Just a few years ago, Adobe was considered one of the best software companies in the world. Its subscription model ensured stable revenue growth, margins were among the highest in the industry, and millions of professionals used Photoshop every day. Investors were willing to pay a high premium for a business that seemed like a near perfect combination of quality and predictability.

Today, the situation looks completely different.

Since the beginning of the year, Adobe’s shares have lost more than 40 percent of their value, and the market is increasingly asking whether the company has ended up on the wrong side of one of the biggest technological revolutions in recent decades. The rise of generative artificial intelligence has made it easier than ever to create graphics, videos, and documents. With just a few sentences entered into an appropriate model, you can generate an image in seconds that would have required hours of work in professional software just a few years ago.

It is therefore not difficult to understand where investor skepticism comes from. If AI can perform an increasing share of the user’s work, why pay tens of dollars per month for a complex software suite? Will Photoshop and other tools eventually become relics of another era, just as cameras replaced film and smartphones replaced many everyday devices?

This narrative now dominates Adobe’s valuation. The market assumes that AI will not only slow the company’s growth but may also undermine the foundations of its business model over time. As a result, a company long regarded as one of the highest quality names in software has quickly become one of the most heavily discounted tech stocks.

However, one very important question remains.

Does this pessimistic vision find confirmation in Adobe’s financial results and operational data, or is the market once again pricing the future based more on fears than on facts?

Chapter 1. Where did the fear around Adobe actually come from?

Looking at the development of artificial intelligence, it is difficult to say investor concerns are entirely unfounded. Just two or three years ago, creating a professional graphic, removing an object from a photo, or producing a short animation required knowledge of specialized software and many hours of work. Today, more and more of these tasks can be completed with a single prompt entered into an AI model. That is a fundamental shift.

For decades, Adobe’s advantage was based partly on the fact that mastering its tools required time, experience, and practice. Photoshop, Illustrator, and Premiere Pro were not programs you could learn in one evening. For professionals, this created a natural barrier to entry, but for beginners it was often an obstacle.

Generative AI has begun to gradually lower that barrier.

Tools like Midjourney can generate impressive quality images within seconds. Runway automates more and more elements of video editing. Canva is developing its own AI features and allows users to create attractive marketing materials without knowledge of design principles. Even people who have never opened Photoshop before can now produce professional looking graphics.

It is therefore no surprise that a question has emerged that until recently seemed absurd: will the world even need such complex tools as Photoshop if more and more tasks can be done faster and more easily?

This is the core of the current narrative around Adobe. If AI becomes the main tool of creative professionals, traditional software may gradually lose relevance. For a company that has long derived the vast majority of its revenue from a subscription model, such a scenario would mean not only slower growth but also pricing pressure and lower customer loyalty.

At first glance, this sounds entirely rational. But there is one problem.

Most of this narrative is based on assumptions about the future. Meanwhile, investors have something far more valuable than forecasts: financial and operational data showing how Adobe’s customers are behaving today. And this is where the story becomes truly interesting.

Chapter 2. Financial results tell a completely different story

If one looked only at the stock price, one might assume Adobe has entered a deep crisis. The market is valuing the company as if AI has already started taking its customers and gradually undermining its entire business model. If that were true, the first place it would show up would be in financial results. Declining revenues, shrinking margins, or deteriorating cash flows would be a natural consequence of losing competitive advantage.

