Stoxx Europe 600 futures are rising more than 0.2%, with European equities extending positive momentum after record highs on Wall Street, fresh peaks across Asian markets, and a sharp decline in oil prices below $100 per barrel amid expectations of a potential agreement between the United States and Iran.

Eurozone retail sales declined by 0.1% month-over-month, compared to market expectations for a 0.3% decline; the previous reading stood at -0.2%. On an annual basis, retail sales increased by 1.2%, in line with consensus forecasts, although below the prior reading of 1.7%.

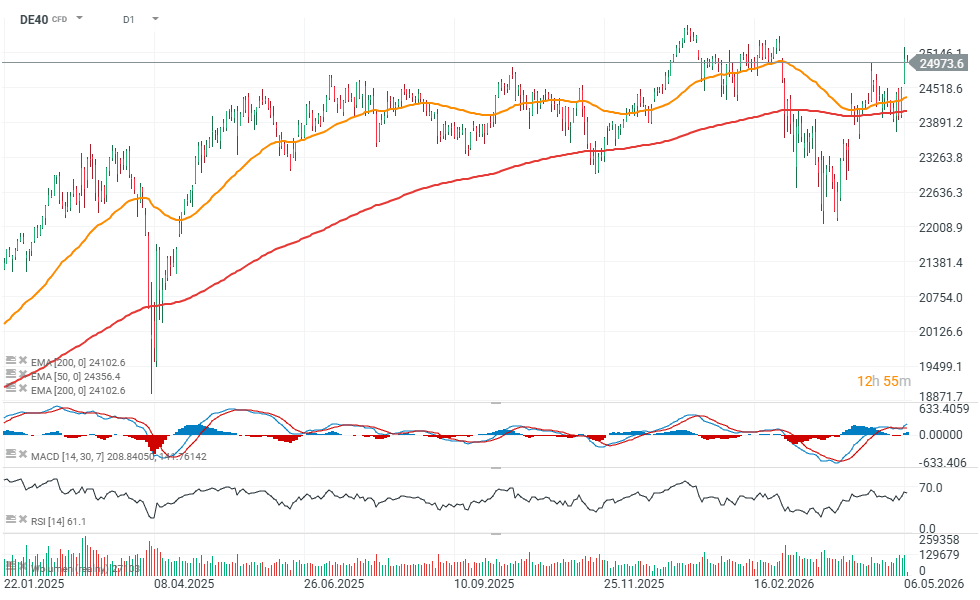

Global markets are also seeing a weaker US dollar and lower bond yields, supporting equities, precious metals, and Bitcoin. In Europe, Germany’s DAX is underperforming relative to the broader market, slipping around 0.1% despite the generally positive sentiment across the region.

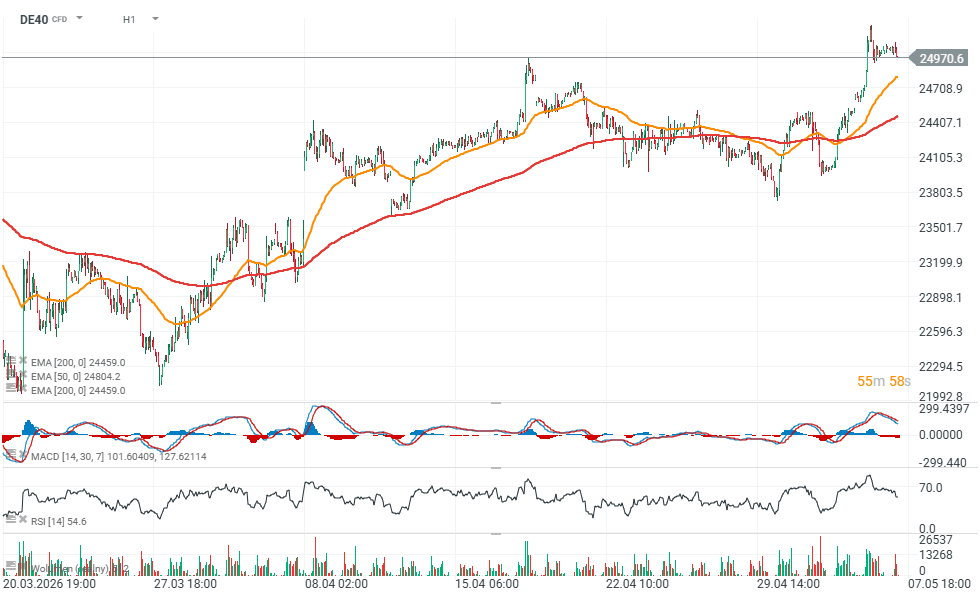

DAX (DE40) futures chart, D1 / H1 interval

Source: xStation5

Source: xStation5

Corporate earnings support sentiment across European markets

- Qiagen reported adjusted EPS of 54 cents, in line with analyst expectations.

