- Netflix shares are down around 45% from their all-time high and are trading slightly lower ahead of earnings due after the U.S. market closes on July 16.

- The company is trading at a discount to the S&P 500 for the first time since 2022 based on its forward price-to-earnings (P/E) ratio.

- Wall Street expects revenue to grow 14% year over year while operating margin is forecast to remain strong at around 33%.

- Netflix shares are down around 45% from their all-time high and are trading slightly lower ahead of earnings due after the U.S. market closes on July 16.

- The company is trading at a discount to the S&P 500 for the first time since 2022 based on its forward price-to-earnings (P/E) ratio.

- Wall Street expects revenue to grow 14% year over year while operating margin is forecast to remain strong at around 33%.

Netflix (NFLX.US) will report its second-quarter results after Thursday’s closing bell on Wall Street. For investors, this will be one of the most important reports of the earnings season, as the company has endured an exceptionally difficult year in terms of market sentiment.

Since reaching an all-time high in June 2025, the shares have fallen by around 45%, erasing more than $260 billion in market value, and have ranked among the weakest performers in the S&P 500 over the past 12 months. For the first time since 2022, Netflix is also trading at a discount to the broader market, with its forward P/E ratio at around 20, compared with more than 30 a year ago and a historical company average of roughly 51.

For some investors, this represents a more attractive valuation, but the key question for the market is whether the slowdown in growth is temporary or signals that Netflix is entering a more mature phase of development.

The key questions ahead of Netflix earnings. What will Wall Street focus on?

The financial results themselves may not be the most important part of Thursday’s release. After several quarters of deteriorating sentiment, investors primarily want to hear whether Netflix can reaccelerate growth and preserve its advantage over intensifying competition. Many analysts believe that management commentary and guidance for the coming quarters could have a greater impact on the share price than the second-quarter figures themselves.

According to Bloomberg consensus estimates, the market expects:

- Revenue: $12.58 billion, up 14% year over year

- Revenue in the U.S. and Canada: $5.52 billion

- Revenue in EMEA: $4.03 billion

- Revenue in Latin America: $1.51 billion

- Revenue in Asia-Pacific: $1.53 billion

- Earnings per share: $0.79

- Operating income: $4.13 billion

- Operating margin: 33%

- Cash flow from operations: $2.93 billion

- Free cash flow: $2.72 billion

Investors may pay even closer attention to guidance for the third quarter and the full year. The current consensus calls for third-quarter revenue of $13.0 billion, EPS of $0.84, and an operating margin of 33.5%. For the full year 2026, analysts expect approximately $51.4 billion in revenue, an operating margin of 31.7%, and more than $13 billion in free cash flow.

The market will be watching four issues particularly closely:

- whether Netflix raises its full-year 2026 revenue guidance,

- what the next edition of the “What We Watched” report reveals about actual user engagement,

- whether the company plans to expand further into short-form video and podcasts,

- whether management provides new information about potential acquisitions and its broader M&A strategy.

More important than the reported figures may be what management says about the coming quarters. Following a weaker first quarter, investors are primarily looking for an upward revision to guidance. It is the outlook that could ultimately determine the direction of the shares after the release.

Analysts will also closely monitor commentary on:

- advertising revenue growth,

- the effectiveness of the crackdown on account sharing,

- new short-form video formats,

- the development of podcasts,

- potential acquisitions and the broader M&A strategy,

- viewing-time data, which is increasingly replacing subscriber growth as the main measure of the platform’s health.

This could be Netflix’s most important report in years

In recent quarters, investors have focused less on subscriber additions and more on user engagement. Growing competition from YouTube, Meta, short-form video platforms, and traditional media means Wall Street wants to see whether Netflix can still capture and retain viewers’ attention effectively.

Some portfolio managers believe the company remains fundamentally very strong. Netflix is still the most profitable streaming platform in the world, generates billions of dollars in free cash flow, and is now considerably cheaper than in previous years because of the lower valuation. According to Bloomberg, 51 of 64 analysts recommend buying the shares, while the average price target stands at $112.51, implying approximately 53% upside from current levels.

At the same time, the market remains cautious. Many investors are concerned that slowing user engagement could limit revenue growth, while rising spending on content, advertising, artificial intelligence, and new entertainment formats could put pressure on margins. For that reason, the most important part of the report may not be the second-quarter result itself, but management’s answer to the question of how Netflix intends to reaccelerate growth in the years ahead.

If the company shows improving engagement and raises its outlook, the current valuation may prove to be an attractive starting point for rebuilding investor confidence. However, if the report disappoints again, the market may conclude that the year-long decline has not yet run its course.

Is Netflix a value trap or one of the opportunities on Wall Street?

After more than a year of significant declines, opinions remain divided. On the one hand, the market is concerned about slowing user engagement, stronger competition from YouTube, Meta, and traditional media, as well as heavy spending on content, advertising, and new product development. On the other hand, many portfolio managers believe the current valuation is beginning to reflect most of these risks, while Netflix’s fundamental position remains genuinely strong.