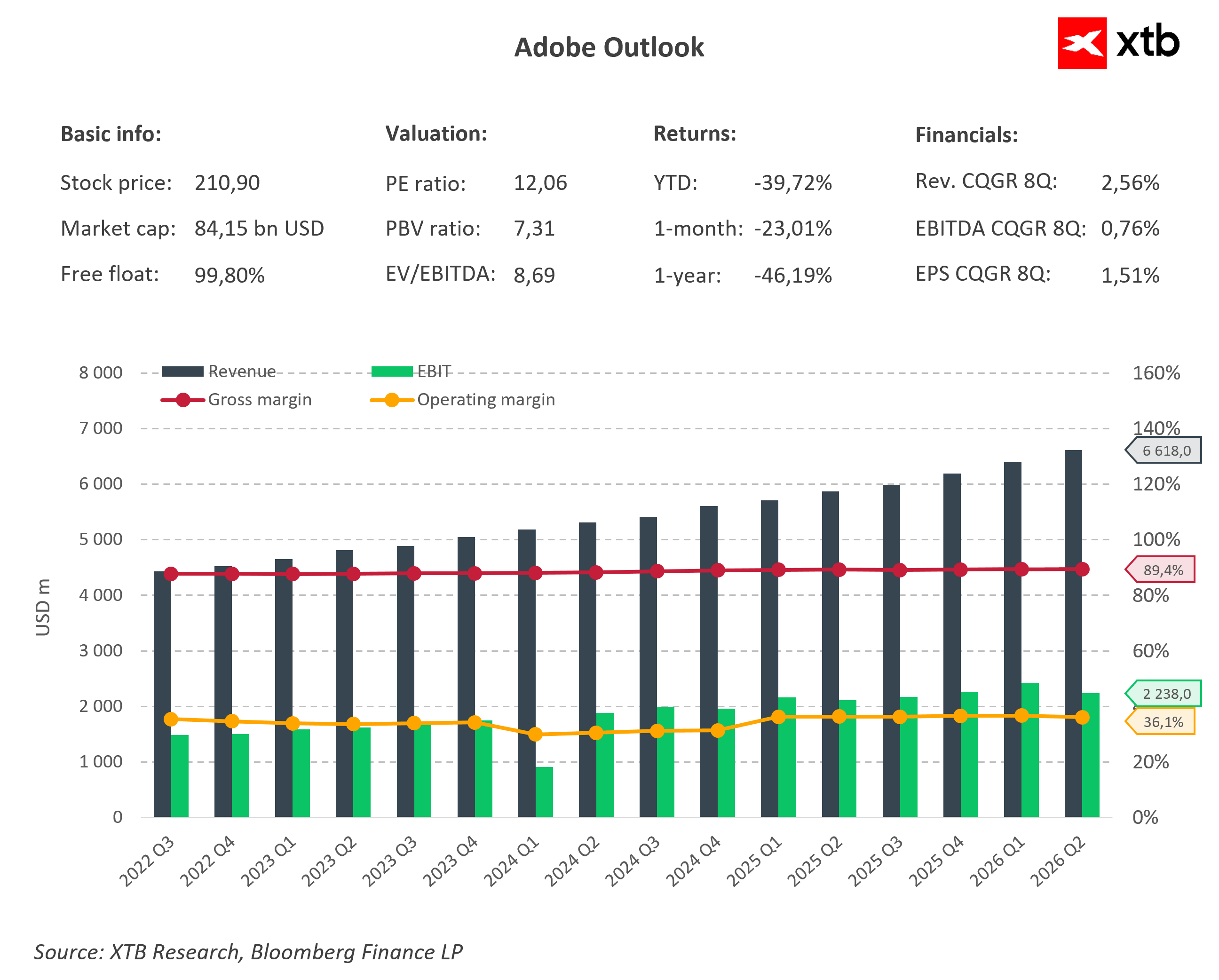

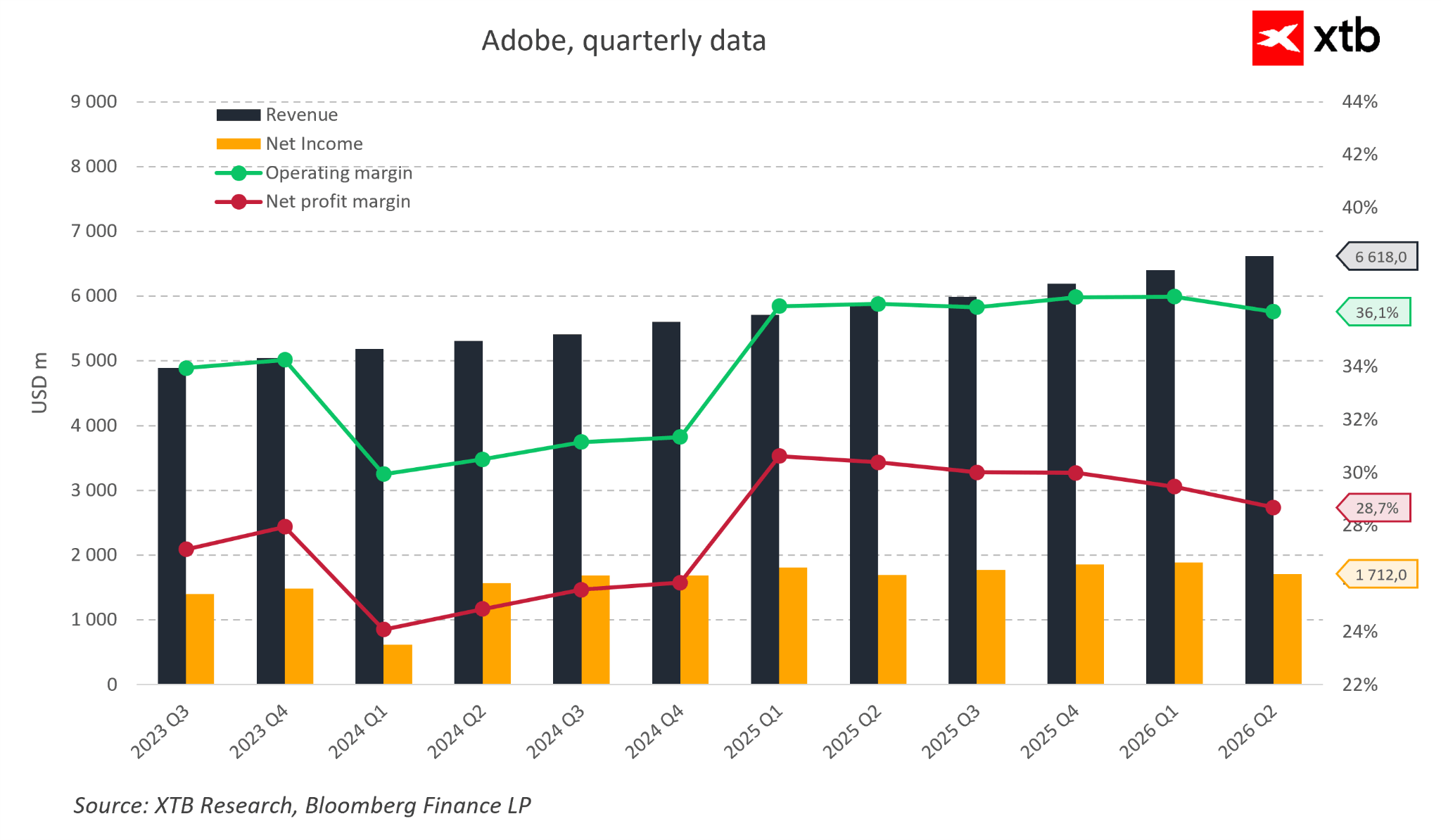

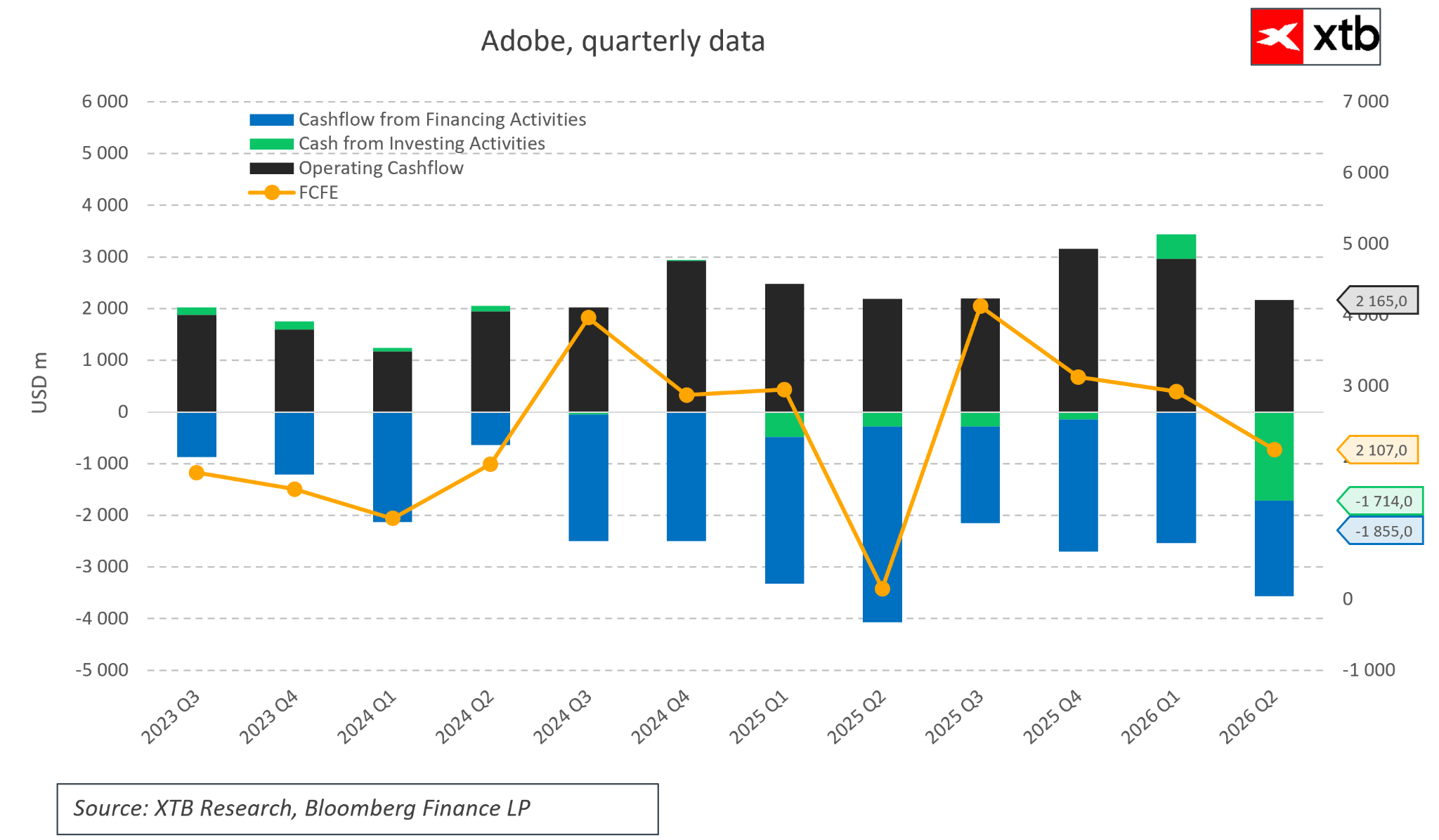

The problem is that Adobe’s reports show a completely different picture. The company has been steadily expanding for many quarters. Revenue is setting new records almost quarter by quarter, and net income remains very strong despite massive investments in new AI based products. Even more impressive are operating margins, which remain extremely stable at around 36 percent. There are not many large software companies that can both grow and maintain such high profitability at the same time.

