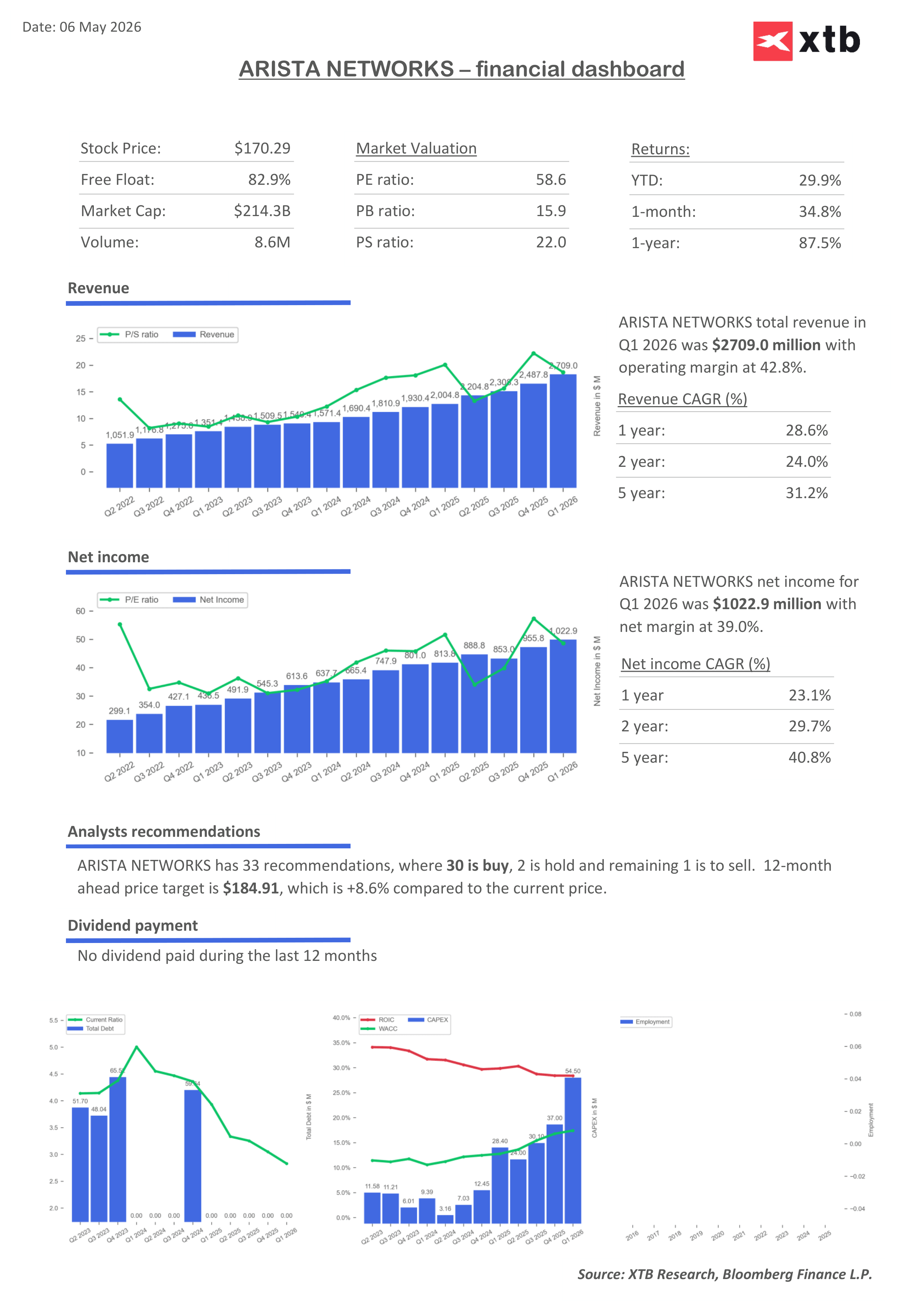

The results of Arista Networks for the first quarter of 2026 illustrate a classic case where “good” is not always “good enough” in the eyes of the market. The company delivered a solid report, beating expectations on both revenue and earnings per share, and additionally raised guidance for the coming quarters. Despite this, investor reaction was clearly muted, and the stock declined after the earnings release.

At first glance, the numbers look strong. Arista continues its rapid growth trajectory, driven primarily by rising demand for data center networking infrastructure and the expansion of AI-driven environments. The company is benefiting from the same structural trend as major semiconductor players, providing a critical infrastructure layer that enables scalable computing power.

Key financial highlights for the first quarter

-

Revenue $2.71 billion versus expectations of around $2.66 billion, up 35.1% year over year

-

Earnings per share $0.87 above consensus of around $0.82

-

Revenue growth approximately 35% year over year driven by data center and AI demand

-

Gross margin 62.4%, slightly below market expectations

-

Operating margin 47.8%

-

Operating cash flow approximately $1.69 billion, reflecting very strong cash generation

Outlook for the next quarter and full year

-

Second-quarter guidance revenue of around $2.8 billion and EPS of around $0.88, both above consensus

-

Raised full-year 2026 outlook revenue of around $11.5 billion, implying approximately 27.7% year-over-year growth

Despite these solid fundamentals, the market reacted negatively. The main reason was margin performance, which came in slightly below expectations. For companies like Arista, even minor deviations in profitability can trigger a notable reaction, especially when investors are accustomed to consistently high-quality execution.