- Lottomatica generated revenue of €600 million and stated that it expects 2026 adjusted EBITDA to come in at the upper end of previously issued guidance.

- Tenaris posted sales of $3.10 billion, beating market expectations of $2.99 billion.

- Endesa reported net profit of €725 million versus analyst estimates of €627.6 million.

- Jeronimo Martins posted EBITDA of €572 million, above consensus forecasts of €560.6 million.

- Banco Comercial Portugues reported net profit of €305.8 million, significantly above expectations of €283.4 million.

Elevated volatility across European equities following earnings releases

- Prosus gained around 3%, making it one of the strongest performers in the Stoxx Europe 600, while Henkel rose about 2% after reporting better-than-expected first-quarter organic sales growth.

- CSG NV advanced 1.7% and BE Semiconductor Industries climbed 1.6% amid continued optimism surrounding the semiconductor sector; STMicroelectronics also traded higher, gaining around 1.4%.

- Argenx rose 1.5% after reporting Vyvgart sales above analyst expectations.

- TUI and Lufthansa both added around 1%, supported by improving sentiment in the travel and airline sectors as oil prices declined.

- Prysmian gained 0.8% after comments suggesting an extended growth runway driven by data center investments and expansion in the US market.

- RENK Group fell around 1%, alongside BP, Novo Nordisk, Voestalpine, and Nokia, which were also under pressure ahead of the European open.

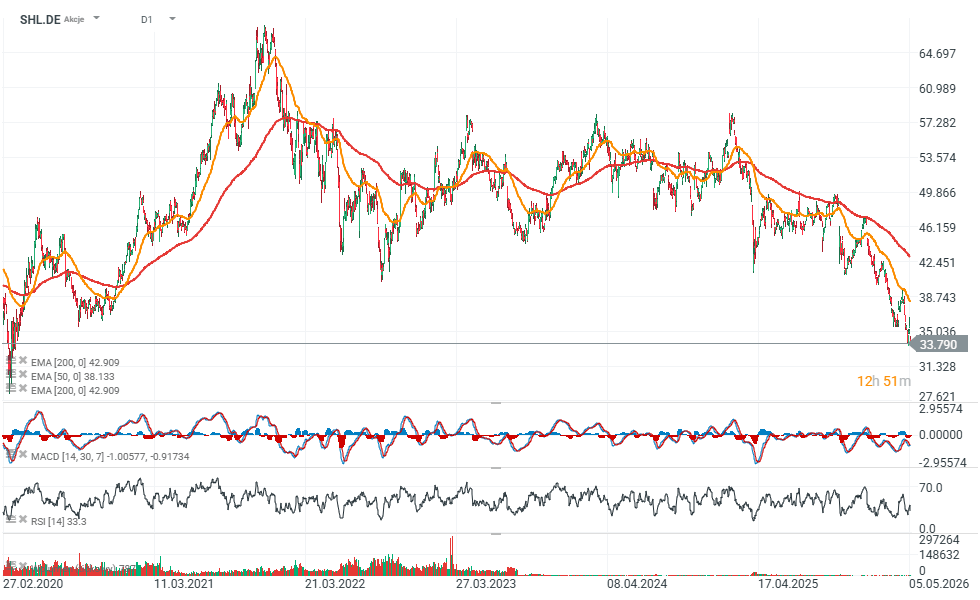

- Aumovio declined 1.7% despite reporting adjusted EBIT of €106 million versus expectations of €93 million, while Siemens Healthineers dropped nearly 5% after cutting its comparable sales growth outlook for the full fiscal year.