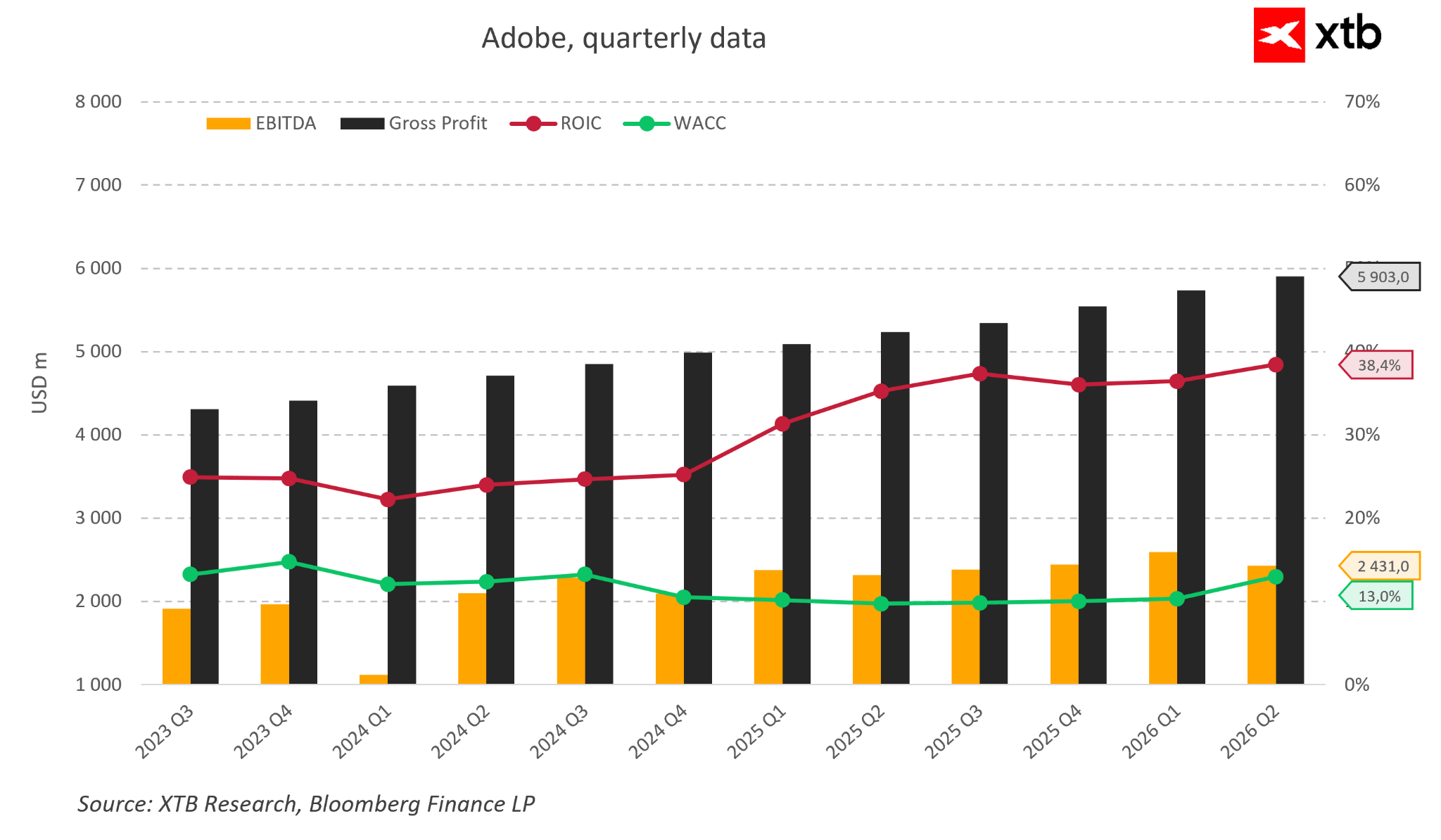

The quality of the business does not end with revenue growth. Adobe has long belonged to the group of companies that are exceptionally efficient at converting sales into cash and shareholder value. Its ROIC currently exceeds 38 percent, while the cost of capital is nearly three times lower. This means each new investment generates value far above its financing cost. At the same time, operating profit and gross profit continue to grow quarter by quarter, showing that the business is scaling efficiently.