Even more important, however, is the expectations framework. Arista is now viewed as one of the key beneficiaries of the AI boom, which significantly raises the bar. In such cases, a simple earnings beat is often not enough. The market expects results that are not only above consensus, but meaningfully and decisively above it. The raised guidance, while positive in isolation, also failed to deliver the level of upside surprise investors were hoping for.

So how should this report be interpreted? The fundamentals remain very strong. The company is growing rapidly, scaling its operations, and confirming robust demand for its solutions. At the same time, there are early signs of slight margin pressure, which could reflect product mix shifts, continued investment in AI-related technologies, or increasing competition in the most attractive segments of the market.

In a broader context, Arista remains one of the best-positioned players in the data center networking space. Its solutions are essential for enabling and scaling modern AI systems, placing the company directly within one of the most powerful technological trends of this decade.

Ultimately, this is a report that can be described as operationally very strong but underwhelming relative to extremely elevated market expectations. The stock reaction says more about sentiment and positioning than about the underlying health of the business. If growth momentum is sustained and margin pressure proves temporary, the current pullback may represent a reset in expectations rather than a deterioration in fundamentals.

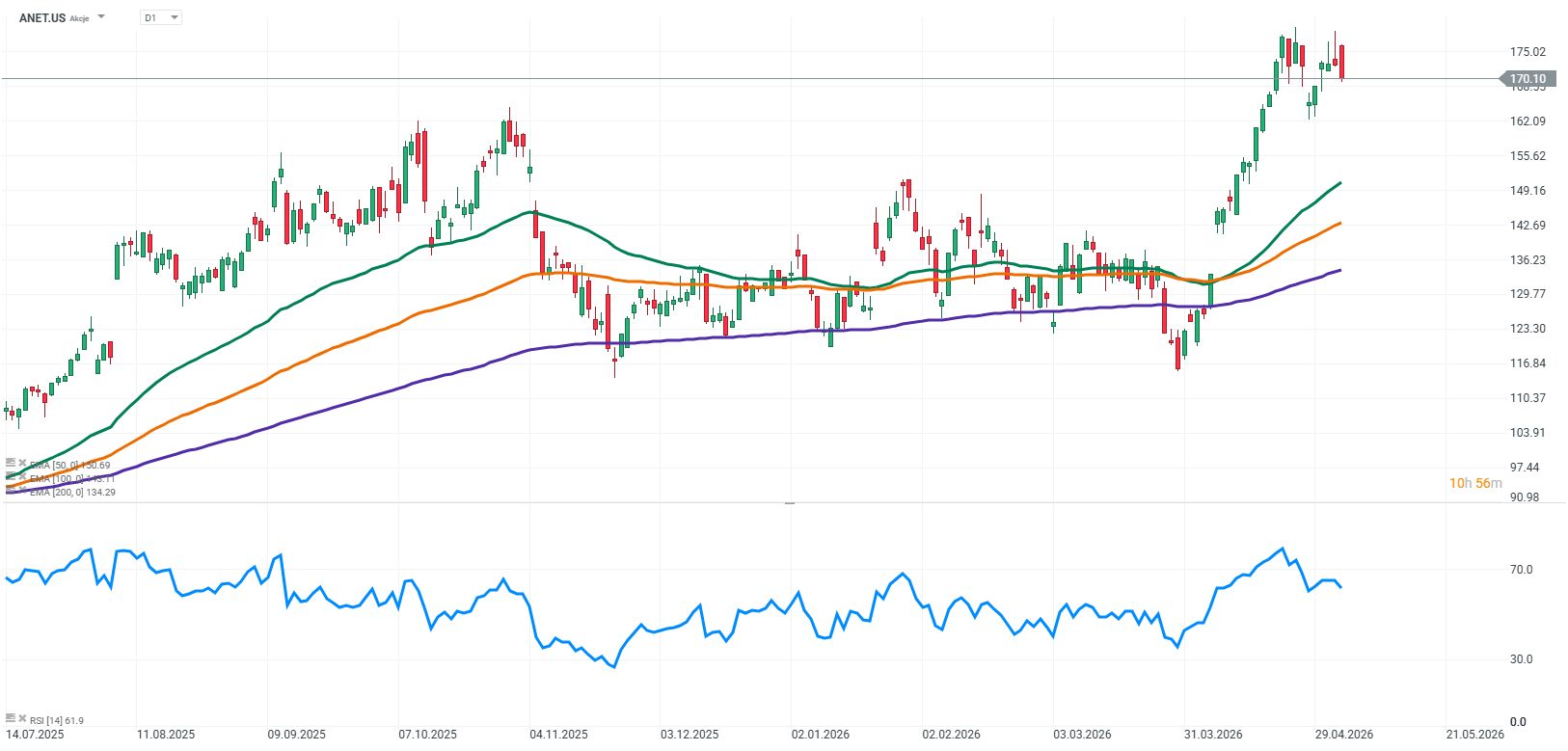

Source: xStation5

ASML sell-out: Dreams and rumors will not break the monopoly

Economic Calendar: PayPal, Visa and Coca-Cola to overshadow macro data (28.07.2026)

Morning Wrap: US halt to attacks balanced by semiconductor sector declines (28.07.2026)

Daily Summary: Chip War Weighs on Wall Street as Oil Plunges After US–Iran Ceasefire ⭐