-

End of exclusivity: Microsoft and OpenAI are loosening ties; OpenAI can now partner with rivals (Amazon, Oracle), while Microsoft cuts revenue-share fees to diversify its AI portfolio (e.g., via Anthropic).

-

Infrastructure bottleneck: Azure’s main hurdle is the GPU shortage. The market will track if cloud growth can stay strong despite supply constraints and massive capex (the "Nvidia tax").

-

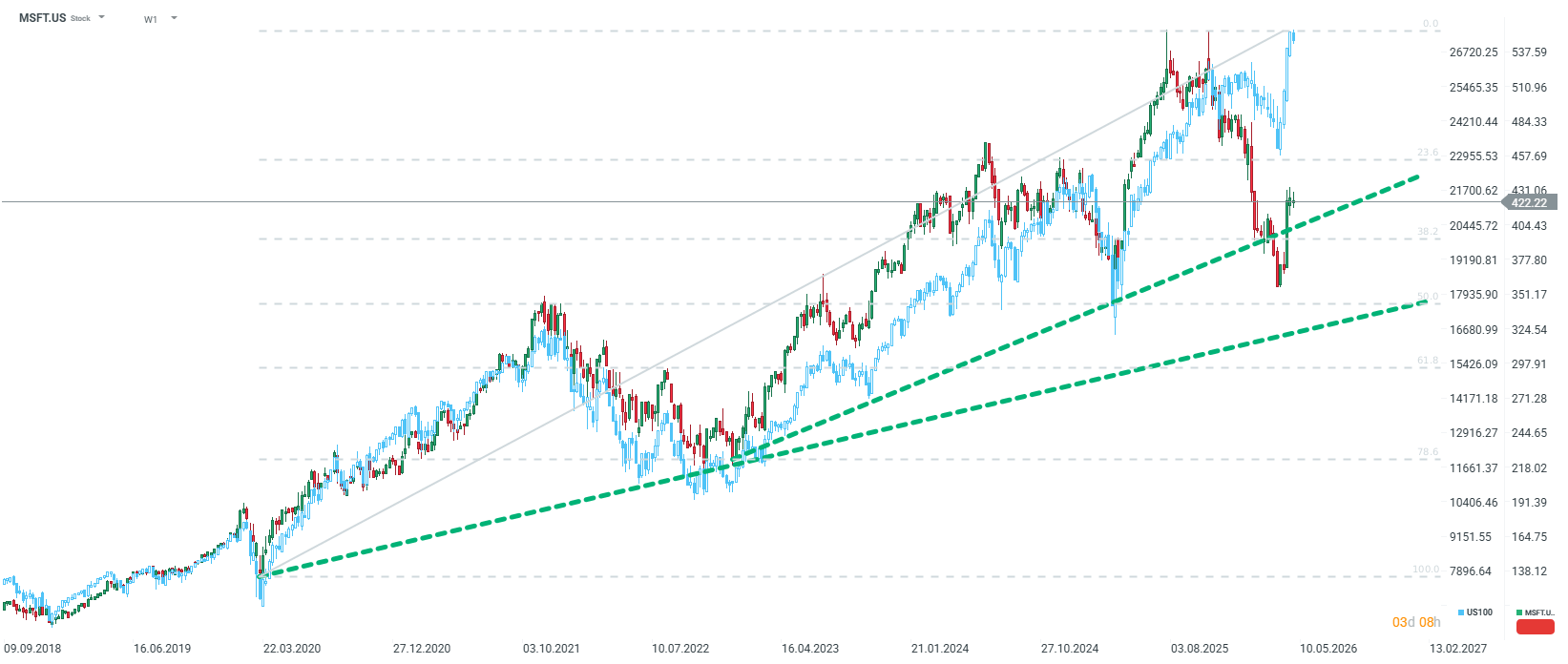

Valuation opportunity: Following a 20% correction, Microsoft’s valuation is attractive (Forward P/E ~21x). With $90bn in cash, current levels offer a compelling entry point for long-term investors.

-

End of exclusivity: Microsoft and OpenAI are loosening ties; OpenAI can now partner with rivals (Amazon, Oracle), while Microsoft cuts revenue-share fees to diversify its AI portfolio (e.g., via Anthropic).

-

Infrastructure bottleneck: Azure’s main hurdle is the GPU shortage. The market will track if cloud growth can stay strong despite supply constraints and massive capex (the "Nvidia tax").

-

Valuation opportunity: Following a 20% correction, Microsoft’s valuation is attractive (Forward P/E ~21x). With $90bn in cash, current levels offer a compelling entry point for long-term investors.

Following today's Fed decision, Wall Street is bracing for an intense after-hours session. No fewer than four "Magnificent 7" companies are set to publish their quarterly financial results. While it is difficult to rank one company above another, many eyes will turn toward Redmond—the home of the world’s largest software company, Microsoft.