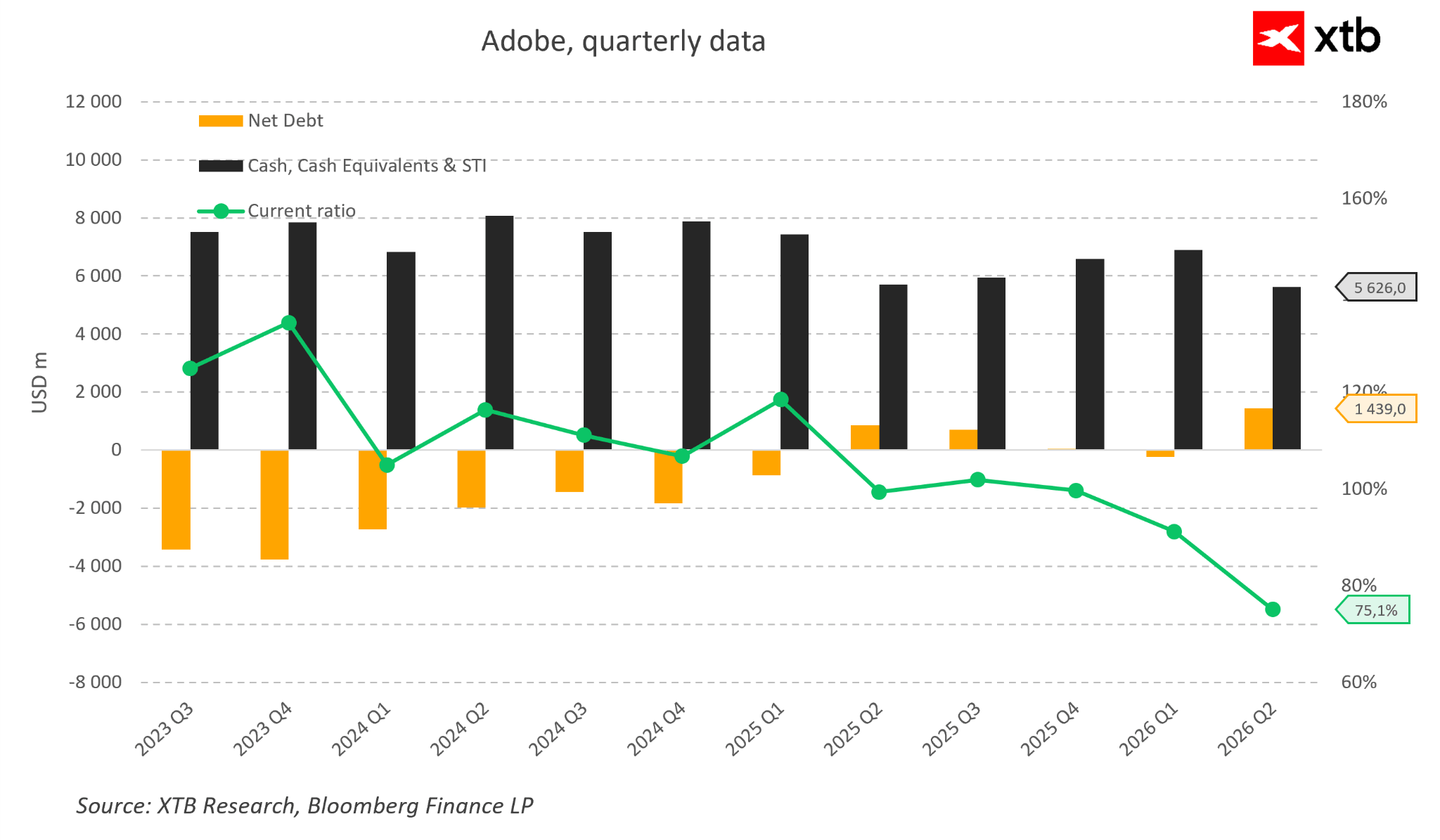

The balance sheet is equally solid. Just a few quarters ago, Adobe had net cash, and despite an active share buyback program, its financial position remains very comfortable. The company holds billions in cash, allowing it to simultaneously invest in AI development, finance acquisitions, and return capital to shareholders. Even though net debt has increased slightly in recent quarters, it is hardly at a level that would raise concerns for a company generating such strong cash flows.

This leads to a somewhat surprising conclusion. If you removed the company’s name from the chart, few investors would assume they are looking at a firm supposedly losing the battle with one of the biggest technological revolutions in decades. On the contrary, the financial data paints a picture of a mature business that continues to grow, remains highly profitable, and generates massive amounts of cash.

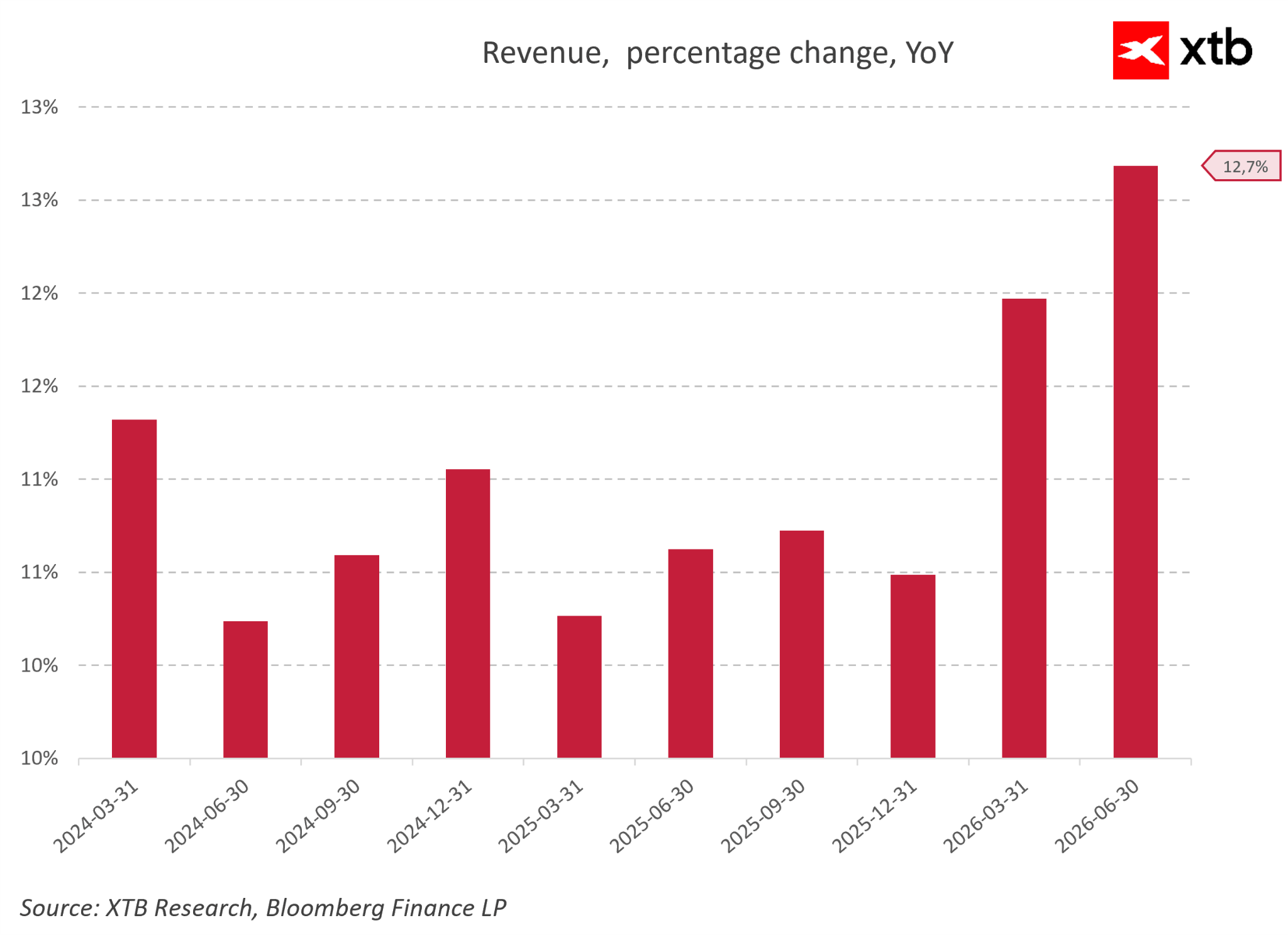

Instead of any signs of crisis, year over year revenue dynamics show that Adobe is actually shifting into a higher gear. Throughout 2024 and 2025, the company grew at a stable and predictable rate of 10 to 11 percent. The real acceleration appears in the first half of 2026, where growth first jumped to around 12 percent and then reached an impressive 12.7 percent year over year in the quarter ending June 2026. These hard data points directly contradict the narrative of supposed market loss to AI competitors.

