European equities opened Friday’s session with notable gains, rebounding after earlier declines driven by growing concerns over the impact of the Middle East conflict on energy markets and inflation. The pan-European Stoxx 600 index, along with key indices in Germany, France, and the UK, are rising as investor sentiment improves following statements from the United States aimed at calming markets after a wave of sell-offs, partly triggered by higher energy commodity prices. At the same time, European natural gas prices remain under pressure, rising amid the escalation of the conflict and the risk of supply disruptions. Markets are closely monitoring potential supply constraints and the implications for energy costs and inflation, which continue to affect sentiment toward riskier assets.

Oil prices are gaining, hovering around USD 110 per barrel.

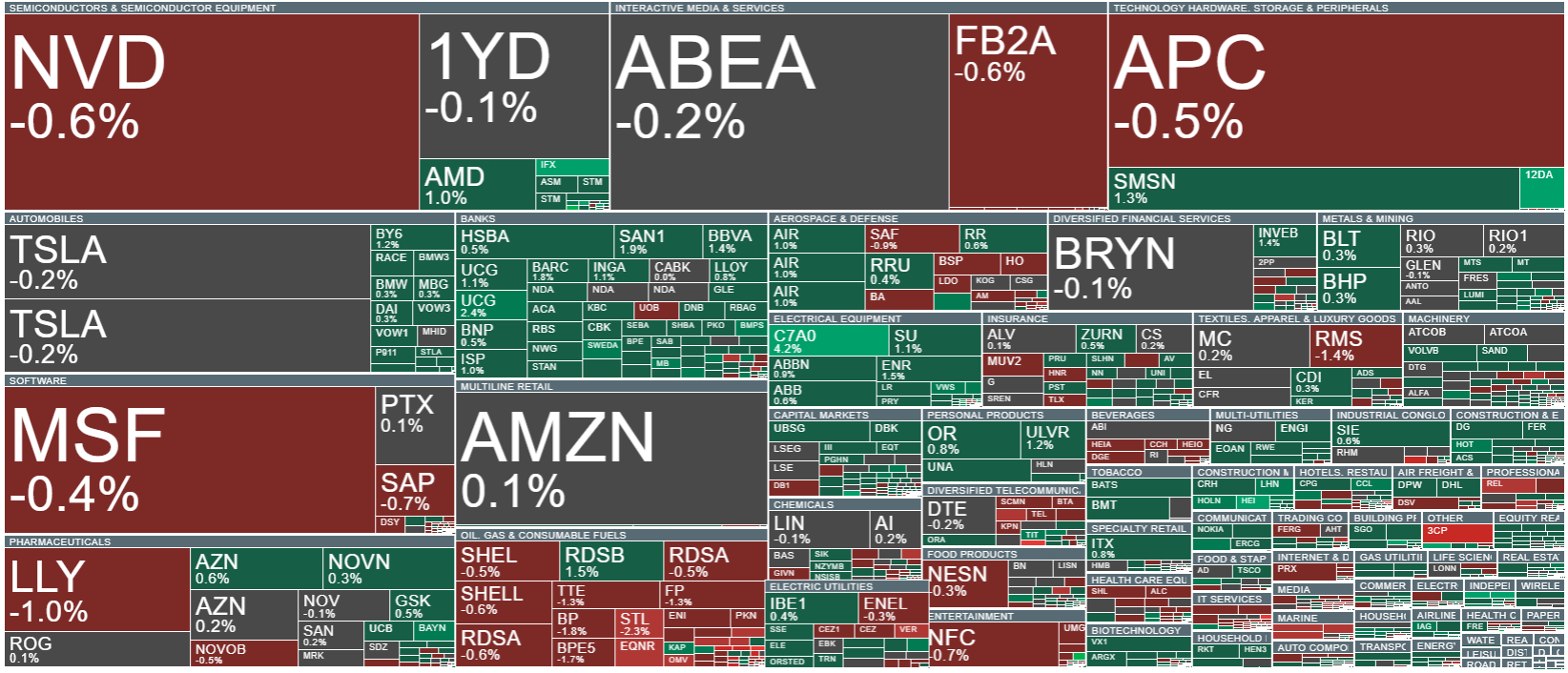

Volatility is currently visible across sectors in Europe. Source: xStation

Key macroeconomic releases from selected European countries today:

Germany – Producer Price Index (PPI), February

-

Month-on-month (m/m): -0.5% vs forecast 0.3% and previous -0.6%

The producer price index fell by 0.5% in February, exceeding the forecasted decline and closely matching the previous month. This suggests that cost pressures at the production level remain limited.

-

Year-on-year (y/y): -3.3% vs forecast -2.7% and previous -3.0%

The annual PPI decline deepened, indicating a clear reduction in production costs compared to last year. This may influence future monetary policy decisions and inflation sentiment in the eurozone.

Poland – BIEC Well-Being Indicator, March

-

Value: 95.4 vs previous 95.6

The indicator recorded a slight decline, signaling stabilization, though the modest decrease could point to a minor weakening of consumer sentiment in the country.

Eurozone – Balance of Payments, January

-

Current account balance (n.s.a.): EUR 13 bn vs previous EUR 34.6 bn

A notable decrease in the current account balance may reflect a reduced trade surplus or increased import flows.

-

Current account balance (s.a.): EUR 37.9 bn vs forecast EUR 17.2 bn and previous EUR 14.6 bn

Seasonally adjusted data show a significantly higher balance than forecast, which could be a positive signal for eurozone stability, although non-adjusted figures suggest the effect is partly seasonal.

Italy – Foreign Trade Balance, January

-

Balance: EUR 1.09 bn vs forecast EUR 5.6 bn and previous EUR 5.99 bn

The trade balance came in well below expectations, potentially indicating higher imports or lower exports. This could temporarily weigh on Italy’s economic growth outlook.

Futures on European indices are rebounding after recent declines, although the scale of the recovery has been somewhat limited since the morning. Source: xStation

Economic Calendar: Time for Tesla and Google Earnings (22.07.2026)

Morning Wrap: AI companies and gold back in favour? (22.07.2026)

Daily Summary: Semiconductors Rise in the Shadow of Geopolitical Turmoil

Tech sector catches its breath 🚀