Microsoft (MSFT.US), along with Meta Platforms, will join the "Magnificent Seven" group of companies today, publishing their latest quarterly results. Microsoft, which has a shifted fiscal year compared to the calendar year, will present its Q4 2024/25 results today after the market closes. Investor attention will primarily focus on the dynamics of the cloud segment, management's comments on the further development of Copilot, the potential impact of large-scale layoffs on margins, and the company's development plans in the new reality of increased tariffs.

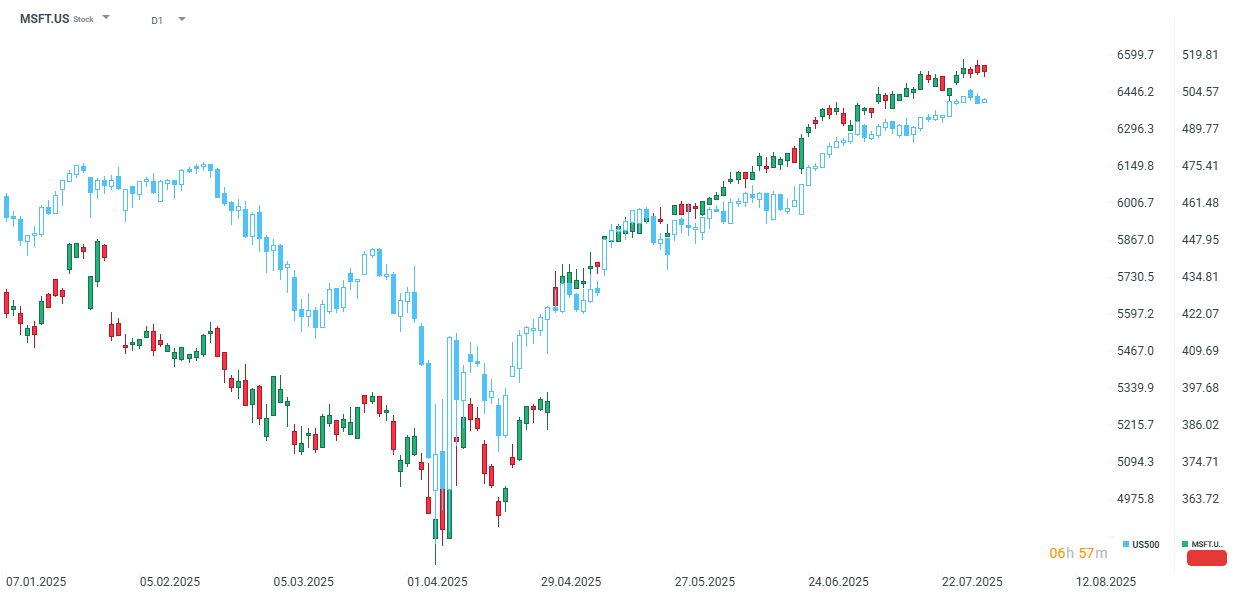

The company has been performing significantly better than the broader index. YTD Microsoft has risen by 22%, while the broader market has grown by approximately 9%. Source: xStation

Cloud Segment remains key

For Microsoft's results, one of the key aspects investors will be watching is the cloud segment. Microsoft, second only to Amazon's AWS, remains a key player in this segment, with Azure revenues being the most dynamic part of the company's results. In light of the AI revolution we are currently witnessing, cloud segment revenues are most likely to contribute significantly to the rapid growth of the company's results.

Since Q1 2023/24, Microsoft's year-on-year revenue growth in this segment has consistently remained above 30% (with the exception of Q4 2023/24, when the rate dropped to 29%). This means that Microsoft not only achieves higher revenues in this segment than, for example, its competitor Alphabet, but also maintains a higher growth rate. Hence, this is an area for Microsoft to deepen its advantage over other companies. Therefore, this segment will be particularly closely watched by investors. The current consensus forecasts a 34% year-on-year increase, which would be the highest rate since Q1 2022/23. With the increasing share of cloud revenues in the company's total revenues (estimated share for Q4 2024/25 is 39% compared to 35% two years ago), maintaining high dynamics in this segment becomes a condition driving Microsoft's growing valuation.

Looking at the consensus sentiment towards Microsoft's prospects, we see a stable level of forecasts over the last four weeks. The consensus predicts an adjusted earnings per share of $3.37, which translates to a 14.3% year-on-year increase. Thus, the projected growth is expected to be higher than that of its competitors.

Total revenues are expected to show weaker dynamics than competitors, with a projected value of $73.89 billion (of which the Intelligent Cloud segment is expected to account for $29.1 billion).