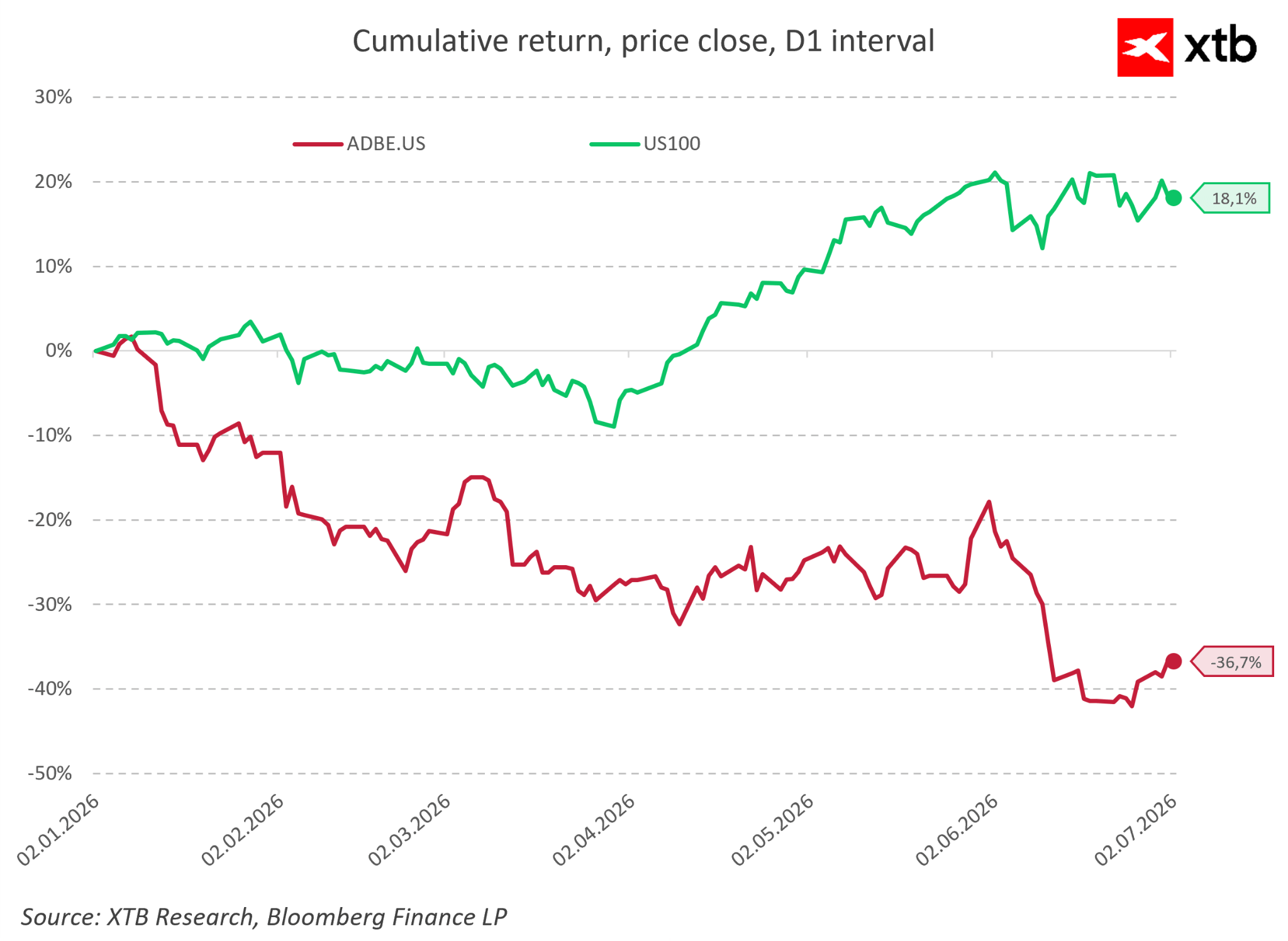

At the same time, the stock market has completely detached from fundamentals, which is clearly visible in cumulative returns since the beginning of 2026. While the broader tech market rose by a solid 18.1 percent over this period, Adobe’s stock fell by nearly 40 percent. Such a divergence usually signals deep operational deterioration, which, based on Adobe’s reports, simply does not exist.