For the company led by Satya Nadella, this is no ordinary quarter. After a period of euphoria surrounding Artificial Intelligence, the market is entering a "Show-Me" phase, where promises alone no longer suffice. The share price, currently in a roughly 20% correction from its peaks, suggests that investors have doubted Microsoft’s position as a primary driver of the AI revolution. Nevertheless, the tide has begun to turn in recent weeks. What should we focus on in the upcoming report, and does the company have a chance to reclaim its throne?

1. Cloud and Azure: The Key Growth Engine Facing Supply Constraints

Cloud computing remains the heart of Microsoft’s valuation. Market consensus expects revenue growth in the Intelligent Cloud segment at high-20% or low-30% levels. HSBC analysts are even more optimistic, forecasting a compound annual growth rate (CAGR) for Azure of 33.6% through 2030.

However, the primary issue is not a lack of demand but infrastructure constraints. Microsoft is struggling with a shortage of computing power (GPUs), forcing management into difficult allocation choices. Currently, priority is given to first-party products (M365 Copilot, GitHub Copilot) and R&D, while external Azure customers are left with the "leftovers." If Azure fails to show acceleration this quarter while AWS and Google Cloud (GCP) do, it may be interpreted as a loss of leadership to competitors with their own, more efficient silicon. On the other hand, projections suggest that Azure could surpass AWS as the market share leader by the end of calendar 2026.

2. The Revolution in OpenAI Relations and Diversification via Anthropic

Recent days have brought a fundamental shift in Microsoft’s AI strategy. According to reports from Bloomberg and the NYT, Microsoft and OpenAI have officially loosened their partnership. Key takeaways include:

-

End of Exclusivity: Microsoft is no longer the sole entity authorized to resell OpenAI models. This allows ChatGPT to strike deals with rivals like Amazon (AWS) and Oracle.

-

Financial Model Shift: In exchange for ending exclusivity, Microsoft will no longer pay OpenAI a revenue share on products resold via its cloud.

-

The Path to IPO: These changes are intended to facilitate OpenAI's restructuring into a traditional for-profit company and its eventual stock market debut.

To reduce dependence on OpenAI (which accounts for approximately 45% of MSFT's remaining performance obligations), Microsoft is aggressively betting on Anthropic. The Redmond giant invested $5 billion in Anthropic, but more importantly, as part of the deal, Anthropic committed to renting $30 billion of compute from Microsoft. HSBC estimates that Anthropic’s revenue surged from $9 billion in December 2025 to $30 billion in April 2026, making them a second, critical source of orders for Azure. While the market reacted nervously to the loosening of ties with OpenAI, it may turn out that Microsoft has made the best possible decision for the long-term development of its own products.

3. Capex: The Arms Race and the "Nvidia Tax"

Capital Expenditure (Capex) has become a point of contention. The market expects Microsoft to drastically increase spending to match Alphabet and Amazon. However, there is a significant difference in the efficiency of this spending. While Google and Amazon have advanced in-house AI chips (TPU, Trainium), Microsoft still relies heavily on Nvidia (Blackwell and Rubin).

The lack of a proprietary processor at mass scale means a significant portion of Microsoft’s capex is essentially an "Nvidia margin" (estimated at 75% of the chip price). Investors will be scanning the report for progress on the deployment of Maia chips, which could lower infrastructure costs and improve the profitability of the AI segment.

4. M365 and Copilot: Are Customers Willing to Pay?

The Productivity and Business Processes segment, while stable (growth of approx. 14-15%), is causing concern regarding Copilot adoption. Microsoft currently has roughly 15 million paid Copilot subscriptions—a penetration rate of just 3% among its user base. In contrast, Google’s Gemini is showing a much higher adoption rate. If Microsoft cannot demonstrate that AI is materially boosting Office revenue, the thesis of an "AI software revolution" may be undermined.

5. Investment Perspective: Opportunity or Trap?

Despite the stock price being down roughly 12% YTD (and 20% from its highs), the company’s fundamentals remain formidable:

-

Valuation: At approximately $425, Microsoft trades at a P/E ratio of 23x–25x for the current year and roughly 21x–22x for next year. This is 20% below the company’s historical average, making the valuation the most attractive in years.

-

Balance Sheet: The company maintains a "financial fortress" with over $90 billion in cash and a pristine AAA credit rating.

-

Long-term Outlook: For long-term investors, the current sell-off could be seen as an opportunity. Microsoft is no longer just an "OpenAI proxy" but is building a diversified AI ecosystem (OpenAI, Anthropic, proprietary Mistral models, and open-source models).

Summary

The upcoming results will be a test of whether Microsoft can translate technological leadership into repeatable profits. Three numbers will be key: Azure growth rate (expected >30%), Capex levels (signaling confidence in demand), and Copilot subscription dynamics.

While short-term volatility may be high, especially given the overlapping results of other "Mag 7" giants, the low valuation relative to historical averages and the strategic shift toward a more open cloud model suggest that Microsoft is preparing for its next phase of growth, now less vulnerable to the risks of partner concentration.

All or nothing: ServiceNow earnings preview

Did SaaS lost too much? Morgan Stanley says yes.

US OPEN: The market extends losses as investor concerns grow

Daily Summary: Lower inflation weakens the dollar and awakens gold and S&P 500 to gains