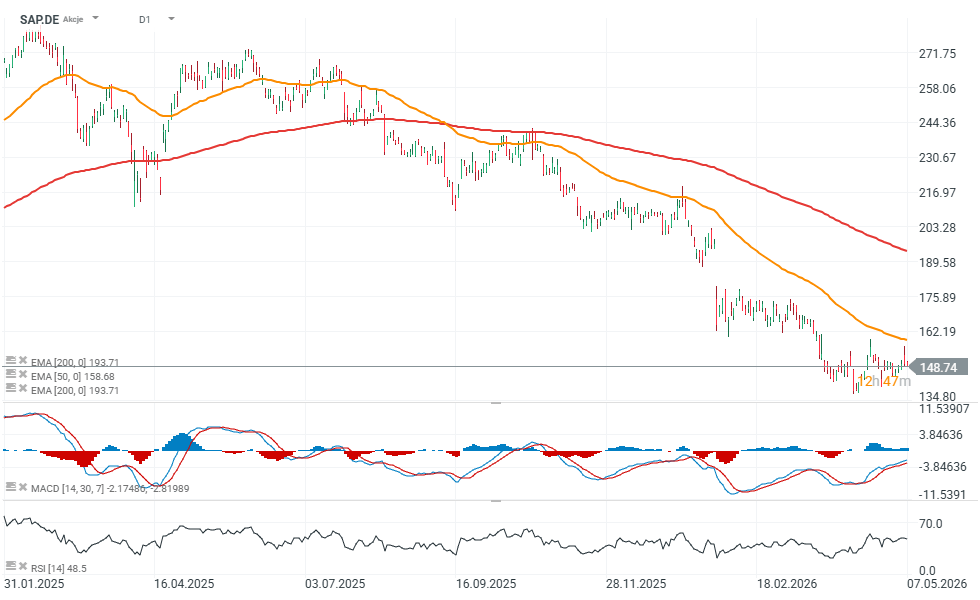

- SAP and OMV fell around 1.1%, while Andritz lost 1.3% following mixed earnings results.

SAP chart (D1 interval)

Source: xStation5

European companies continue to beat market expectations

- Flutter Entertainment reported revenue of $4.30 billion, above market expectations of $4.24 billion.

- AMS-Osram posted quarterly revenue of €796 million versus consensus estimates of €774.3 million.

- Aker BP reported pre-tax profit of $2.72 billion, significantly above forecasts of $1.89 billion.

- Avolta recorded organic revenue growth of 4.7%, exceeding analyst expectations of 4.55%.

- Sanoma posted second-quarter revenue of €221.1 million, above consensus estimates of €215 million.

- BNP Paribas Bank Polska reported net profit of PLN 375.3 million, well above expectations of PLN 306.5 million.

- Swiss Re delivered second-quarter net income of $1.51 billion versus forecasts of $1.19 billion.

- GN Store Nord maintained its full-year organic revenue growth guidance of 0–6% and EBITA margin guidance of 8–9%, compared to 7.6% achieved in 2025.

- Siemens Healthineers lowered its full-year comparable sales growth forecast to 4.5–5% from the previous 5–6% range, while the market had expected approximately 4.94%.

Siemens Healthineers stock chart (D1 interval)

Source: xStation5

- Nexi reported first-quarter revenue of €821.4 million versus expectations of €814.5 million.

- Lanxess reported first-quarter sales of €1.38 billion, compared to market expectations of €1.40 billion.

- Knorr-Bremse posted first-quarter EBIT of €245 million, slightly above consensus estimates of €244.8 million.

- Pharming reported quarterly revenue of $72.4 million; the market compared the result with $79.1 million achieved a year earlier.

- Vonovia reported adjusted first-quarter EBITDA of €711.6 million, above analyst expectations of €701.9 million.

- SAF-Holland posted adjusted first-quarter EBIT of €42.5 million, beating consensus forecasts of €41.6 million.

- Zealand Pharma reported a first-quarter net loss of DKK 43.94 million versus expected losses of DKK 68 million.

- Wacker Neuson posted first-quarter EBIT of €41.5 million, significantly above analyst expectations of €12.1 million.

- Solvay reported underlying first-quarter EBITA of €219 million versus market expectations of €228 million.

- Intrum reported adjusted first-quarter EBIT of SEK 50.1 million, well above expectations of SEK 17 million.

- FinecoBank posted first-quarter net profit of €162.2 million versus forecasts of €158 million.

- Veidekke reported quarterly revenue of NOK 965 million, above analyst expectations of NOK 895 million.

- Legrand reported organic revenue growth of 9.3%, significantly above market expectations of 6.81%.

- Davide Campari posted organic revenue growth of 2.9%, while analysts had expected a 5% decline; despite the strong results, cautious forward guidance triggered a sharp selloff in the stock.

Campari chart (D1 interval)

Source: xStation5

EU50 and OIL charts (D1 interval)

Source: xStation5

Source: xStation5

SpaceX Preview: It's Time to See How Much of Its Valuation Is Based on Business and How Much on Promise

BREAKING: US ISM Manufacturing - Strong Beat Across the Board

Eurozone PMIs: German Factory Revival Masks Underlying Stagnation 🇪🇺

Wall Street rebounds as Q2 earnings season significantly exceeds investors expectations