The main bullish argument is valuation. The shares currently trade at a forward P/E ratio of around 21, compared with a ten-year average of more than 50. This is the first time since 2022 that Netflix has traded at a discount to the S&P 500, despite remaining the world’s most profitable streaming platform and continuing to generate billions of dollars in free cash flow.

For some investors, the upcoming report could be a turning point. If management demonstrates improving user engagement, confirms growth in the advertising business, and raises its guidance for the second half of the year, the market may conclude that the worst period for the company is already over. A larger share-buyback programme or more optimistic commentary on margins and platform monetisation could provide an additional catalyst.

At the same time, risks remain elevated. If Netflix once again disappoints with its guidance or fails to present a convincing strategy for improving engagement, investors may conclude that the company has entered a period of structurally slower growth. In that scenario, even a relatively low valuation may not be enough to attract capital back into the stock.

Despite the recent sell-off, Wall Street remains moderately optimistic. According to Bloomberg data, 51 of 64 analysts recommend buying the shares, while the average price target of $112.51 implies more than 50% upside from current levels. The results will primarily test whether Netflix is still a growth company or whether investors will need to lower their expectations and adopt a more defensive valuation framework.

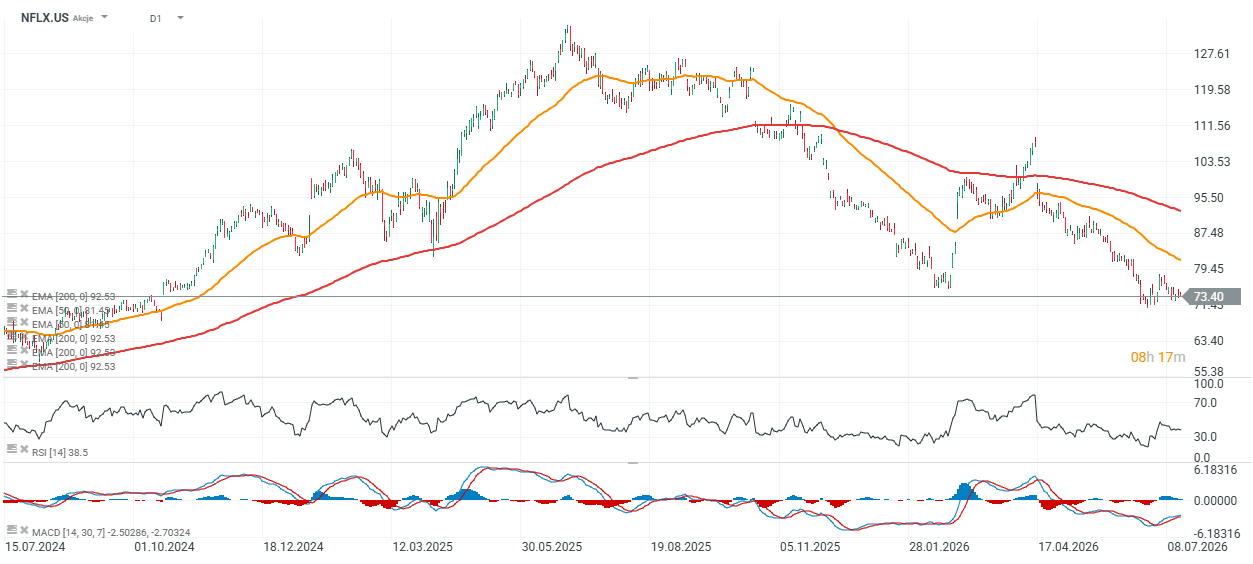

Netflix share price and valuation chart (D1 timeframe)

Netflix shares are trading around 15% below their 200-day EMA, shown by the red line. In a scenario involving stronger-than-expected results and higher guidance, this level, often viewed as a symbolic dividing line between a bull and bear market, could be tested by buyers during the next session. Key support is located near $71. A break below that level would increase the probability of further selling toward $60 per share, a level last seen in the summer of 2024.

Source: xStation5

The chart shows that despite an almost 42% decline in the share price over the past 12 months, Netflix’s fundamentals remain relatively strong. Revenue has continued to grow steadily from quarter to quarter and reached around $12.2 billion in the first quarter of 2026, while operating income rose to approximately $4 billion and the EBIT margin remained high at 32.3%. Over the past eight quarters, Netflix increased revenue by an average of 3.6% quarter over quarter, EBIT by 6.2%, and earnings per share by 9.9%, showing that profitability has grown faster than sales.

At the same time, the decline in the share price has reduced the forward P/E ratio to around 21, well below the company’s historical average. This suggests that the current valuation reflects considerably more investor pessimism than the financial results alone would imply. The upcoming quarterly report may therefore determine whether the market begins to value Netflix as a growth company again or maintains a cautious stance on its outlook.

Source: XTB Research

US Open: S&P 500 shows strength as semiconductor lags 🚩 Western Digital down 12%

SoftBank earnings: Intel and AI are not enough?

Nasdaq 100 Slides Again 🚩 SanDisk Falls 10% After Earnings, Semiconductors Under Pressure

Morning Wrap: Equities under pressure after Wall Street took profits, FX frozen (06.08.2026)