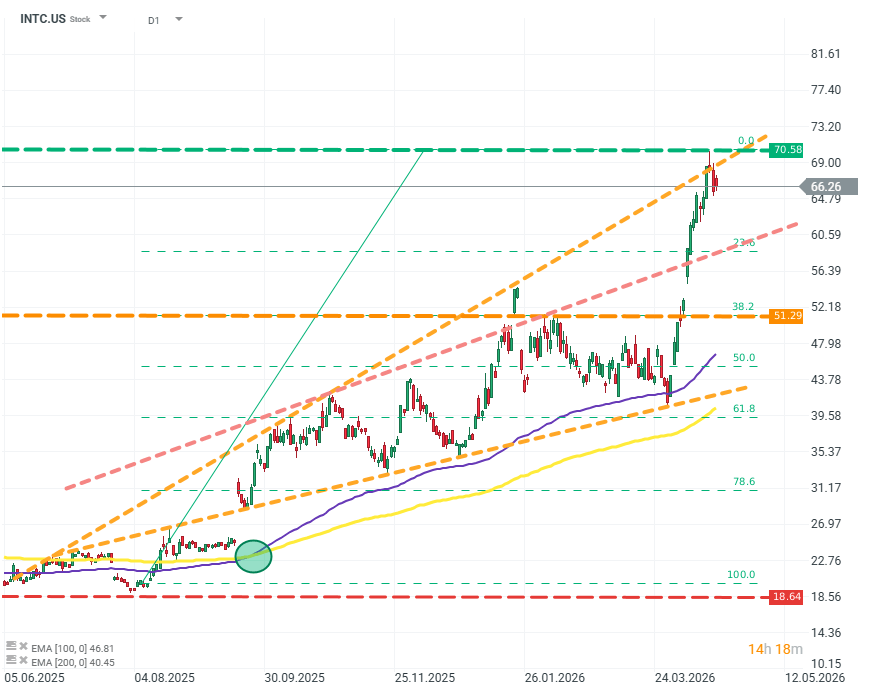

The semiconductor maker’s valuation is currently at its highest level since the Dot-Com bubble, sitting just a few dollars below its all-time high. From the 2024 low, the stock is up more than 250%; this year it has gained nearly 70%, with most of that move occurring in just the last three weeks.

INTL.US (D1)

The latest rally can only be described as hyperbolic: more than 70% in less than a month, despite no fundamental changes to the business model or the broader business environment. The move only stalled around the psychological ~$70 level. Intel has reached valuations at this level only twice in its history - during the dot-com bubble and during the Covid pandemic. Could the stock once again be signaling a late-stage phase of a speculative bubble? Source: xStation5

Is this move, and its magnitude, justified?

Market expectations for the Q1 2026 results appear relatively conservative compared with the stock’s behavior:

- Revenue: above USD 13.3 billion

- EBITDA: ~USD 3.25 billion

- EBIT: ~USD 420 million

- Adj. EPS: around 0

It’s worth noting these figures imply a year-over-year decline. If so, what could be driving market sentiment and the outsized gains?

The key areas investors are watching right now are the Data Center/AI segment and the “Intel Foundry” initiative.

While Data Center and AI account for only about 30% of company revenue, they generate most, if not all, of net income. The bulk of Intel’s revenue still comes from servers and PCs, but the margin profile of that segment is currently around 2%.

Intel Foundry, meanwhile, is still loss-making. Intel Foundry is a broad initiative aimed at providing chip “packaging” services - one of the major bottlenecks in the semiconductor industry and a pillar of Intel’s long-term growth ambitions.

The key word here is “long-term.” Even though Intel Foundry generates over USD 4 billion in revenue, it is effectively more than USD 2 billion in the red, and due to technical constraints, that is unlikely to change for at least the next 4–6 quarters.

Given this, the only way the recent Intel rally would be justified is if we see:

- (Even) higher margins in the Data Center/AI segment

- Raised guidance

- Announcement of a major, not-yet-public new contract

Otherwise, it is difficult to justify current valuations for a company with only a few remaining chances, a long list of problems, and profitability close to zero relative to its scale.

Did SaaS lost too much? Morgan Stanley says yes.

US OPEN: The market extends losses as investor concerns grow

Daily Summary: Lower inflation weakens the dollar and awakens gold and S&P 500 to gains

Worse than the Dot-com bubble: IBM stock crash