Over the last eight quarters, the company has consistently exceeded consensus expectations, so it is likely that investors have also factored in an "earnings beat premium" in the weeks leading up to the results release.

Earnings estimates. Source: Bloomberg Finance L.P.

Estimated Results for Q4 2024/25

-

Estimated Revenue: $73.89 billion USD

-

Estimated Microsoft Cloud Revenue: $45.96 billion USD

-

Estimated Intelligent Cloud Revenue: $29.1 billion USD

-

Estimated Azure and other cloud services revenue growth (excluding currency effects): +34.2%

-

-

Estimated Productivity and Business Processes Revenue: $32.15 billion USD

-

Estimated More Personal Computing Revenue: $12.67 billion USD

-

Estimated Earnings Per Share (EPS): $3.37 USD

-

Estimated Adj. Earnings Per Share (EPS): $3.37 USD

-

Estimated Operating Income: $32.14 billion USD

-

Estimated Capital Expenditures (CapEx): $17.89 billion USD

-

Estimated Capital Expenditures (CapEx) including finance lease additions: $23.17 billion USD

-

Estimated Revenue at Constant Currency: +13.3%

-

Estimated Azure growth attributable to Artificial Intelligence: 17.25%

Q1 2025/26 Forecasts

-

Estimated Capital Expenditures (CapEx): $18.08 billion USD

-

Estimated Capital Expenditures (CapEx) including finance lease additions: $24.21 billion USD

2025/26 Forecasts

-

Estimated Capital Expenditures (CapEx): $73.93 billion USD

-

Estimated Capital Expenditures (CapEx) including finance lease additions: $100.63 billion USD

Copilot adoption vs its effectiveness

Management remains highly optimistic about the development of the Copilot service, which is one of the most dynamically growing solutions introduced by the company in recent years. Recent statements by Microsoft's CFO indicated a threefold increase in customers within just one year. Of course, as with any new technology, such dynamic growth still contains a low-base effect, but management remains strongly positive about the new AI tool.

The problem with Microsoft's proposed solution lies in its effectiveness. According to Mensa Norway IQ test results, Microsoft's model is not only weaker than the average human IQ (defined as 100 in the test) but also significantly weaker than other models (including OpenAI o3, Gemini, Grok, and DeepSeek).

In such a case, the desire to use Microsoft's service may primarily be based on its compatibility with the entire ecosystem offered by the company. However, if management wants to maintain Copilot as another engine driving results, investors will need to hear information regarding planned technological advancements.

Impact of Large-Scale Layoffs on Results

Since the beginning of 2025, Microsoft has continued its cost-cutting plan through significant layoffs, which reached 6,300 in Q4 2024/25 alone, and another "wave" in July saw 9,000 layoffs. Therefore, a potential increase in planned expenditures for artificial intelligence development may be offset by lower salary costs. Such a prospect opens the way for a potential strengthening of the company's margin, which, in light of an extended valuation, could provide a solid basis for further increases in the company's share price.

Valuation Before Results

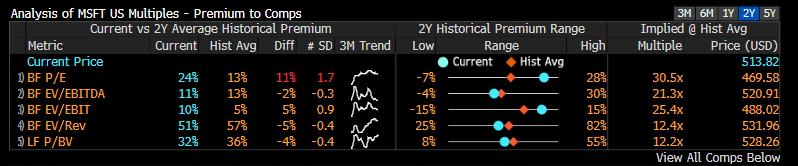

Compared to Alphabet, Microsoft can no longer boast such a comfortable valuation. The company, compared to its two-year averages, remains at elevated values in all key fundamental multiples, except for forward P/BV, where it remains close to its two-year averages.

Comparing the multiples to other companies in the "Magnificent Seven," we can see that, based on forward multiples, the company remains at significantly higher levels than the rest of the companies. The P/E ratio stands out in particular, where the company is trading at a 24% higher level than the other six companies. Over the last two years, the company has traded at an average of 13% higher levels. Thus, it is clear that for Microsoft, strengthening the company's profitability will be particularly crucial.

Among all companies in the "Magnificent Seven," only Nvidia and Tesla are currently trading at higher multiple levels than Microsoft.

Microsoft valuation compared to the valuations of the "Magnificent Seven" stocks. Source: Bloomberg Finance L.P.

Economic Calendar: PayPal, Visa and Coca-Cola to overshadow macro data (28.07.2026)

Morning Wrap: US halt to attacks balanced by semiconductor sector declines (28.07.2026)

Daily Summary: Chip War Weighs on Wall Street as Oil Plunges After US–Iran Ceasefire ⭐

Nasdaq-100 under pressure after chip sell-off