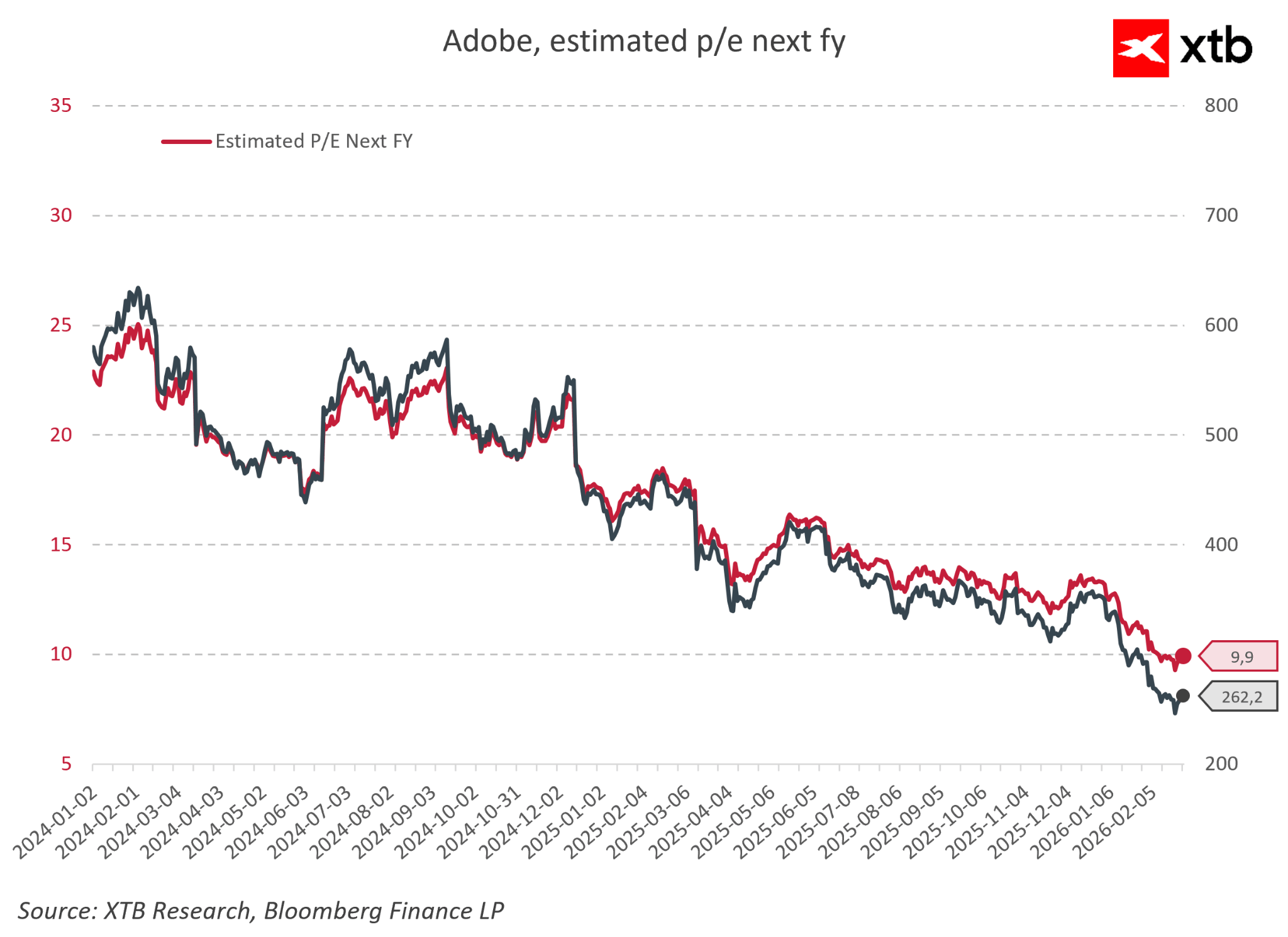

As a result of this sharp selloff, Adobe’s valuation has fallen to absurdly low levels. The forward price to earnings ratio, which stood at 23 to 25 at the beginning of 2024, dropped to around 9.9 by mid 2026. A company with a near monopolistic position, growing at a double digit rate, has been priced by market sentiment at a single digit multiple typical of declining businesses.

This all leads to a surprising conclusion. If you removed the company name from the chart, few investors would think they are looking at a firm supposedly losing against one of the biggest technological revolutions of recent decades. Instead, the financial data shows a mature business that continues to grow, remains highly profitable, and generates enormous cash flows.

So why does the market see the story so differently?

Perhaps the answer lies in the fact that most investors look at Adobe as a Photoshop company. Meanwhile, Photoshop is only a small piece of a much larger puzzle.

Chapter 3. Adobe does not sell Photoshop

When most investors think of Adobe, the first associations are Photoshop, Illustrator, or Premiere Pro. This is natural, as these are the company’s most recognizable products. The problem is that this view is too simplified.

Adobe does not sell Photoshop, and in reality, it never treated it as a standalone product.

Photoshop is only an entry point into a much larger system that represents the company’s true value, the creative ecosystem. It is a comprehensive workflow where an idea moves from initial concept to finished product, rather than a single editing tool.

Users are not simply buying graphic software. They are entering an environment where they create, store, collaborate, and share projects. All these elements are interconnected, and the longer someone works within this ecosystem, the harder it becomes to leave. Switching costs are no longer just about software pricing but about rebuilding an entire way of working.

In this sense, Adobe operates like infrastructure for creative work, similar to how Microsoft became the standard in office environments. Competitive advantages do not come from individual applications but from their integration into a unified system. This is where the market’s key misunderstanding arises. If Adobe is seen only as Photoshop, then any AI image generator looks like a direct threat. But if Adobe is seen as a creative operating system, the competitive landscape becomes much more complex.

The question is no longer who can generate an image faster, but who can replace the entire creation process. That includes not only content generation, but also team collaboration, multi stage workflows, version control, format compatibility, and integration with the broader work environment. At present, AI tools only replace fragments of this process, they do not replace it entirely.

That is why Adobe is not directly competing with image generators, but with attempts to rebuild the entire creative workflow from scratch.

Chapter 4. AI in Adobe: threat or natural evolution?

The market narrative often assumes Adobe was caught off guard by AI. In reality, the company is not only responding to this shift but actively integrating it into its products.

The best example is Firefly, Adobe’s own AI model, directly integrated into the Creative Cloud suite. Rather than treating AI as an external threat, Adobe is embedding it into its ecosystem and developing it as a natural extension.

This is a crucial difference. In this case, AI does not replace the workflow, it extends it. Users still operate within the same environment, but some tasks are performed faster or automatically.

In practice, this means Adobe is not fighting the trend of prompt based content creation; it is absorbing it into its subscription model. This simultaneously lowers the entry barrier for new users while maintaining control over the professional creative environment.

The market often views AI as a force that could destroy Adobe’s model. In reality, in the short term it acts more as a tool that increases engagement and usage rather than replacing the company’s products.

The key question is therefore not whether Adobe will be replaced by AI, but whether it can maintain its role as the central creative platform where AI becomes just another layer of functionality. So far, everything suggests the company’s strategy is moving in exactly that direction.

Chapter 5. Why the market still sees risk

Despite stable results and AI integration, the market continues to price in significant risk for Adobe. This mainly stems from a misunderstanding of what the company’s product actually is.

Investors often view Adobe through individual applications rather than the entire workflow system. In this framing, AI does indeed look like direct competition that can simplify and eliminate the need for advanced tools.

The problem is that professional creative work is not about isolated tasks, but about the entire process. In this context, even advanced AI generators do not solve issues such as collaboration, version control, project consistency, or client integration.

The market also overestimates the speed of change, assuming each new technology instantly replaces the previous one. In reality, most technological transformations are evolutionary, not immediate.

As a result, a gap emerges between business fundamentals and market narrative. Adobe continues to generate stable cash flows and grow, but its valuation reflects a scenario of severe business erosion. This gap between perception and reality is the main driver of the current story around the company.

Chapter 6. Valuation and asymmetry of expectations

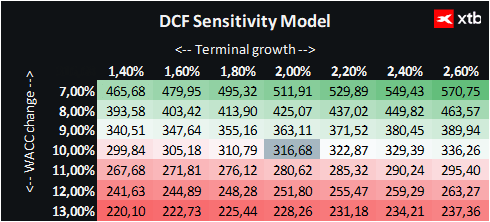

We present a DCF valuation of Adobe. It should be emphasized that it is for informational purposes only and should not be treated as investment advice or a precise valuation.

Adobe remains one of the key global players in software, providing a comprehensive ecosystem of tools used by professionals worldwide. Its subscription model ensures high revenue predictability and stable cash flows, which has long established its status as one of the highest quality businesses in the tech sector.

In recent years, the key factor shaping market narrative has been generative AI, which potentially lowers barriers to digital content creation and changes how users work. This factor largely explains the sharp decline in the stock price and the market’s shift from a growth narrative to a scenario of significant business erosion.

Given the current share price of around 210 dollars and a DCF valuation of approximately 316 dollars per share, the upside potential is about 50 percent. This implies a clear asymmetry between market pricing and a conservative cash flow model.

However, this does not eliminate risk. The current valuation largely assumes a deep transformation of Adobe’s business model due to AI. The key question is not the company’s current financial health, but whether it can maintain its competitive advantage built around the Creative Cloud ecosystem.

The biggest risk remains a gradual weakening of user lock in. For years, the longer someone used Adobe tools, the harder it was to switch. If AI tools begin to take over not only individual features but the entire creative process, this effect may weaken, impacting both the subscription model and customer loyalty.

An additional risk is increasing competition from fully AI native platforms, built from the ground up around automation and simple text based interfaces.

This creates a classic situation where strong financial fundamentals collide with a market narrative assuming deep structural disruption. This gap between real data and expectations is the key element of the Adobe story today.

Chapter 7. Summary: Is artificial intelligence taking Adobe’s future?

- Valuation paradox: The market reacted to generative AI with extreme panic, leading to a more than 40 percent drop in Adobe’s share price. This also pushed the forward price to earnings ratio down to a single digit level around 9.9x, not seen in years.

- No crisis in financial results: The bearish scenario is completely inconsistent with operational reality. Adobe continues to break revenue records, maintains an exceptionally stable operating margin of around 36 percent, and generates a ROIC exceeding 38 percent.

- Acceleration instead of slowdown: Rather than losing customers to free or cheaper AI tools, year over year revenue growth in the first half of 2026 actually accelerated.

- Misinterpretation of the product: The market’s main mistake is viewing Adobe only through individual apps like Photoshop. In reality, the company does not sell programs, but a complete and integrated operating system for creative work that is extremely difficult to replace.

- Absorption instead of destruction: Adobe has not been caught off guard by AI. Through successful deployment of its Firefly model, it actively absorbs prompt based technology into its ecosystem, turning it into a tool that increases loyalty and lowers barriers to entry.

- Infrastructure over content generation: Professional creative work is not just generating an image in seconds, as tools like Midjourney do, but a full process involving teamwork, version control, copyright compliance, and format compatibility. In these areas, Adobe remains unmatched.

- Cash machine: The company has a strong balance sheet and stable operating cash flows of 2 to 3 billion dollars per quarter, allowing it to fund AI innovation and aggressive share buybacks at depressed valuations.

- Strong risk reward asymmetry: The current DCF valuation suggests Adobe’s intrinsic value is significantly above its market price. The market is pricing in an extremely pessimistic scenario while ignoring strong and growing fundamentals.

Alphabet and Tesla report earnings 🚩 Google's AI business shines, Tesla accelerates Optimus plans

Daily Summary: Wall Street Stabilizes Despite Higher Oil Prices

All or nothing: ServiceNow earnings preview

US Open: S&P 500 Tries to Halt the Decline 🗽 GE Vernova Falls 5%